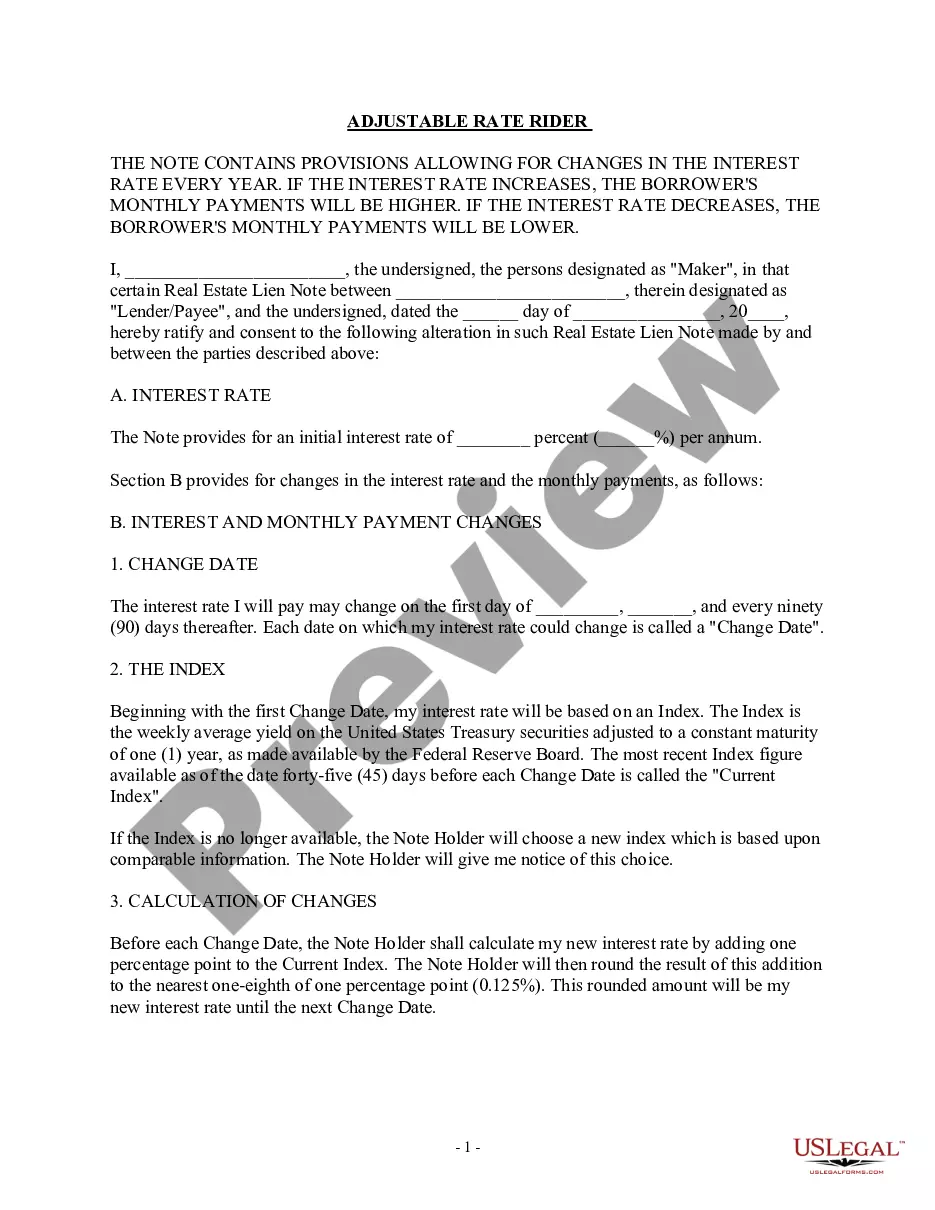

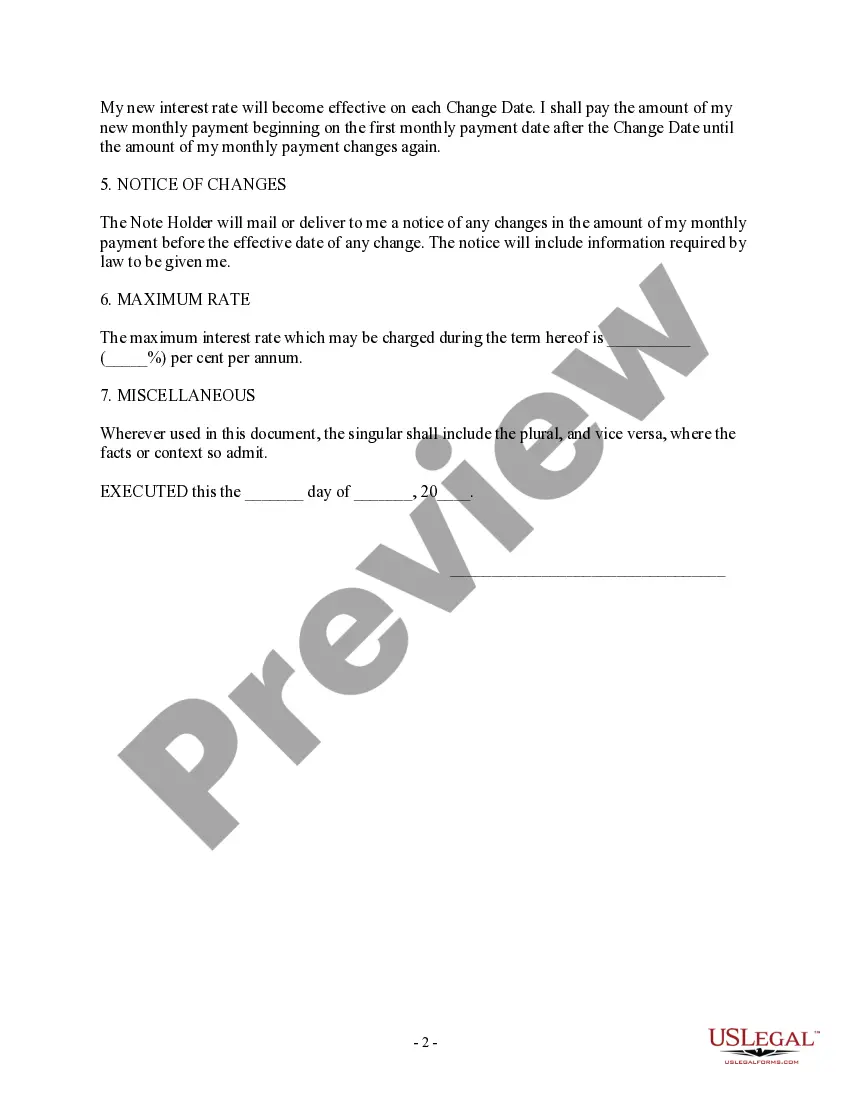

The Massachusetts Adjustable Rate Rider (also known as the Massachusetts ARM Rider or the Massachusetts Variable Rate Note) is a legal document that applies to adjustable-rate mortgage (ARM) loans in the state of Massachusetts. It is an essential component of the mortgage agreement, specifically detailing the terms and conditions of the variable interest rate associated with the loan. The Massachusetts Adjustable Rate Rider — Variable Rate Note outlines the initial interest rate, as well as the periodic adjustments that may occur throughout the loan term. With an adjustable-rate mortgage, the interest rate fluctuates over time, typically based on an index such as the U.S. Treasury rates or the London Interbank Offered Rate (LIBOR). The key features of the Massachusetts Adjustable Rate Rider — Variable Rate Note include: 1. Initial Rate: This section specifies the starting interest rate of the mortgage, which is typically lower than the prevailing fixed-rate mortgage at the time. It is often referred to as the "teaser rate" as it lures borrowers with lower monthly payments initially. 2. Adjustment Period: This clause details how frequently the interest rate can be adjusted after the initial fixed-rate period expires. Common adjustment periods are one, three, five, or seven years. For example, a 5/1 ARM means the rate will adjust once every year after the first five years. 3. Index: It provides information about the financial index that is used to calculate the adjusted interest rate. The Massachusetts ARM Rider can specify which specific index is being utilized, ensuring transparency in the borrower-lender relationship. 4. Margin: The margin represents the fixed percentage that is added to the chosen index to determine the new interest rate. For instance, if the index value is 3% and the margin is 2%, the resulting interest rate would be 5%. 5. Rate Caps: This section limits the extent to which the interest rate can fluctuate during each adjustment period or over the life of the loan. For example, the note may state that the rate cannot increase by more than 2% per adjustment period or 6% over the term of the loan. 6. Negative Amortization: The ARM Rider may address the possibility of negative amortization, which occurs when the monthly payment is insufficient to cover the interest and the unpaid amount is added to the principal balance. Rules surrounding negative amortization will be defined to prevent its occurrence or limit the extent of potential negative impact. It is important to note that there may be different variations or types of the Massachusetts Adjustable Rate Rider or Variable Rate Note, including specific provisions tailored to different loan products or lenders' requirements. However, the main goal of these documents remains consistent — to establish a clear framework for adjusting the interest rate on an ARM loan while protecting the rights of both the borrower and the lender.

Massachusetts Adjustable Rate Rider - Variable Rate Note

Description

How to fill out Massachusetts Adjustable Rate Rider - Variable Rate Note?

It is possible to spend hours on-line attempting to find the lawful document web template that suits the federal and state requirements you want. US Legal Forms offers a large number of lawful types which are evaluated by specialists. It is simple to acquire or produce the Massachusetts Adjustable Rate Rider - Variable Rate Note from the support.

If you already have a US Legal Forms profile, you are able to log in and then click the Download button. Next, you are able to total, revise, produce, or indication the Massachusetts Adjustable Rate Rider - Variable Rate Note. Each and every lawful document web template you purchase is your own property forever. To have one more copy of the bought form, check out the My Forms tab and then click the related button.

If you use the US Legal Forms internet site the first time, adhere to the straightforward recommendations below:

- Initial, be sure that you have chosen the best document web template for your area/town that you pick. Browse the form information to ensure you have selected the proper form. If accessible, use the Review button to check from the document web template at the same time.

- If you would like discover one more version from the form, use the Lookup discipline to obtain the web template that meets your requirements and requirements.

- When you have identified the web template you want, just click Buy now to carry on.

- Pick the rates prepare you want, type your references, and sign up for your account on US Legal Forms.

- Comprehensive the transaction. You should use your charge card or PayPal profile to pay for the lawful form.

- Pick the format from the document and acquire it to your system.

- Make alterations to your document if required. It is possible to total, revise and indication and produce Massachusetts Adjustable Rate Rider - Variable Rate Note.

Download and produce a large number of document themes while using US Legal Forms website, that offers the greatest variety of lawful types. Use skilled and express-specific themes to tackle your company or individual requirements.