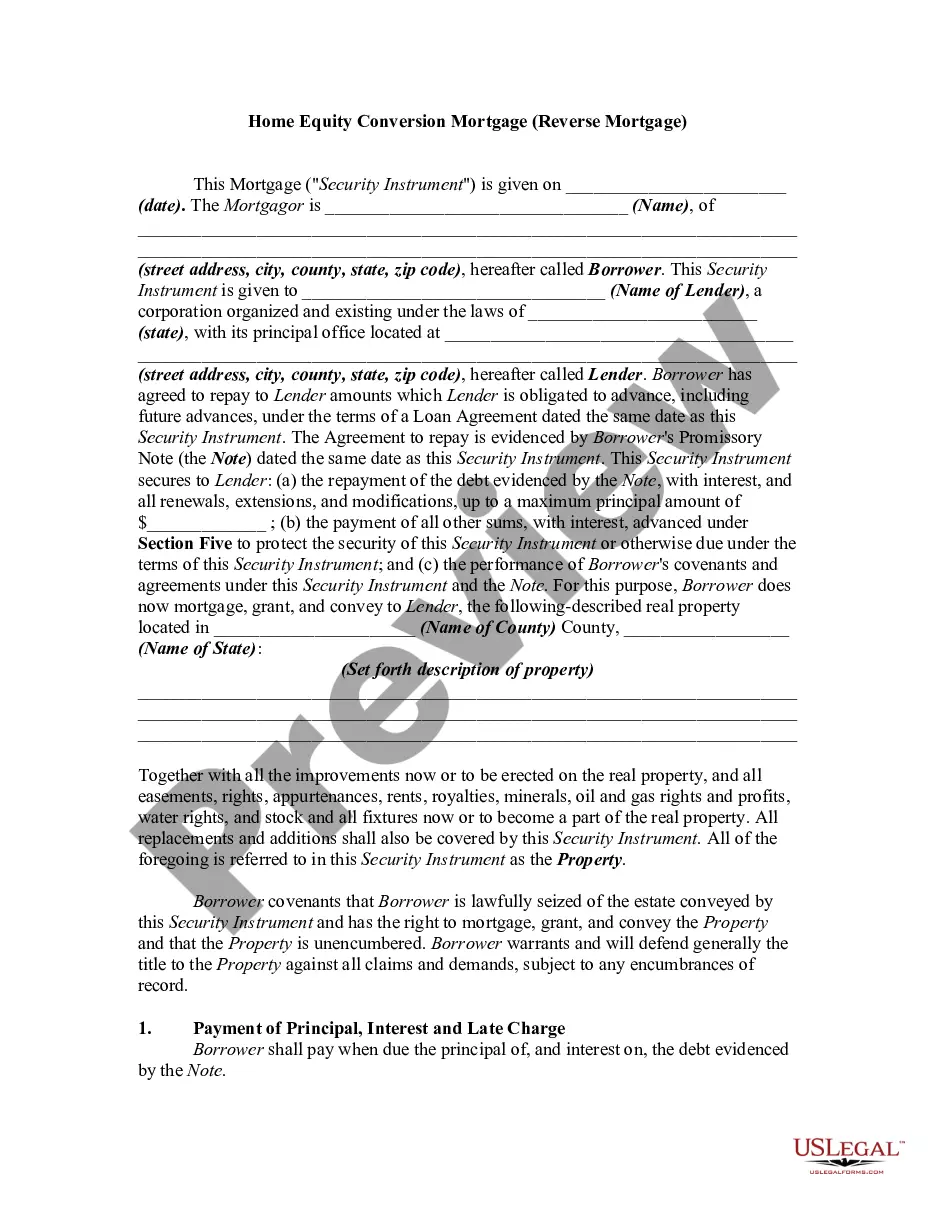

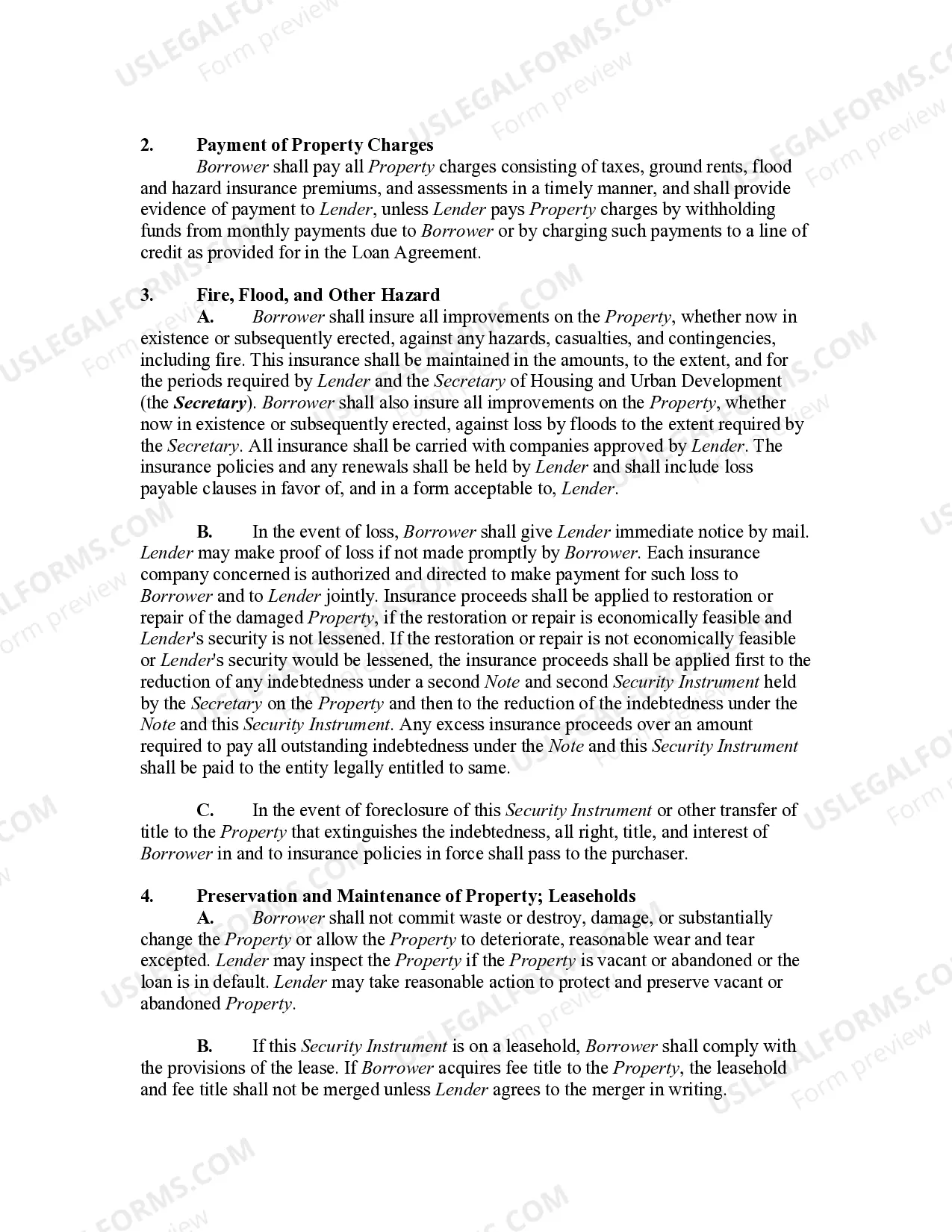

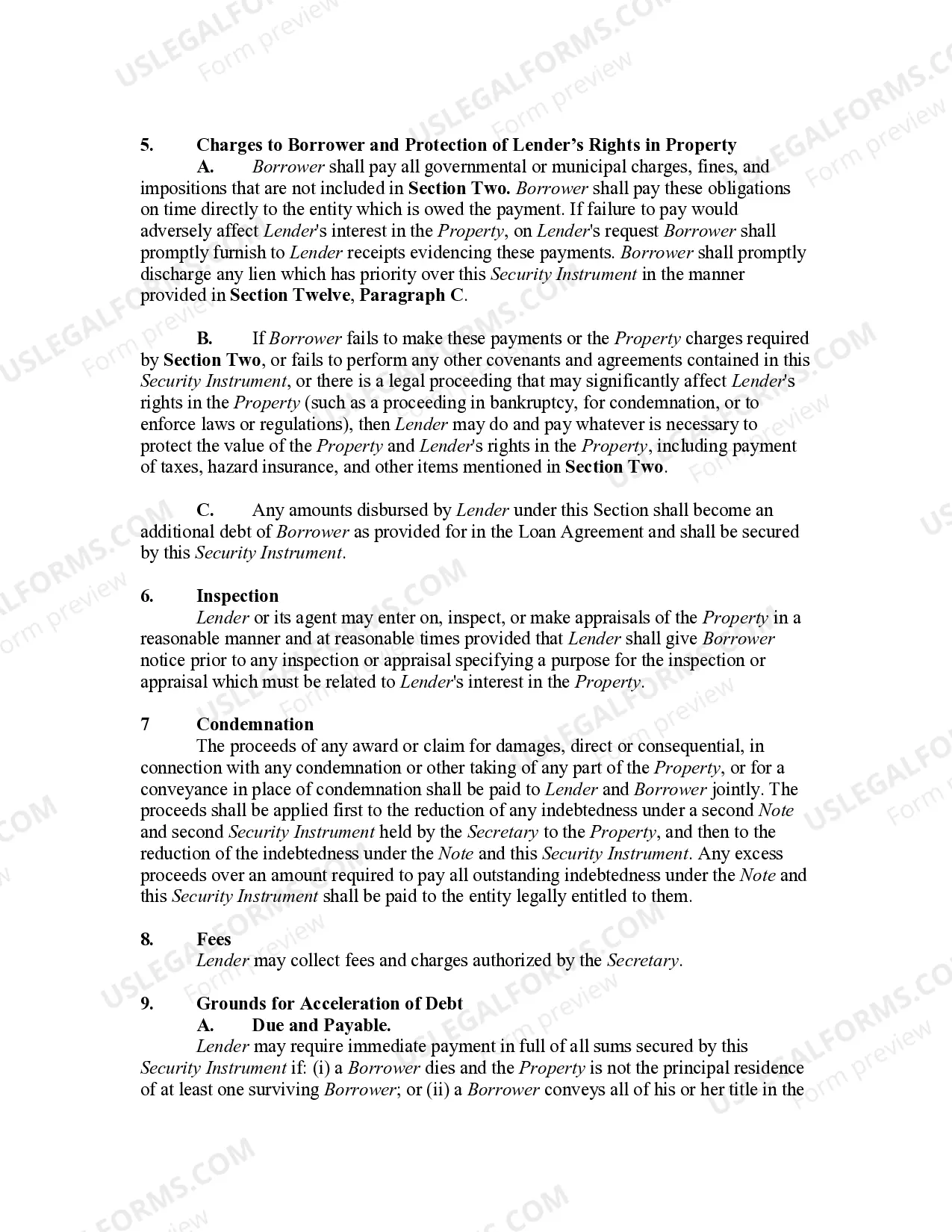

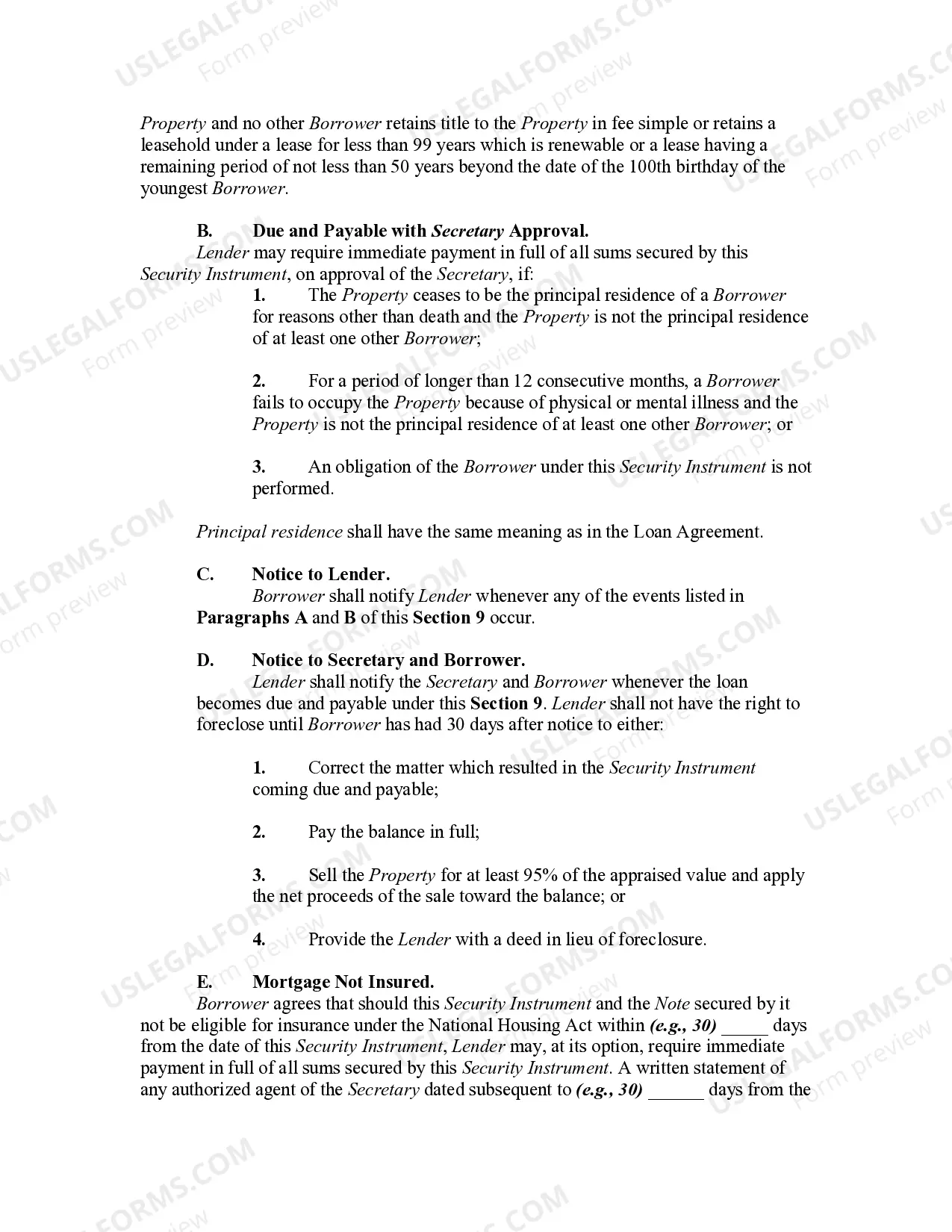

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

A Massachusetts Home Equity Conversion Mortgage (HELM), also known as a reverse mortgage, is a specialized loan program designed for homeowners aged 62 and older to convert a portion of their home equity into usable cash. By utilizing this financial tool, Massachusetts residents can tap into their home's value without selling the property or making monthly mortgage payments. One type of HELM available in Massachusetts is the fixed-rate reverse mortgage. This option offers a lump-sum payment, allowing homeowners to receive a predetermined amount of money upfront. The fixed-rate HELM provides stability and security for borrowers, as the interest rate remains consistent throughout the loan term. Another option is the adjustable-rate reverse mortgage, which provides borrowers with various disbursement choices. Massachusetts homeowners can receive their funds as a lump sum, a line of credit, or a series of monthly payments. The adjustable rate ensures flexibility, as borrowers have the freedom to modify their payment plans according to their specific financial needs. The Massachusetts HELM reverse mortgage program is regulated by the Federal Housing Administration (FHA) and financially insured by the U.S. Department of Housing and Urban Development (HUD). This ensures that borrowers are protected and that lenders adhere to strict guidelines and regulations. To be eligible for a Massachusetts HELM reverse mortgage, homeowners must meet specific criteria, including being at least 62 years old, owning the home as the primary residence, and having sufficient equity in the property. Additionally, borrowers must undergo mandatory counseling sessions offered by HUD-approved counselors to ensure they fully understand the terms and obligations associated with the loan. By choosing a Massachusetts Home Equity Conversion Mortgage (HELM), homeowners can access the equity they have built in their property, allowing them to supplement retirement income, cover healthcare expenses, make home improvements, or fulfill any other financial needs. It is essential to consider the pros and cons of this loan product and seek professional advice before making any decisions.