Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

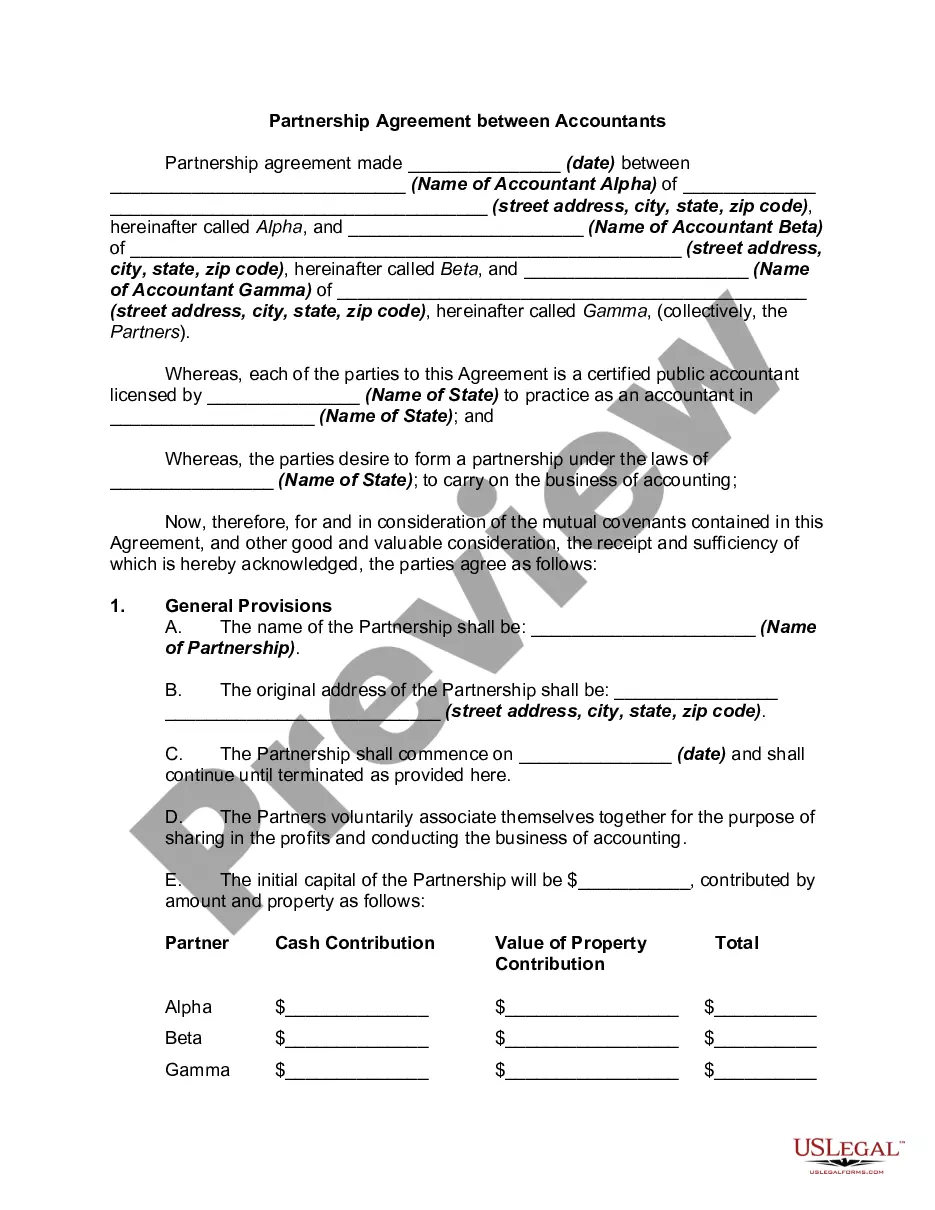

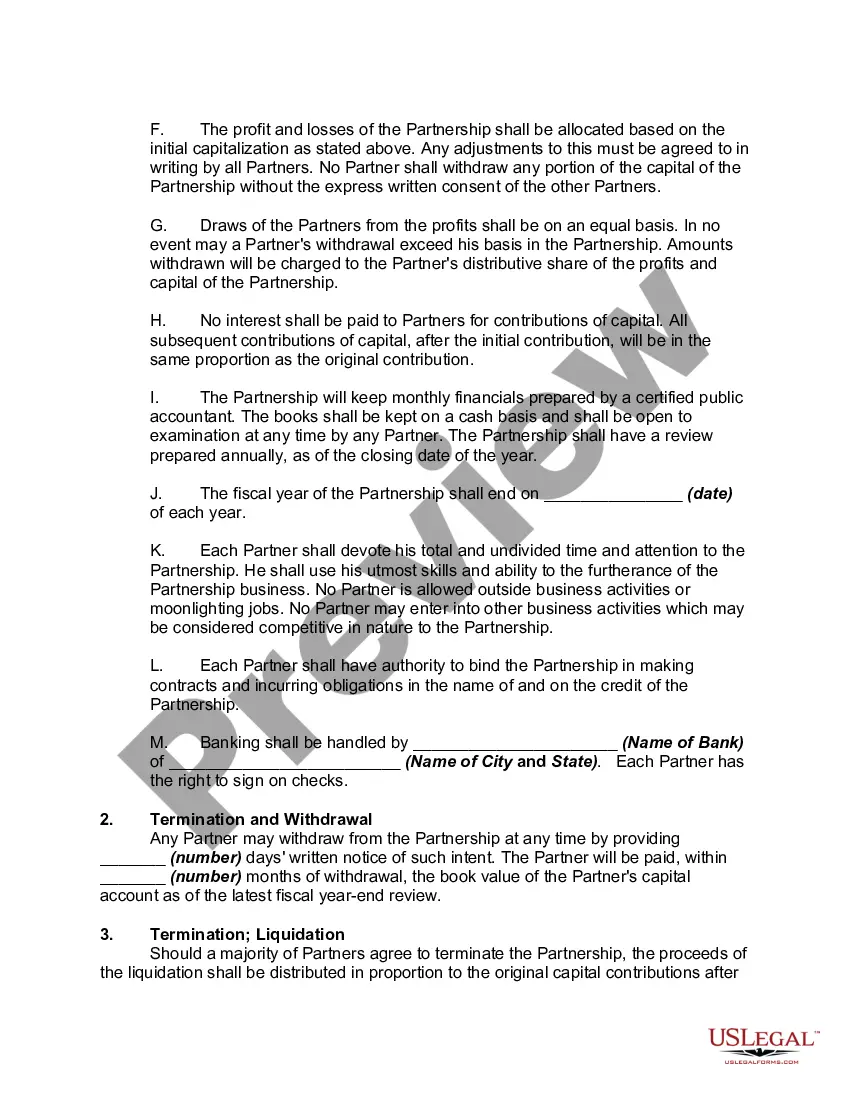

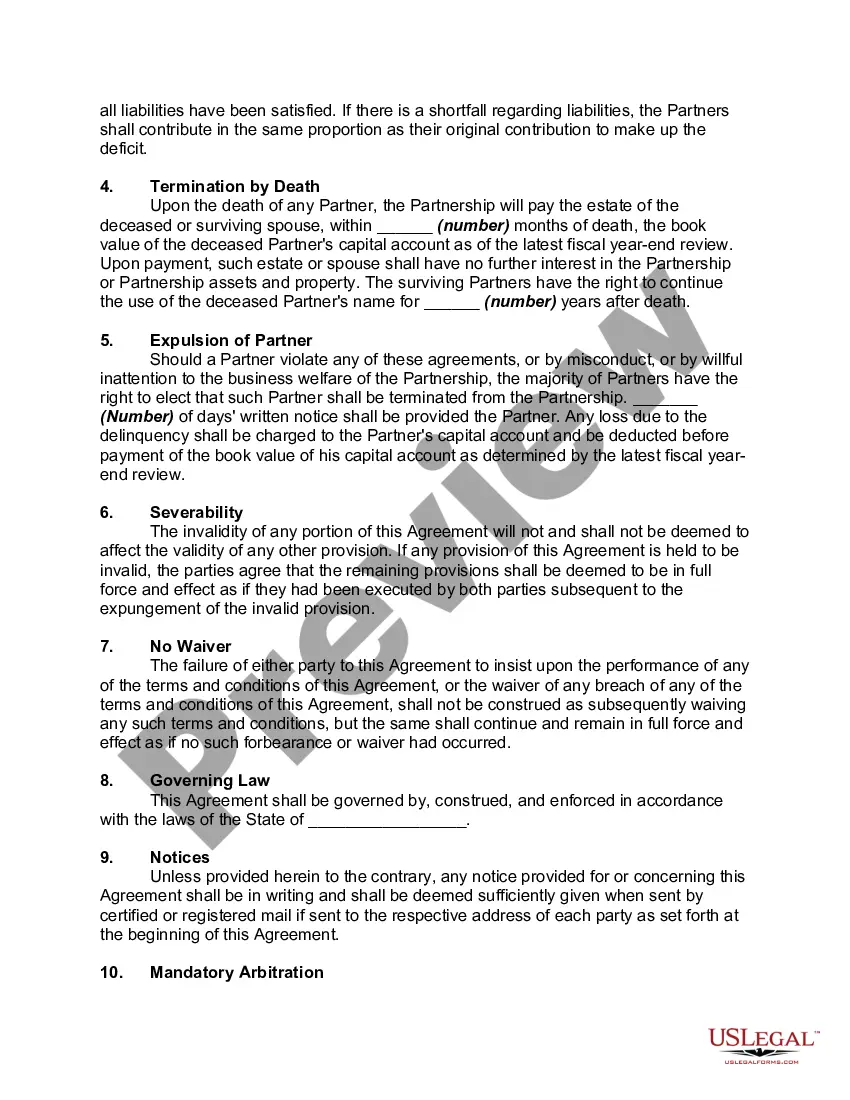

A Massachusetts Partnership Agreement between accountants is a legal document that outlines the terms and conditions agreed upon by two or more accountants who decide to form a partnership to operate their accounting practice in Massachusetts. This partnership agreement serves as a guideline for the partners, providing clarity on the rights, responsibilities, and obligations of each partner, as well as the rules governing the partnership. In Massachusetts, there are various types of Partnership Agreements between accountants, which include: 1. General Partnership Agreement: This is the most common type of partnership agreement among accountants in Massachusetts. In a general partnership, all partners contribute capital, share profits, losses, and liabilities equally, and participate in the decision-making process of the accounting practice. 2. Limited Partnership Agreement: A limited partnership agreement in Massachusetts allows for the formation of a partnership where there are both general partners and limited partners. General partners have unlimited liability, participate in the management of the business, and share profits and losses equally. Limited partners, on the other hand, contribute capital but have limited liability and no management authority. 3. Limited Liability Partnership (LLP) Agreement: This type of partnership agreement provides protection to the partners' personal assets against business liabilities. In Massachusetts, accountants can form an LLP to limit personal liability for the negligence or misconduct of other partners. Each partner remains personally liable for their own actions, but not for the actions of other partners in the partnership. 4. Professional Corporation Partnership Agreement: For accountants who wish to form a partnership but also want the added protection of incorporating, they can establish a professional corporation partnership. This structure allows accountants to enjoy liability protection while practicing as a partnership under specific regulations set by the Massachusetts Board of Public Accountancy. Keywords: Massachusetts, partnership agreement, accountants, general partnership, limited partnership, limited liability partnership, LLP, professional corporation partnership, rights, responsibilities, obligations, profits, losses, liabilities, decision-making, capital, unlimited liability, management authority, personal assets, personal liability, negligence, misconduct, incorporation, regulations, Massachusetts Board of Public Accountancy.A Massachusetts Partnership Agreement between accountants is a legal document that outlines the terms and conditions agreed upon by two or more accountants who decide to form a partnership to operate their accounting practice in Massachusetts. This partnership agreement serves as a guideline for the partners, providing clarity on the rights, responsibilities, and obligations of each partner, as well as the rules governing the partnership. In Massachusetts, there are various types of Partnership Agreements between accountants, which include: 1. General Partnership Agreement: This is the most common type of partnership agreement among accountants in Massachusetts. In a general partnership, all partners contribute capital, share profits, losses, and liabilities equally, and participate in the decision-making process of the accounting practice. 2. Limited Partnership Agreement: A limited partnership agreement in Massachusetts allows for the formation of a partnership where there are both general partners and limited partners. General partners have unlimited liability, participate in the management of the business, and share profits and losses equally. Limited partners, on the other hand, contribute capital but have limited liability and no management authority. 3. Limited Liability Partnership (LLP) Agreement: This type of partnership agreement provides protection to the partners' personal assets against business liabilities. In Massachusetts, accountants can form an LLP to limit personal liability for the negligence or misconduct of other partners. Each partner remains personally liable for their own actions, but not for the actions of other partners in the partnership. 4. Professional Corporation Partnership Agreement: For accountants who wish to form a partnership but also want the added protection of incorporating, they can establish a professional corporation partnership. This structure allows accountants to enjoy liability protection while practicing as a partnership under specific regulations set by the Massachusetts Board of Public Accountancy. Keywords: Massachusetts, partnership agreement, accountants, general partnership, limited partnership, limited liability partnership, LLP, professional corporation partnership, rights, responsibilities, obligations, profits, losses, liabilities, decision-making, capital, unlimited liability, management authority, personal assets, personal liability, negligence, misconduct, incorporation, regulations, Massachusetts Board of Public Accountancy.