Massachusetts Joint Trust with Income Payable to Trustors During Joint Lives

Description

How to fill out Joint Trust With Income Payable To Trustors During Joint Lives?

Are you currently in a situation where you require documentation for either business or personal purposes nearly every day.

There are numerous legal document templates accessible online, but locating trustworthy ones is not easy.

US Legal Forms offers thousands of form templates, including the Massachusetts Joint Trust with Income Payable to Trustors During Joint Lives, which can be printed to satisfy federal and state regulations.

Choose the pricing plan you prefer, fill in the required information to create your account, and pay for the order with your PayPal or credit card.

Select a convenient file format and download your copy.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- After that, you can download the Massachusetts Joint Trust with Income Payable to Trustors During Joint Lives template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Select the form you need and ensure it is for the correct city/state.

- Use the Preview option to review the document.

- Check the information to make sure you have chosen the correct form.

- If the form isn’t what you need, utilize the Search field to find the form that suits your needs and specifications.

- Once you find the right form, click Get now.

Form popularity

FAQ

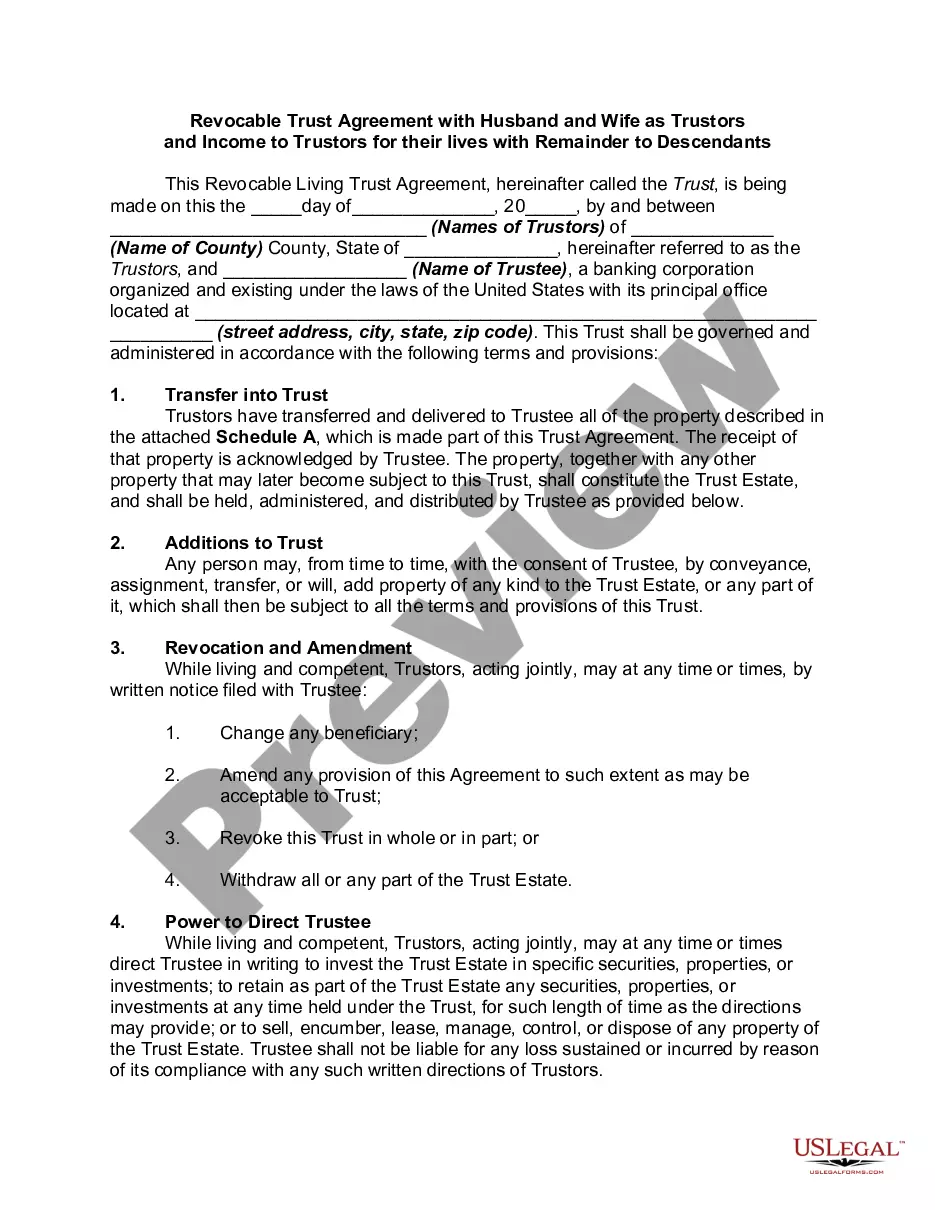

Joint trusts are also revocable living trusts, set up to hold all of the assets of a married couple and to provide access to the trust assets for both. Typically, at the first death, half of the assets receive a step-up in basis, but all of the assets stay in the trust.

What happens in this type of trust is that the trust is a joint revocable trust when both spouses are alive. When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse.

Under typical circumstances, the surviving spouse would become the sole trustee after the death of one spouse. The surviving spouse would control the shared property, and the personal property of the deceased spouse would be distributed to the beneficiaries.

The trust remains revocable while both spouses are alive. The couple may withdraw assets or cancel the trust completely before one spouse dies. When the first spouse dies, the trust becomes irrevocable and splits into two parts: the A trust and the B trust.

The joint revocable living trust should be revocable and subject to amendment by either spouse or both spouses acting together during the joint lifetimes of the spouses. If the trust is revoked, its assets will be distributed to the spouses as they direct.

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor's final income tax return. As mentioned earlier, the once-revocable grantor trust will now be considered a separate taxpayer, with its own income tax reporting responsibility.

In general, most experts agree that Separate Trusts can provide more asset protection. Joint Trust: Marital assets are all together in a single trust. This means there's less asset protection, because if there's ever a judgment over one of the spouses, all of the assets could end up being at risk.

Though not a silver bullet for every situation, in appropriate circumstances, a Joint Revocable Living Trust ("Joint Trust") can provide a married couple with significant benefits and simplify the administration of assets upon death or incapacity.

After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property.

A revocable living trust becomes irrevocable once the sole grantor or dies or becomes mentally incapacitated. If you have a joint trust for you and your spouse, then a portion of the joint trust can become irrevocable when the first spouse dies and will become irrevocable when the last spouse dies.