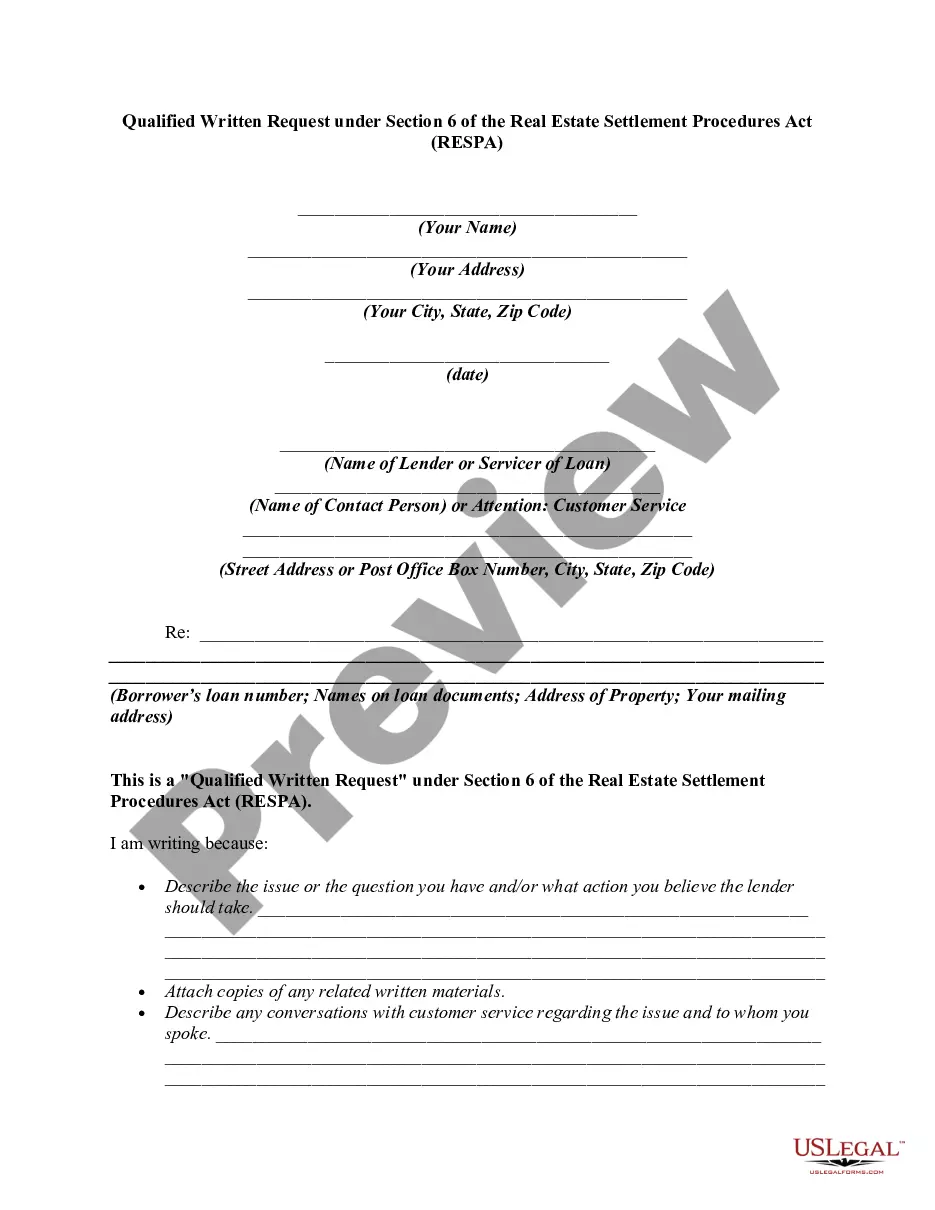

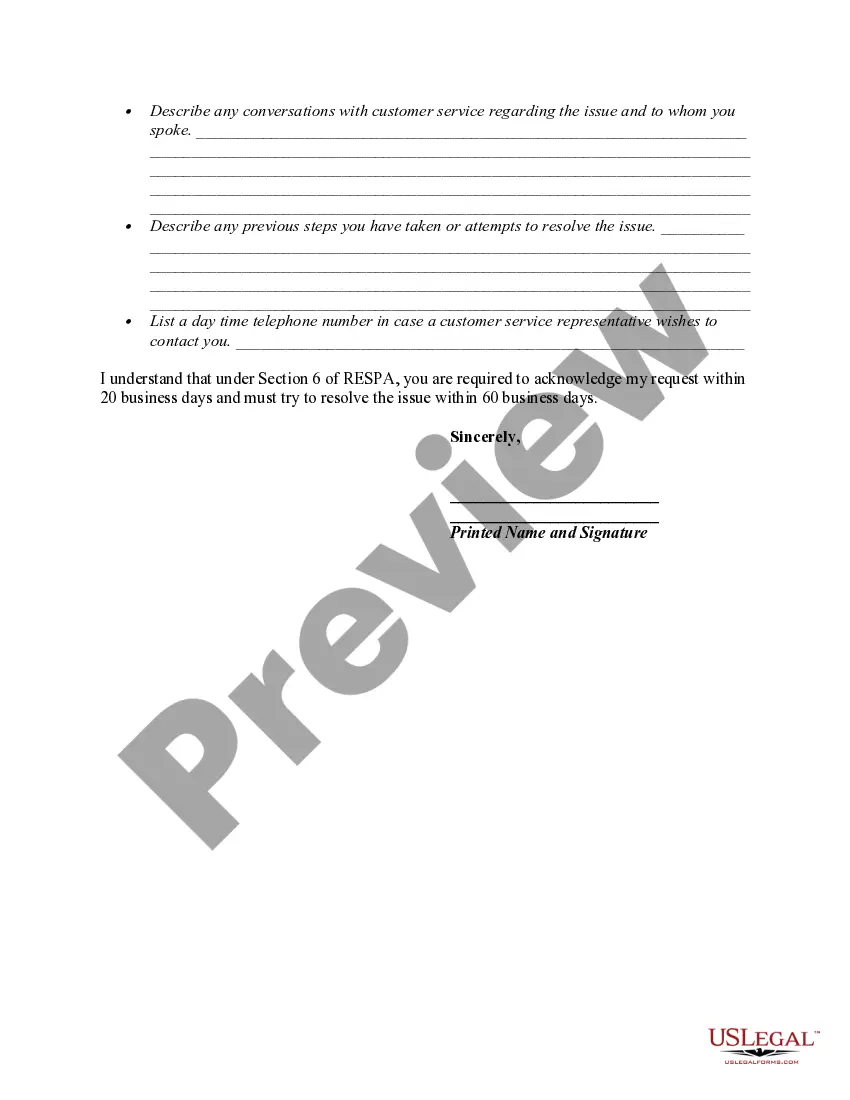

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

A Massachusetts Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a legal tool that homeowners can utilize to obtain information from their mortgage services. A BWR allows borrowers to request specific details about their mortgage loan and service's actions, ensuring compliance with RESP regulations. This detailed description will outline the purpose, process, and potential types of requests that fall under Massachusetts BWR. RESP, enforced by the Consumer Financial Protection Bureau (CFPB), aims to protect borrowers from unscrupulous lending practices and promote transparency in the real estate settlement process. Section 6 of RESP empowers borrowers to submit a BWR to their mortgage services. This provision enables consumers to seek information, clarification, or corrections regarding their loan and payment issues. Under Massachusetts BWR, borrowers can make formal requests to their mortgage services about various matters related to their loans, including: 1. Loan Account Details: Borrowers can request a detailed breakdown of their loan accounts, including principal balance, interest rate, payment history, escrow accounts, and any additional charges or fees applied. 2. Mortgage Servicing Transfers: If the mortgage gets transferred from one service to another, borrowers can seek information about the transfer terms, timelines, and contact details for the new servicing entity. 3. Escrow Account: BWR can be used to obtain specific information regarding the management of escrow accounts, such as the calculation of escrow payments, disbursement of funds, and any surplus or deficiency amounts. 4. Loan Modification and Forbearance: Borrowers facing financial difficulties can use the BWR to initiate discussions regarding loan modifications, forbearance plans, or alternatives to foreclosure. This request helps clarify eligibility criteria, required documentation, and potential impacts on the loan terms. 5. Fees and Charges: Borrowers can question the validity of any charges, fees, or assessments imposed by the mortgage service, including late fees, property inspection fees, or force-placed insurance charges. 6. Error Resolution and Documentation: In cases where borrowers identify errors in their loan documents, billing statements, or credit reporting, they can seek explanations, corrections, or updated documents through the BWR process. To initiate a Massachusetts BWR, borrowers should submit a written request to their mortgage service with relevant details, such as loan number, property address, and a clear description of the information sought. The service is obligated to acknowledge receipt of the BWR within five business days and initiate an investigation into the requested matters. Within 30 business days, the service must provide a response, either complying with the request, requesting additional time (up to 15 business days), or explaining why compliance is not feasible. Multiple BWR requests can be made under Section 6 of RESP if needed. Each request should focus on a specific issue or information, enabling borrowers to address their concerns comprehensively. However, it is essential to ensure that the requests are reasonable, relevant, and not overly burdensome for the service. In conclusion, a Massachusetts Qualified Written Request under Section 6 of RESP empowers borrowers to request information and resolve issues related to their mortgage loans. By utilizing this legal tool, homeowners can ensure compliance with RESP regulations, promote transparency, and seek clarification on various aspects of their mortgage servicing.A Massachusetts Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a legal tool that homeowners can utilize to obtain information from their mortgage services. A BWR allows borrowers to request specific details about their mortgage loan and service's actions, ensuring compliance with RESP regulations. This detailed description will outline the purpose, process, and potential types of requests that fall under Massachusetts BWR. RESP, enforced by the Consumer Financial Protection Bureau (CFPB), aims to protect borrowers from unscrupulous lending practices and promote transparency in the real estate settlement process. Section 6 of RESP empowers borrowers to submit a BWR to their mortgage services. This provision enables consumers to seek information, clarification, or corrections regarding their loan and payment issues. Under Massachusetts BWR, borrowers can make formal requests to their mortgage services about various matters related to their loans, including: 1. Loan Account Details: Borrowers can request a detailed breakdown of their loan accounts, including principal balance, interest rate, payment history, escrow accounts, and any additional charges or fees applied. 2. Mortgage Servicing Transfers: If the mortgage gets transferred from one service to another, borrowers can seek information about the transfer terms, timelines, and contact details for the new servicing entity. 3. Escrow Account: BWR can be used to obtain specific information regarding the management of escrow accounts, such as the calculation of escrow payments, disbursement of funds, and any surplus or deficiency amounts. 4. Loan Modification and Forbearance: Borrowers facing financial difficulties can use the BWR to initiate discussions regarding loan modifications, forbearance plans, or alternatives to foreclosure. This request helps clarify eligibility criteria, required documentation, and potential impacts on the loan terms. 5. Fees and Charges: Borrowers can question the validity of any charges, fees, or assessments imposed by the mortgage service, including late fees, property inspection fees, or force-placed insurance charges. 6. Error Resolution and Documentation: In cases where borrowers identify errors in their loan documents, billing statements, or credit reporting, they can seek explanations, corrections, or updated documents through the BWR process. To initiate a Massachusetts BWR, borrowers should submit a written request to their mortgage service with relevant details, such as loan number, property address, and a clear description of the information sought. The service is obligated to acknowledge receipt of the BWR within five business days and initiate an investigation into the requested matters. Within 30 business days, the service must provide a response, either complying with the request, requesting additional time (up to 15 business days), or explaining why compliance is not feasible. Multiple BWR requests can be made under Section 6 of RESP if needed. Each request should focus on a specific issue or information, enabling borrowers to address their concerns comprehensively. However, it is essential to ensure that the requests are reasonable, relevant, and not overly burdensome for the service. In conclusion, a Massachusetts Qualified Written Request under Section 6 of RESP empowers borrowers to request information and resolve issues related to their mortgage loans. By utilizing this legal tool, homeowners can ensure compliance with RESP regulations, promote transparency, and seek clarification on various aspects of their mortgage servicing.