An independent contractor is a person or business who performs services for another person pursuant to an agreement and who is not subject to the other's control, or right to control, the manner and means of performing the services. The exact nature of the independent contractor's relationship with the hiring party is important since an independent contractor pays his/her own Social Security, income taxes without payroll deduction, has no retirement or health plan rights, and often is not entitled to worker's compensation coverage. The traditional tests to determine whether a worker is an employee or independent contractor involve the concept of control. The Internal Revenue Service (IRS) developed 20 factors used to determine whether a worker is an independent contractor under the common law. A "yes" answer to any of these questions would be evidence of an employer-employee relationship.

" Does the principal provide instructions to the worker about when, where, and how he or she is to perform the work?

" Does the principal provide training to the worker?

" Are the services provided by the worker integrated into the principal's business operations?

" Must the services be rendered personally by the worker?

" Does the principal hire, supervise and pay assistants to the worker?

" Is there a continuing relationship between the principal and the worker?

" Does the principal set the work hours and schedule?

" Does the worker devote substantially full time to the business of the principal?

" Is the work performed on the principal's premises?

" Is the worker required to perform the services in an order or sequence set by the principal?

" Is the worker required to submit oral or written reports to the principal?

" Is the worker paid by the hour, week, or month?

" Does the principal have the right to discharge the worker at will?

" Can the worker terminate his or her relationship with the principal any time he or she wishes without incurring liability to the principal?

" Does the principal pay the business or traveling expenses of the worker?

A "yes" answer to any of these questions would be evidence of an independent contractor relationship.

" Does the worker furnish significant tools, materials and equipment?

" Does the worker have a significant investment in facilities?

" Can the worker realize a profit or loss as a result of his or her services?

" Does the worker provide services for more than one firm at a time\

" Does the worker make his or her services available to the general public?

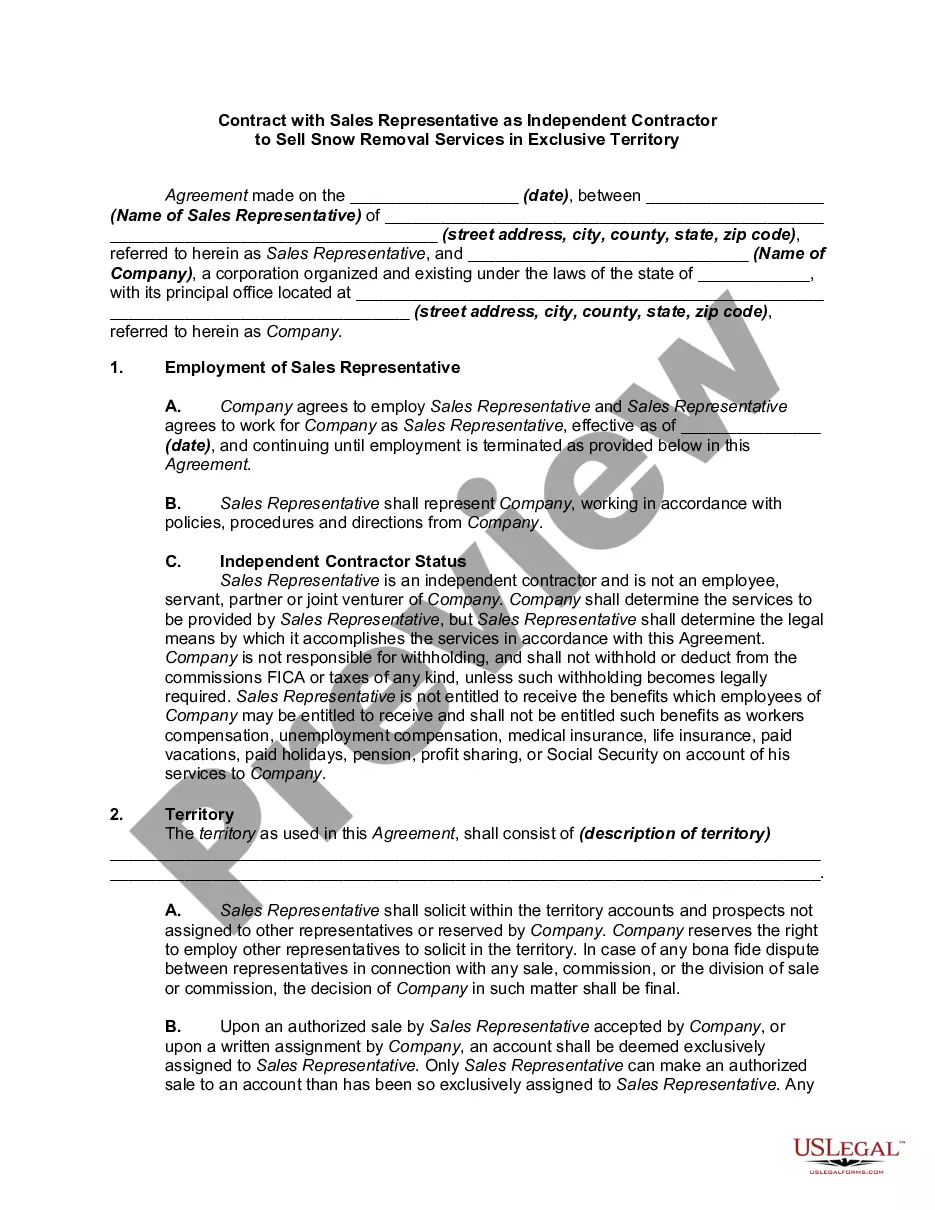

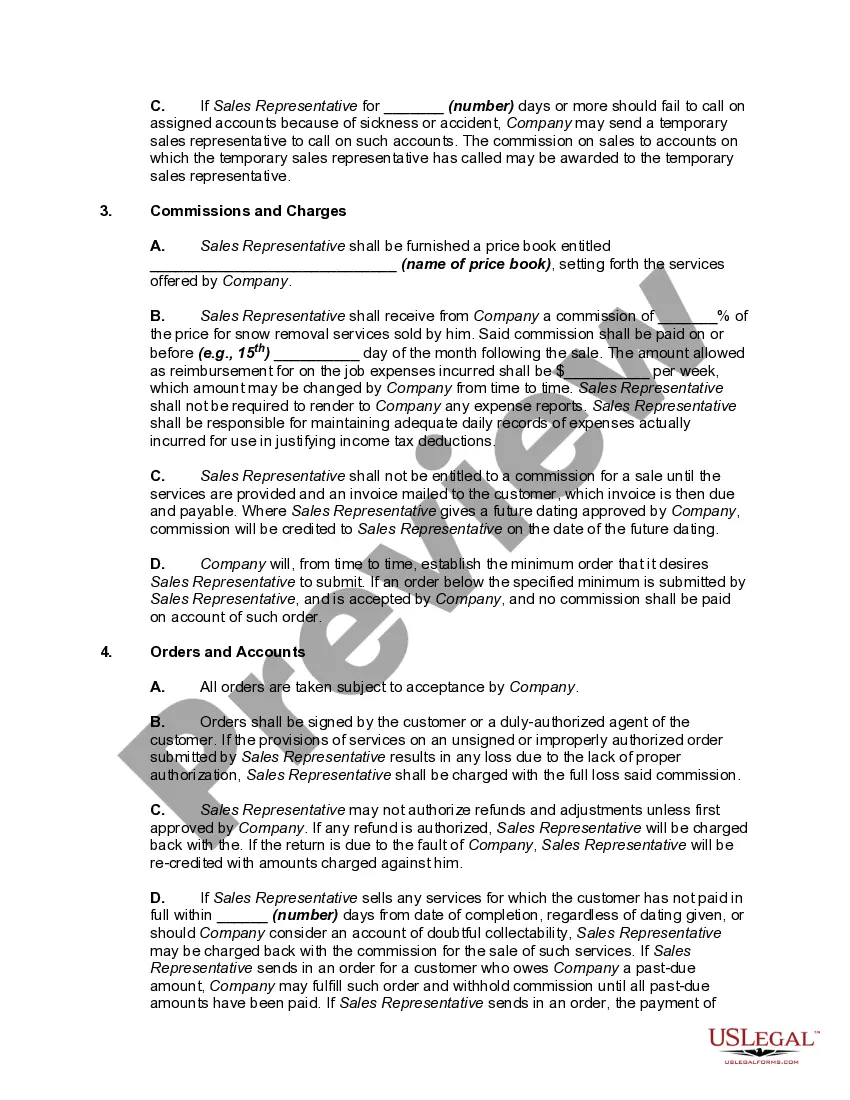

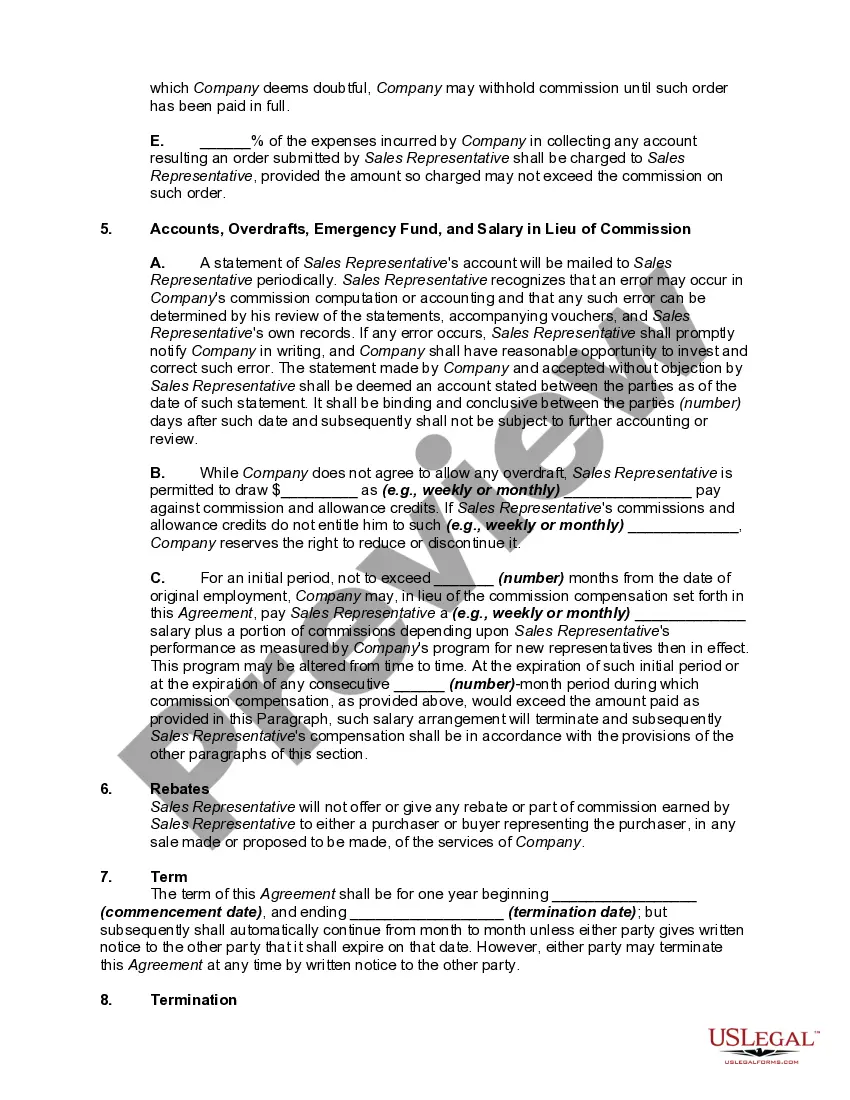

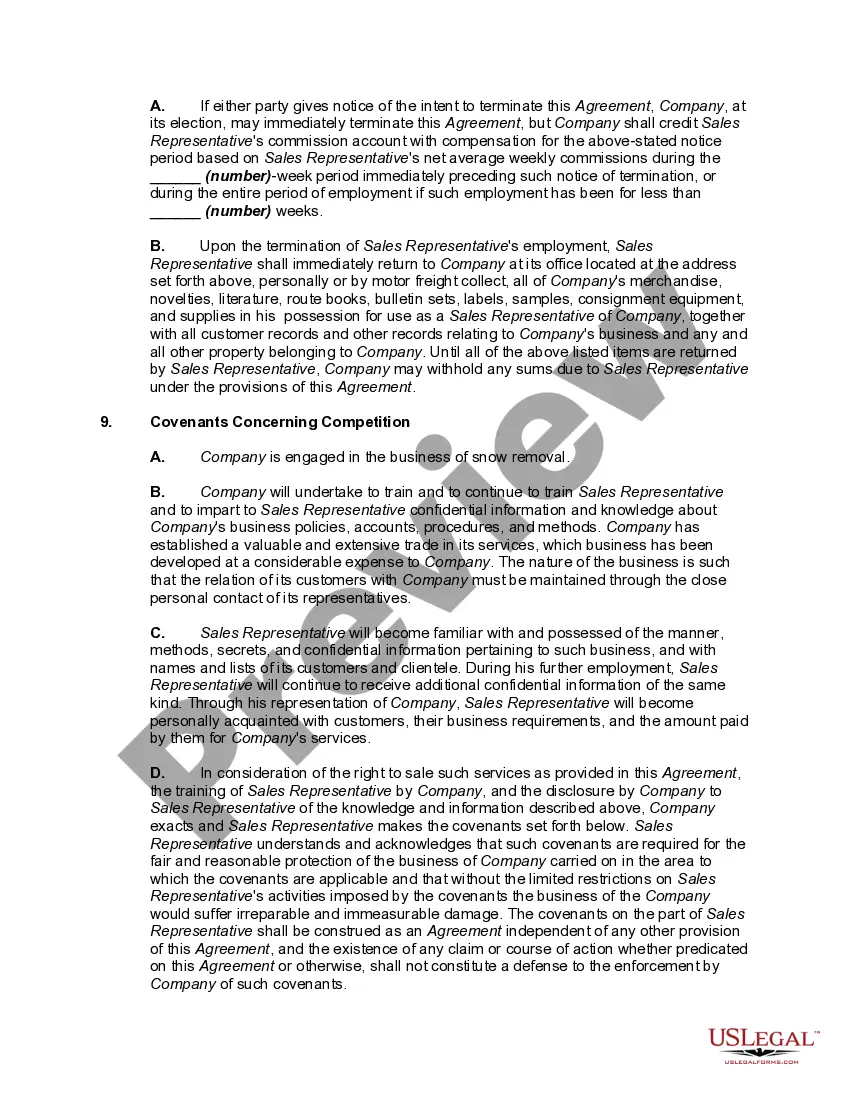

Title: Massachusetts Contract with Sales Representative as Independent Contractor to Sell Snow Removal Services in Exclusive Territory Keywords: Massachusetts, contract, sales representative, independent contractor, snow removal services, exclusive territory Introduction: In the state of Massachusetts, businesses often enter into contracts with sales representatives who work as independent contractors to assist them in expanding their reach and boosting sales. This article will discuss in detail the Massachusetts Contract with Sales Representative as Independent Contractor, focusing on its application in the snow removal services industry within an exclusive territory. 1. Massachusetts Independent Contractor Law: Under the Massachusetts Independent Contractor Law, businesses can engage sales representatives as independent contractors to sell their snow removal services. This law ensures that there is a clear understanding between the business and the sales representative regarding their relationship, responsibilities, and obligations. 2. Contract Structure: A typical Massachusetts Contract with Sales Representative as Independent Contractor to Sell Snow Removal Services in Exclusive Territory consists of the following elements: a. Agreement Term: The contract specifies the duration for which the agreement will be in effect, ensuring clarity and accountability on both sides. b. Exclusive Territory: The contract defines the specific geographic area in Massachusetts where the sales representative will operate and exclusively sell the snow removal services on behalf of the business. c. Sales Targets: The contract may include specific sales targets or goals that the independent contractor needs to achieve, ensuring transparency and performance expectations. d. Compensation Structure: The contract outlines how the sales representative will be compensated, whether it's through commission-based earnings, a fixed fee, or a combination of both. e. Non-Disclosure Agreement: To protect the business's interests, the contract may include a non-disclosure agreement prohibiting the sales representative from disclosing any confidential or proprietary information. 3. Types of Massachusetts Contracts for Snow Removal Services: a. Exclusive Territory Limitation: In this type of contract, the sales representative is granted exclusivity in a specific geographic area but may be restricted from selling snow removal services outside that territory. b. Non-Exclusive Territory Agreement: This contract allows the sales representative to sell snow removal services both within and outside a specified territory and might involve multiple independent contractors operating in the same area. c. Commission-Based Contract: This type of contract primarily focuses on compensating the sales representative based on a percentage of the sales they generate, encouraging them to actively promote the snow removal services within their exclusive territory. d. Retainer Contract: In some cases, a retainer agreement can be established where the sales representative receives a fixed payment for their services irrespective of the sales volume. Conclusion: Massachusetts contracts with sales representatives as independent contractors to sell snow removal services in an exclusive territory offer a mutually beneficial arrangement for both businesses and sales representatives. By clearly outlining the terms, responsibilities, exclusivity, and compensation structures, these contracts provide a framework for effective collaboration and expansion of sales within the snow removal services industry in Massachusetts.