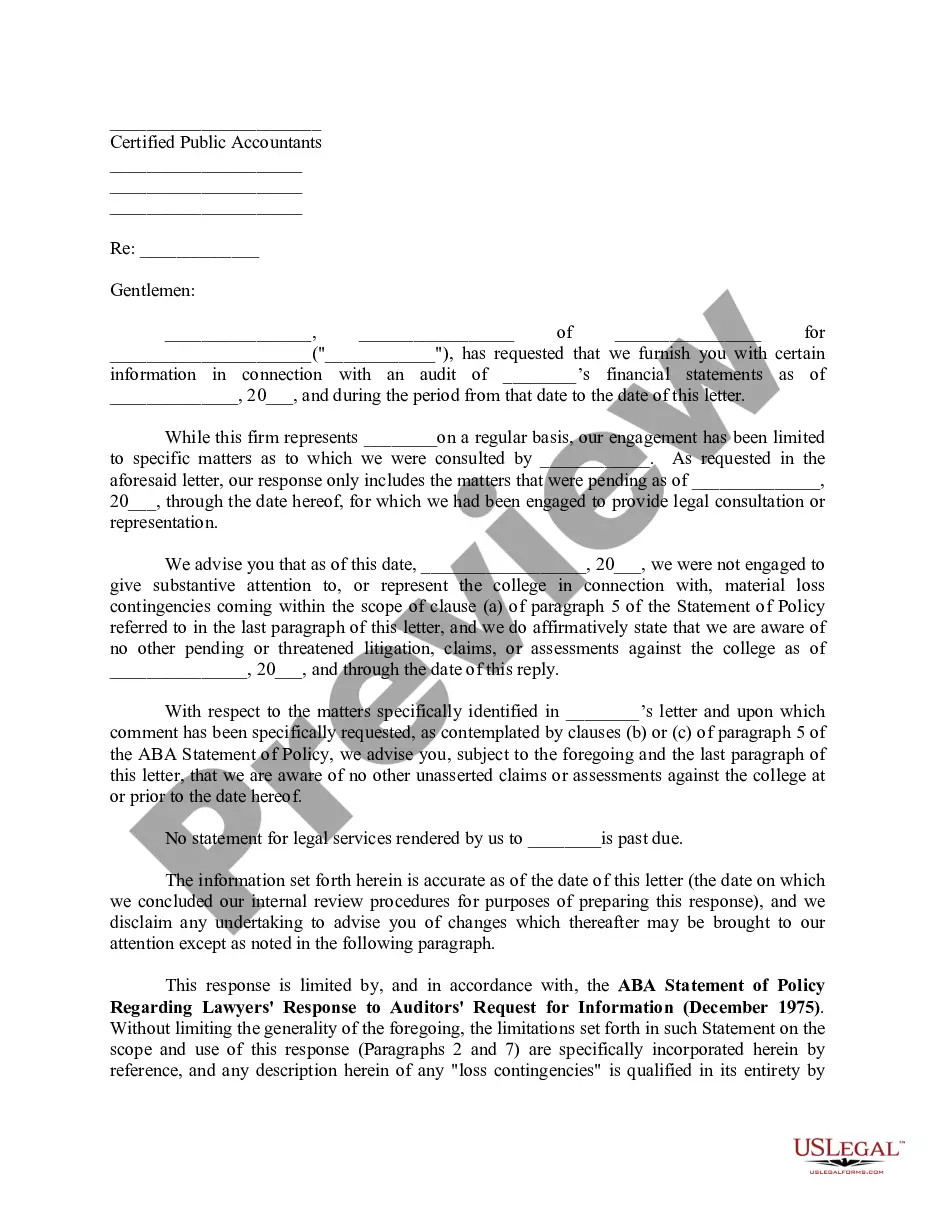

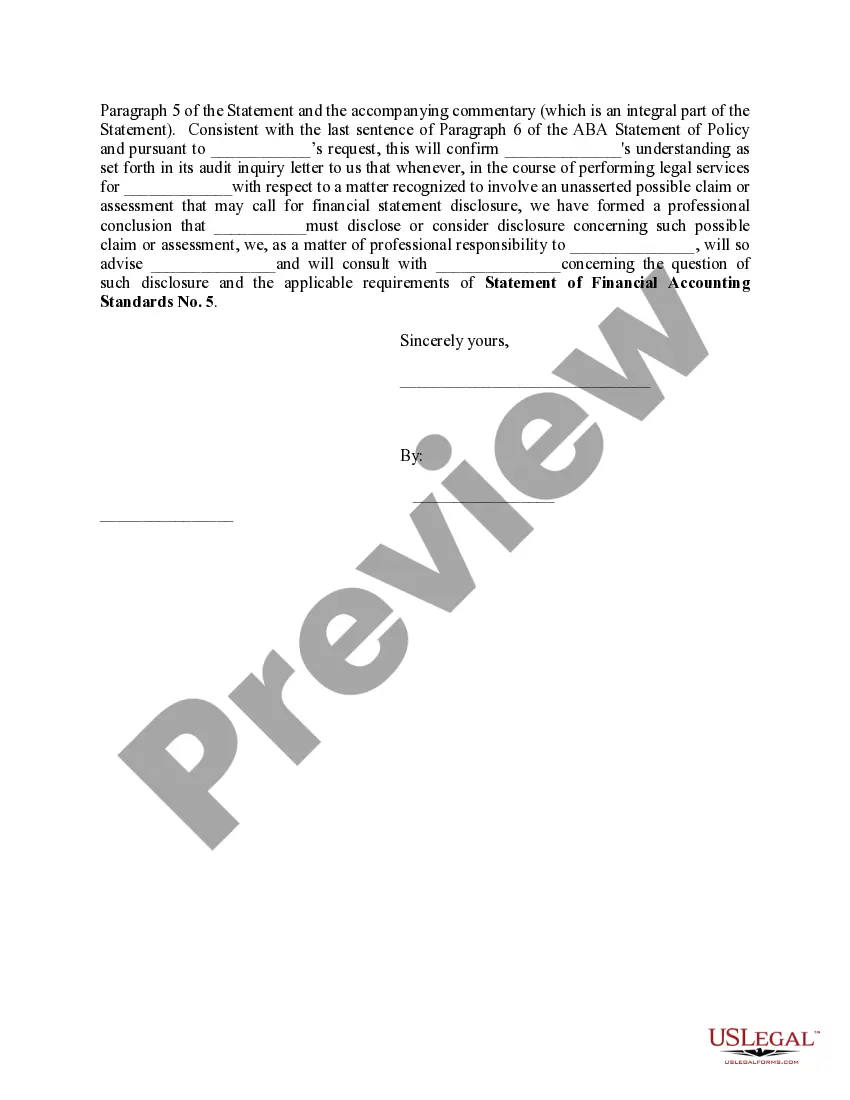

The Massachusetts Model Letter Accountants to Auditors is a standardized communication tool used in the accounting industry to facilitate effective communication between accountants and auditors working on a particular project or engagement. This model letter is specifically designed to comply with the regulations and guidelines set forth by the Massachusetts Board of Public Accountancy. In Massachusetts, there are various types of model letters used by accountants to communicate with auditors based on different scenarios. Some commonly recognized types include: 1. Audit Engagement Letter: This type of model letter is used when an accountant engages an auditor to perform an audit of a client's financial statements. It outlines the terms, responsibilities, and scope of the audit engagement, including the timeframe, fee structure, and reporting requirements. 2. Review Engagement Letter: When an accountant wishes to engage an auditor to perform a review of a client's financial statements, a review engagement letter is used. This model letter defines the purpose, limitations, and responsibilities of both parties involved in the review engagement process. 3. Compilation Engagement Letter: In cases where an accountant prepares financial statements for a client without the intention of giving an assurance opinion, a compilation engagement letter is used. This letter clearly defines the scope and limitations of the compilation engagement, highlighting that no audit or review procedures have been performed. 4. Agreed-Upon Procedures Engagement Letter: This type of model letter is used when an accountant engages an auditor to perform specific procedures on financial information based on an agreed-upon set of terms. The procedures may vary depending on the specific requirements of the client or project, and the letter outlines these procedures and associated responsibilities. The Massachusetts Model Letter Accountants to Auditors serves as a valuable communication mechanism to ensure clarity, mutual understanding, and compliance with the professional standards and regulations established by the Massachusetts Board of Public Accountancy. It helps foster transparency, professionalism, and effective collaboration between accountants and auditors, ultimately enhancing the integrity of financial reporting and decision-making processes for organizations based in Massachusetts.

Massachusetts Model Letter Accountants To Auditors

Description

How to fill out Massachusetts Model Letter Accountants To Auditors?

Choosing the best authorized record design can be a have difficulties. Of course, there are a lot of templates available online, but how can you find the authorized form you want? Utilize the US Legal Forms web site. The support gives thousands of templates, such as the Massachusetts Model Letter Accountants To Auditors, which you can use for enterprise and personal needs. Every one of the forms are checked by pros and satisfy state and federal requirements.

Should you be previously registered, log in in your account and then click the Download option to have the Massachusetts Model Letter Accountants To Auditors. Use your account to look from the authorized forms you possess ordered previously. Proceed to the My Forms tab of your own account and obtain yet another copy in the record you want.

Should you be a brand new consumer of US Legal Forms, listed below are straightforward directions for you to adhere to:

- First, make certain you have chosen the correct form for the metropolis/region. It is possible to look through the form making use of the Preview option and read the form explanation to make sure it will be the right one for you.

- If the form does not satisfy your preferences, utilize the Seach discipline to discover the appropriate form.

- When you are positive that the form is acceptable, select the Acquire now option to have the form.

- Opt for the prices prepare you desire and enter in the needed info. Make your account and buy an order with your PayPal account or Visa or Mastercard.

- Pick the submit format and obtain the authorized record design in your device.

- Total, change and print and indication the received Massachusetts Model Letter Accountants To Auditors.

US Legal Forms is definitely the biggest library of authorized forms in which you can find various record templates. Utilize the service to obtain expertly-created papers that adhere to state requirements.