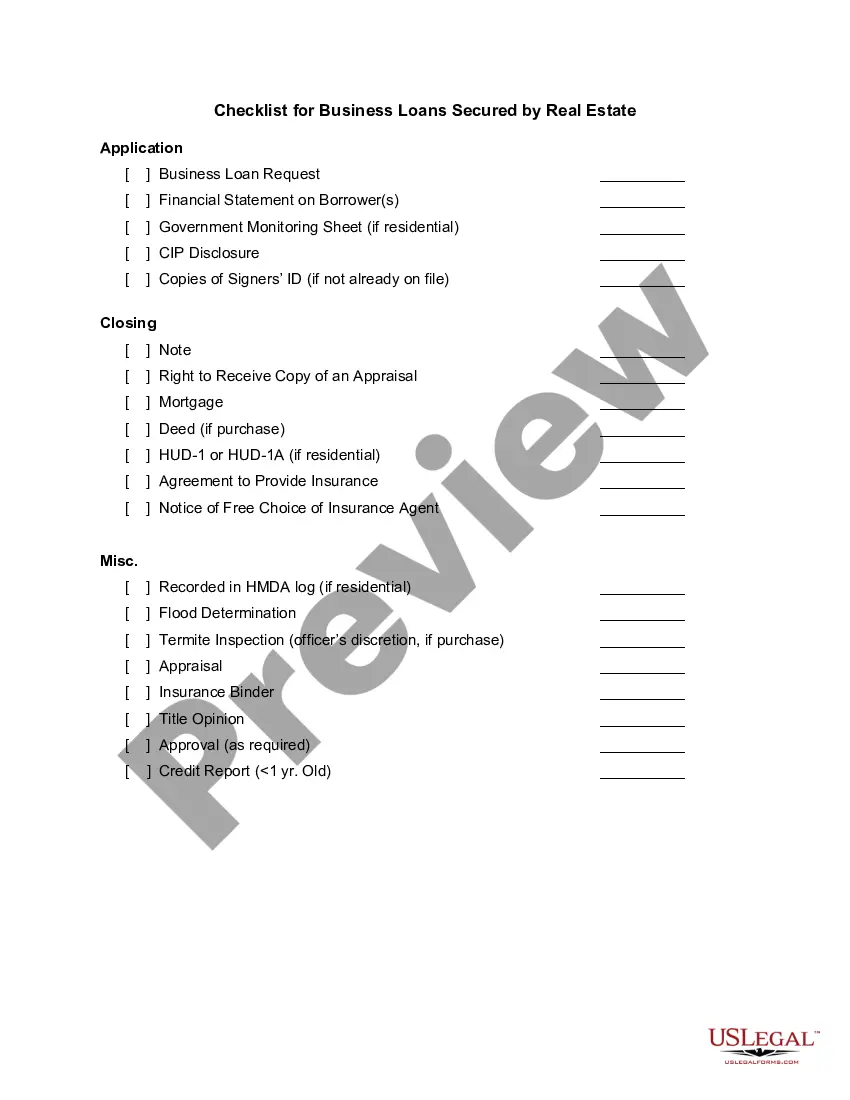

Massachusetts Checklist for Business Loans Secured by Real Estate — A Detailed Description When seeking a business loan in Massachusetts that is secured by real estate, it is crucial for borrowers to be well-prepared and aware of the necessary requirements. Understanding the checklist of requirements can help expedite the loan approval process and increase the chances of securing the desired financing. Here is a detailed description of the Massachusetts Checklist for Business Loans Secured by Real Estate: 1. Complete Loan Application: Begin by filling out a comprehensive loan application form provided by the lender. This form collects essential information about the borrower, the business, and the collateral property. 2. Business Plan: Submit a well-structured business plan that outlines the company's goals, financial projections, industry analysis, and marketing strategies. This document signifies the borrower's commitment and vision for the business. 3. Personal and Business Financial Statements: Prepare and provide up-to-date personal and business financial statements. These statements should demonstrate the borrower's financial stability and capacity to repay the loan. Include income statements, balance sheets, and cash flow statements for both personal and business finances. 4. Credit History and Score: Provide a detailed credit history report from all three major credit bureaus. Aim for a good credit score as it validates the borrower's creditworthiness and ability to handle debt responsibly. A credit score of at least 650 is recommended. 5. Collateral Valuation: Conduct an appraisal of the real estate property that will serve as collateral. The appraisal should be carried out by a licensed and certified appraiser. The lender will evaluate the property's value to determine the loan amount to be extended. 6. Title Search and Insurance: Perform a title search to ensure that the property has a clear title without any liens or legal encumbrances. Acquire title insurance to protect against any unforeseen title-related issues. 7. Environmental Assessment: If applicable, conduct an environmental assessment or Phase I Environmental Site Assessment (ESA) to identify potential environmental liabilities associated with the property. This helps mitigate risks for both the lender and the borrower. 8. Property Insurance: Obtain property insurance coverage to safeguard against potential damages, natural disasters, theft, or any unexpected events that may cause harm to the collateral property. 9. Legal Documents: Prepare and provide legal documents such as contracts, leases, licenses, and permits, if required by the lender or specific to the business industry, to ensure compliance. 10. Business Experience and Resume: Include a comprehensive resume or curriculum vitae highlighting the borrower's professional experience, industry expertise, and relevant accomplishments. This adds credibility and reassures the lender about the borrower's ability to manage the business efficiently. Different Types of Massachusetts Checklist for Business Loans Secured by Real Estate: 1. Commercial Real Estate Loans: For borrowers seeking loans for commercial properties, such as office buildings, retail spaces, or industrial facilities, the aforementioned checklist generally applies. 2. Construction Loans: If the loan is intended for a construction project, additional documents such as architectural plans, construction contracts, and cost estimates may be required. 3. Residential Real Estate Loans: Borrowers seeking loans secured by residential properties, such as rental properties or multi-unit residences, might have specific requirements related to marketability, rental income, and maintenance history. 4. Bridge Loans: These short-term loans that "bridge" the gap between existing financing and a permanent loan may have slightly different requirements, emphasizing the borrower's exit strategy and proof of future permanent financing. By following the Massachusetts Checklist for Business Loans Secured by Real Estate and tailoring it to the specific loan type, borrowers can streamline the loan application process and increase their chances of successfully securing financing for their business ventures.

Massachusetts Checklist for Business Loans Secured by Real Estate

Description

How to fill out Massachusetts Checklist For Business Loans Secured By Real Estate?

Choosing the right legitimate record format can be quite a have a problem. Obviously, there are a lot of templates available on the Internet, but how can you get the legitimate form you want? Take advantage of the US Legal Forms internet site. The service gives thousands of templates, for example the Massachusetts Checklist for Business Loans Secured by Real Estate, that can be used for organization and private demands. Every one of the types are inspected by pros and satisfy state and federal needs.

In case you are already registered, log in in your bank account and click the Download button to find the Massachusetts Checklist for Business Loans Secured by Real Estate. Make use of bank account to appear from the legitimate types you possess ordered formerly. Check out the My Forms tab of the bank account and acquire one more backup in the record you want.

In case you are a fresh user of US Legal Forms, listed here are basic guidelines that you should adhere to:

- Very first, make sure you have chosen the appropriate form for your area/state. You can examine the shape utilizing the Preview button and look at the shape explanation to guarantee it is the best for you.

- If the form fails to satisfy your preferences, use the Seach area to get the correct form.

- Once you are certain that the shape is suitable, go through the Acquire now button to find the form.

- Opt for the rates strategy you want and type in the required information and facts. Create your bank account and buy an order using your PayPal bank account or bank card.

- Opt for the document file format and obtain the legitimate record format in your gadget.

- Complete, change and print out and indicator the attained Massachusetts Checklist for Business Loans Secured by Real Estate.

US Legal Forms will be the largest catalogue of legitimate types in which you can discover various record templates. Take advantage of the service to obtain appropriately-manufactured paperwork that adhere to status needs.