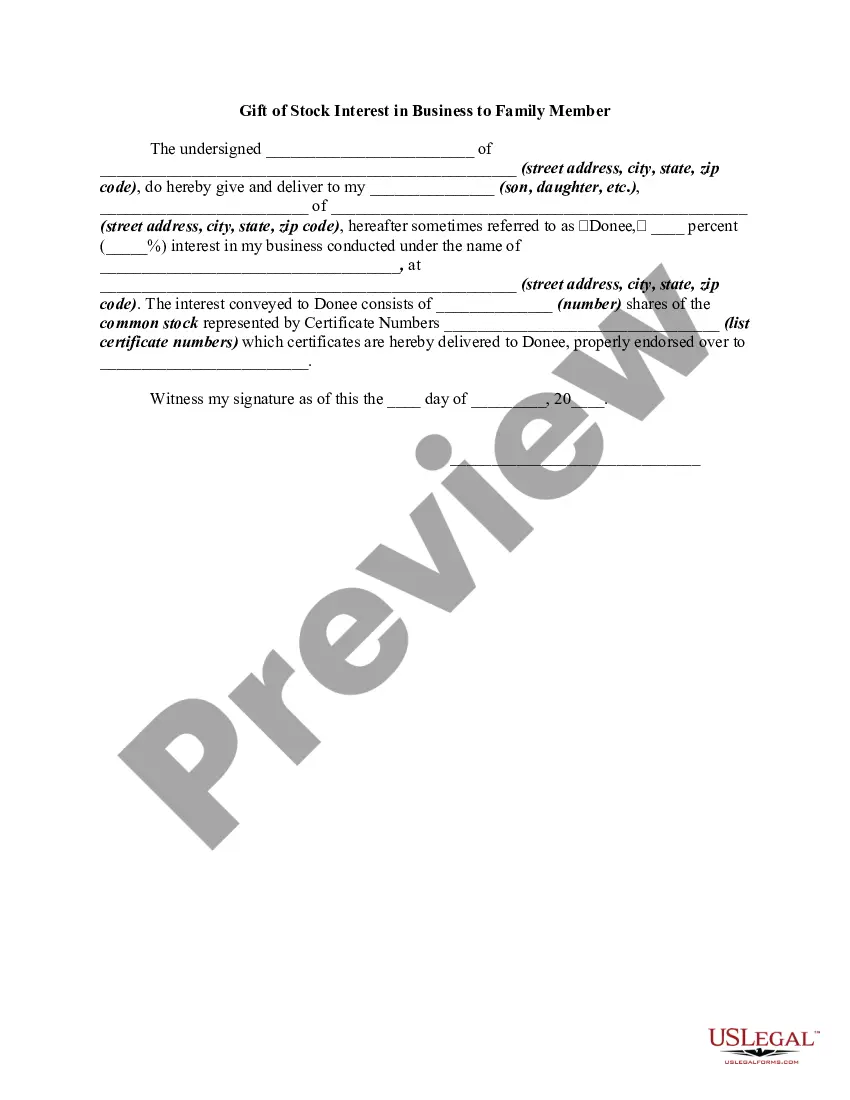

A gift involves transferring title by voluntary action of the owner without receiving anything in exchange. A gift of property is a:

- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

The following form is a gift to a family member of stock in a business owned by the donor.

The Massachusetts Gift of Stock Interest in Business to Family Member refers to a legal transaction where an individual, residing in the state of Massachusetts, gifts a portion or all of their stock interest in a business to a family member. This type of gift entails the transfer of ownership of stocks from one family member to another, with the intention of providing financial support or transferring business ownership within the family. The gift of stock interest in a business can hold significant financial, strategic, and emotional implications. By transferring stock ownership to a family member, the donor relinquishes control, benefits, and rights associated with the stocks, and transfer them to the recipient. This gift can be used to strengthen familial bonds, support inheritance planning, or provide a financial boost to the recipient. One of the key aspects to consider with the Massachusetts Gift of Stock Interest in Business to Family Member is the applicable tax treatment. Different types of stock gifts may have distinct tax implications. In general, gifting stocks may qualify as a taxable event, and it is important to consult with a tax professional to understand any potential tax consequences and ensure compliance with state and federal tax laws. Some variations of the Massachusetts Gift of Stock Interest in Business to Family Member may include specific types of stock transfers, such as gifting shares of common stock or preferred stock. The type of stock involved in the gift can have varying rights and privileges, and it is crucial to clearly identify the type of stock being transferred in order to accurately capture the legal and financial aspects of the gift. Proper documentation is a critical component of this process. The donor should execute a stock transfer form or other relevant legal documents to formally transfer ownership rights to the family member recipient. Additionally, it is advisable to consult an attorney or legal expert to ensure that all legal requirements are met. This may include complying with any applicable securities regulations, corporate bylaws, or specific business partnership agreements. In conclusion, the Massachusetts Gift of Stock Interest in Business to Family Member involves the transfer of stock ownership within a family. It can serve as a means of providing financial support, transferring business ownership, or as part of inheritance planning. Different types of stock may be transferred, each with its own unique legal and financial implications. Understanding the tax consequences and adhering to the necessary documentation and legal requirements is vital in successfully completing this transaction.

The Massachusetts Gift of Stock Interest in Business to Family Member refers to a legal transaction where an individual, residing in the state of Massachusetts, gifts a portion or all of their stock interest in a business to a family member. This type of gift entails the transfer of ownership of stocks from one family member to another, with the intention of providing financial support or transferring business ownership within the family. The gift of stock interest in a business can hold significant financial, strategic, and emotional implications. By transferring stock ownership to a family member, the donor relinquishes control, benefits, and rights associated with the stocks, and transfer them to the recipient. This gift can be used to strengthen familial bonds, support inheritance planning, or provide a financial boost to the recipient. One of the key aspects to consider with the Massachusetts Gift of Stock Interest in Business to Family Member is the applicable tax treatment. Different types of stock gifts may have distinct tax implications. In general, gifting stocks may qualify as a taxable event, and it is important to consult with a tax professional to understand any potential tax consequences and ensure compliance with state and federal tax laws. Some variations of the Massachusetts Gift of Stock Interest in Business to Family Member may include specific types of stock transfers, such as gifting shares of common stock or preferred stock. The type of stock involved in the gift can have varying rights and privileges, and it is crucial to clearly identify the type of stock being transferred in order to accurately capture the legal and financial aspects of the gift. Proper documentation is a critical component of this process. The donor should execute a stock transfer form or other relevant legal documents to formally transfer ownership rights to the family member recipient. Additionally, it is advisable to consult an attorney or legal expert to ensure that all legal requirements are met. This may include complying with any applicable securities regulations, corporate bylaws, or specific business partnership agreements. In conclusion, the Massachusetts Gift of Stock Interest in Business to Family Member involves the transfer of stock ownership within a family. It can serve as a means of providing financial support, transferring business ownership, or as part of inheritance planning. Different types of stock may be transferred, each with its own unique legal and financial implications. Understanding the tax consequences and adhering to the necessary documentation and legal requirements is vital in successfully completing this transaction.