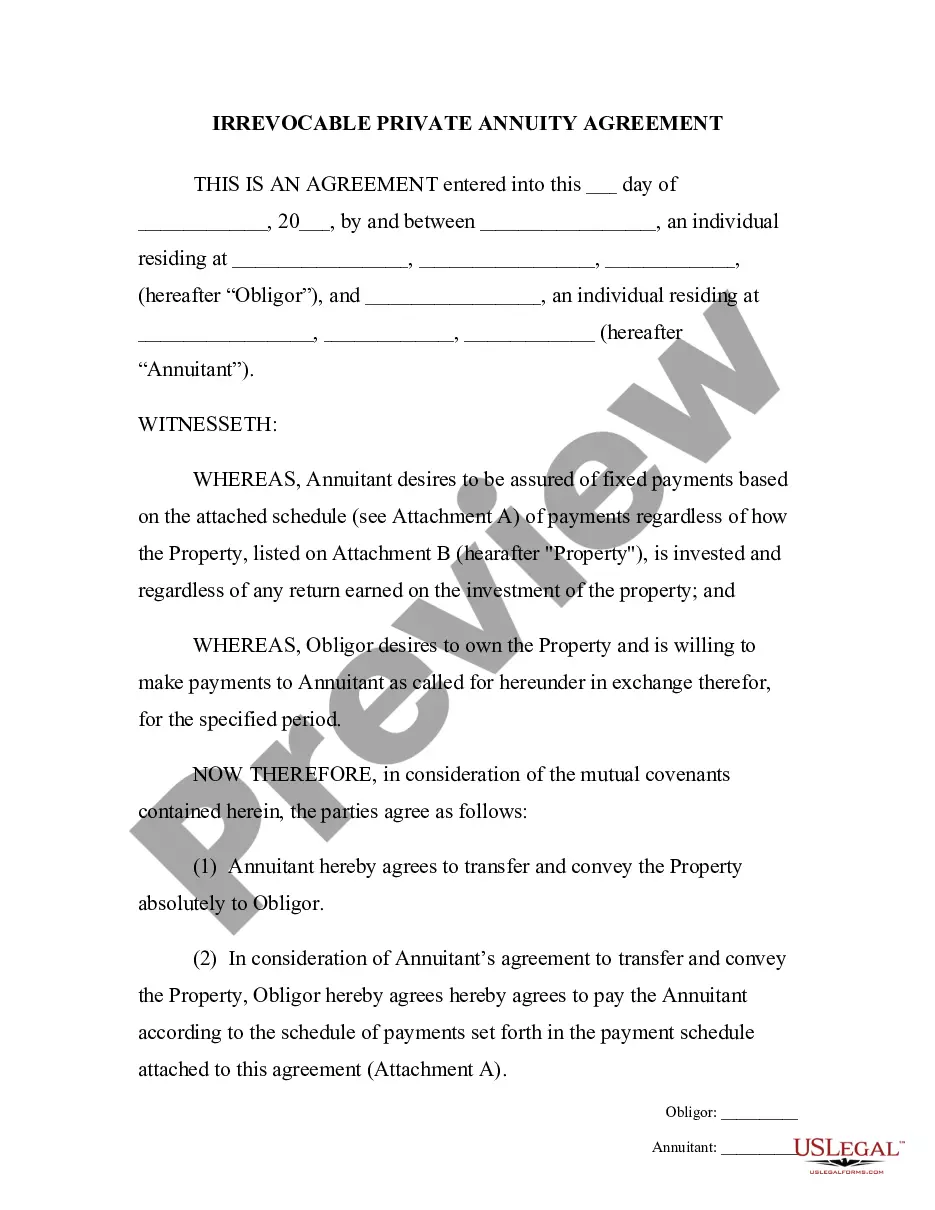

Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant

Description

How to fill out Private Annuity Agreement With Payments To Last For Life Of Annuitant?

US Legal Forms - one of the largest collections of valid documents in the United States - offers a broad selection of official document templates you can download or print.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can obtain the most recent versions of forms such as the Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant in just minutes.

Review the form information to confirm that you have selected the correct type.

If the form does not meet your needs, utilize the Search area at the top of the screen to find the one that does.

- If you already have a subscription, Log In to retrieve the Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant from the US Legal Forms library.

- The Download button will be visible on each form you view.

- You can access all previously downloaded forms in the My documents section of your account.

- If you want to use US Legal Forms for the first time, here are some simple instructions to get you started.

- Ensure that you have chosen the correct form for your region/state.

- Click the Preview button to check the form's details.

Form popularity

FAQ

The taxation of private annuities upon the death of the annuitant hinges on several factors, including the terms of the Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant. Generally, any remaining payments to beneficiaries may be subject to income tax. Consulting a tax professional can provide clarity and ensure compliance with relevant laws, as these situations can become complex.

After the death of the annuitant, annuity payments typically cease unless a death benefit or specific beneficiary provisions are included in the Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant. In cases where no beneficiary is designated, payments may stop entirely. Therefore, it's vital to understand your agreement and consider potential arrangements to provide for heirs.

The annuity that stops payment when the annuitant dies is primarily a life-only annuity. Within the framework of a Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant, this type ensures that payments are made only during the annuitant's lifetime. Once they pass, no further distributions are made, emphasizing the importance of planning for future financial needs.

A life annuity is the type of arrangement that ceases payments upon the annuitant's death. This arrangement aligns with a Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant, targeting the lifetime of the individual. Upon the annuitant's passing, the payments end, leaving no further benefits for heirs unless specified otherwise. Understanding these terms helps in planning your financial future.

The settlement option where payments stop at the annuitant's death is typically referred to as a life-only annuity. In the context of a Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant, this option provides income solely for the life of the annuitant. Once they pass away, no additional payments are made. This can be an important consideration when choosing an annuity.

When an annuitant dies, the fate of the annuity depends on the specific terms outlined in the Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant. Generally, if the annuity is structured as a lifetime payment plan, payments cease upon the annuitant's death. However, some agreements may include provisions for a beneficiary to receive payments. Therefore, reviewing the contract details is crucial.

A longevity annuity contract is a financial product that guarantees income for the lifetime of the annuitant, providing peace of mind in retirement. Specifically, a Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant ensures that you will receive consistent payments, helping you manage expenses and plan for the future. This type of contract can be a vital component of your retirement strategy, especially as it addresses the risk of outliving your savings. With platforms like uslegalforms, you can easily set up a Massachusetts Private Annuity Agreement tailored to your needs.

Annuity payments for a life annuity are typically based on several factors, including the annuitant's age, gender, and life expectancy. Insurance companies use these factors to calculate the monthly payment amount, ensuring it aligns with the risk of longevity. This calculation provides a structured income stream throughout the annuitant's life while reflecting their unique circumstances. A Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant can facilitate this process, tailoring payments to individual needs.

The straight life annuity option is designed specifically for providing lifetime payments to the annuitant. This option pays fixed amounts for the rest of the annuitant's life, ensuring a reliable income source. While it does not offer benefits to beneficiaries after the annuitant’s passing, it focuses solely on maximizing the annuitant's lifetime income. Consider how a Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant can help you secure a consistent financial future.

A lifetime payout annuity is a financial product that guarantees payments to the annuitant for the duration of their life. This type of annuity provides financial security by ensuring that individuals do not outlive their resources. It is particularly useful for retirement planning, as it provides a steady income stream. A Massachusetts Private Annuity Agreement with Payments to Last for Life of Annuitant can help you establish this kind of arrangement.