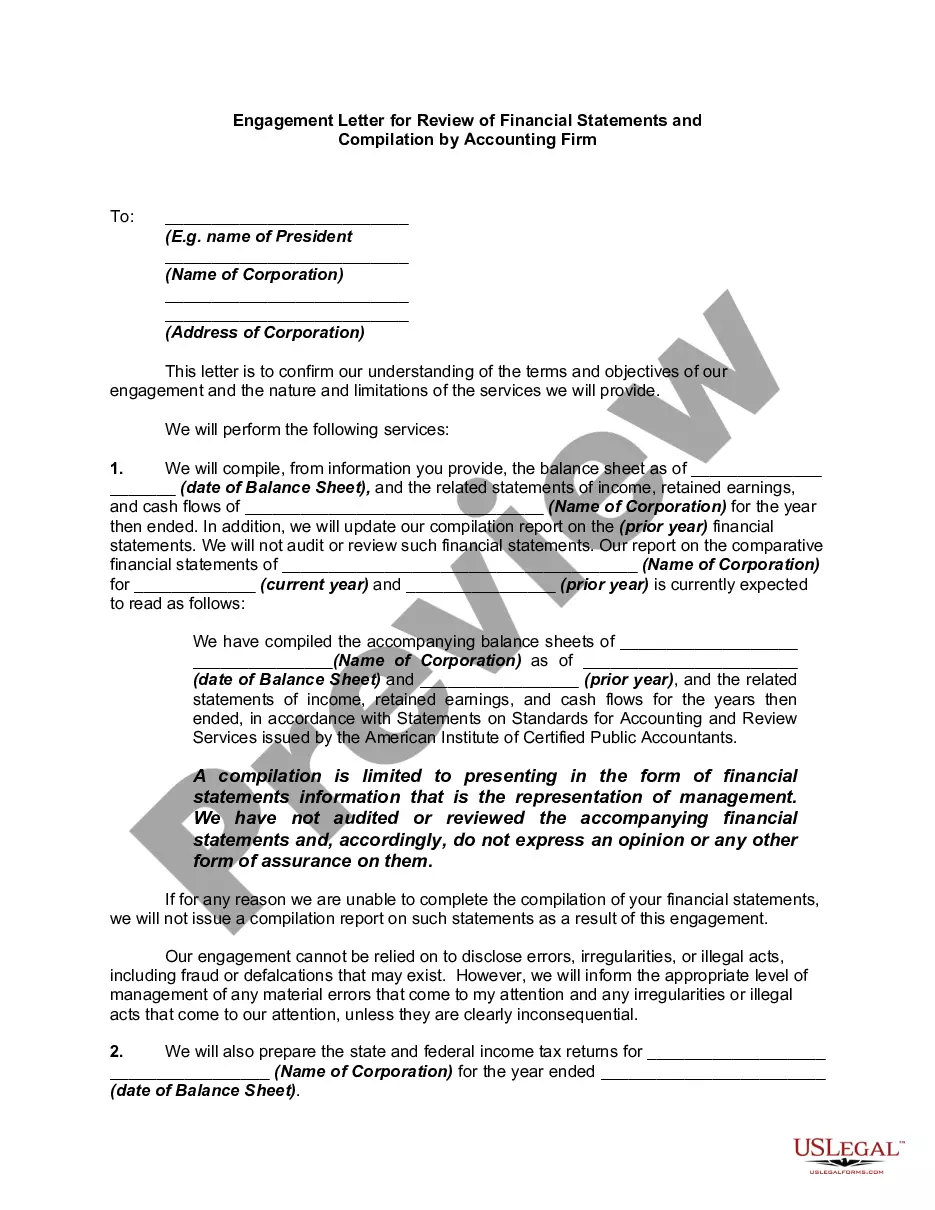

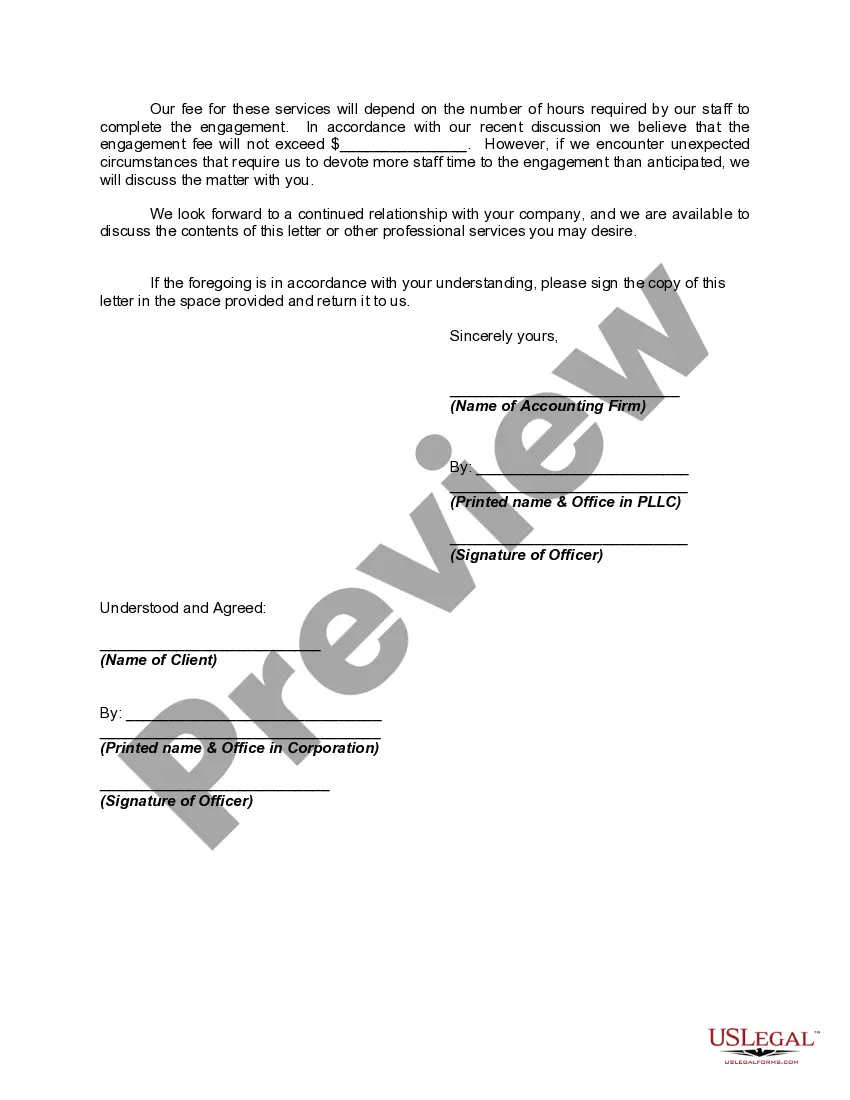

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Massachusetts Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm: Key Elements and Types In Massachusetts, an Engagement Letter for Review of Financial Statements and Compilation is a vital document that outlines the terms and conditions between an accounting firm and its clients. It establishes a formal agreement regarding the review and compilation services to be provided by the firm. This letter serves as a crucial communication tool and helps establish a clear understanding of the scope and objectives of the engagement. The key elements typically included in a Massachusetts Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm are: 1. Introduction: The letter begins with an introduction, stating the names and addresses of both the accounting firm and the client. It may also mention the effective date of the engagement. 2. Services to be Performed: This section provides a detailed description of the specific services to be performed by the accounting firm. It includes a clear differentiation between review and compilation services, as these are distinct procedures regulated by specific professional standards. 3. Financial Statements: The letter specifies the financial statements that will be reviewed or compiled, such as balance sheets, income statements, cash flow statements, and related notes. It may also indicate the applicable accounting framework, such as Generally Accepted Accounting Principles (GAAP) or another appropriate basis of accounting. 4. Responsibilities of the Parties: This section outlines the responsibilities of both the accounting firm and the client. It describes the client's duty to provide accurate and complete financial records and disclose all relevant information. It also highlights the accounting firm's obligation to maintain independence, perform the engagement in accordance with applicable standards, and maintain confidentiality. 5. Deadlines and Deliverables: The letter includes agreed-upon deadlines for providing the reviewed or compiled financial statements to the client. It may also specify any additional reports or deliverables required. 6. Fee Structure: The letter details the fee structure for the services provided, including hourly rates, fixed fees, or any other agreed-upon pricing arrangement. It may also mention any additional costs or expenses that will be billed separately. 7. Limitations of Engagement: This section defines the limitations of the engagement. It clarifies that a review engagement provides limited assurance rather than an audit's reasonable assurance. It may also specify any restrictions on the use or distribution of the financial statements. 8. Termination: The engagement letter may include provisions for termination, clarifying the circumstances under which either party may end the engagement. Different types of Massachusetts Engagement Letters for Review of Financial Statements and Compilation by Accounting Firm may include specialized engagements tailored to specific industries, such as healthcare, manufacturing, or non-profit organizations. These industry-specific letters may contain additional requirements, disclosures, or engagement procedures to address unique accounting and reporting considerations. It is important to note that while an Engagement Letter for Review of Financial Statements and Compilation is commonly used, engaging an accounting firm's services does not automatically guarantee compliance with all regulatory requirements. Businesses should consult with legal and accounting professionals to ensure their specific needs are met and that all applicable rules and regulations are adhered to.Massachusetts Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm: Key Elements and Types In Massachusetts, an Engagement Letter for Review of Financial Statements and Compilation is a vital document that outlines the terms and conditions between an accounting firm and its clients. It establishes a formal agreement regarding the review and compilation services to be provided by the firm. This letter serves as a crucial communication tool and helps establish a clear understanding of the scope and objectives of the engagement. The key elements typically included in a Massachusetts Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm are: 1. Introduction: The letter begins with an introduction, stating the names and addresses of both the accounting firm and the client. It may also mention the effective date of the engagement. 2. Services to be Performed: This section provides a detailed description of the specific services to be performed by the accounting firm. It includes a clear differentiation between review and compilation services, as these are distinct procedures regulated by specific professional standards. 3. Financial Statements: The letter specifies the financial statements that will be reviewed or compiled, such as balance sheets, income statements, cash flow statements, and related notes. It may also indicate the applicable accounting framework, such as Generally Accepted Accounting Principles (GAAP) or another appropriate basis of accounting. 4. Responsibilities of the Parties: This section outlines the responsibilities of both the accounting firm and the client. It describes the client's duty to provide accurate and complete financial records and disclose all relevant information. It also highlights the accounting firm's obligation to maintain independence, perform the engagement in accordance with applicable standards, and maintain confidentiality. 5. Deadlines and Deliverables: The letter includes agreed-upon deadlines for providing the reviewed or compiled financial statements to the client. It may also specify any additional reports or deliverables required. 6. Fee Structure: The letter details the fee structure for the services provided, including hourly rates, fixed fees, or any other agreed-upon pricing arrangement. It may also mention any additional costs or expenses that will be billed separately. 7. Limitations of Engagement: This section defines the limitations of the engagement. It clarifies that a review engagement provides limited assurance rather than an audit's reasonable assurance. It may also specify any restrictions on the use or distribution of the financial statements. 8. Termination: The engagement letter may include provisions for termination, clarifying the circumstances under which either party may end the engagement. Different types of Massachusetts Engagement Letters for Review of Financial Statements and Compilation by Accounting Firm may include specialized engagements tailored to specific industries, such as healthcare, manufacturing, or non-profit organizations. These industry-specific letters may contain additional requirements, disclosures, or engagement procedures to address unique accounting and reporting considerations. It is important to note that while an Engagement Letter for Review of Financial Statements and Compilation is commonly used, engaging an accounting firm's services does not automatically guarantee compliance with all regulatory requirements. Businesses should consult with legal and accounting professionals to ensure their specific needs are met and that all applicable rules and regulations are adhered to.