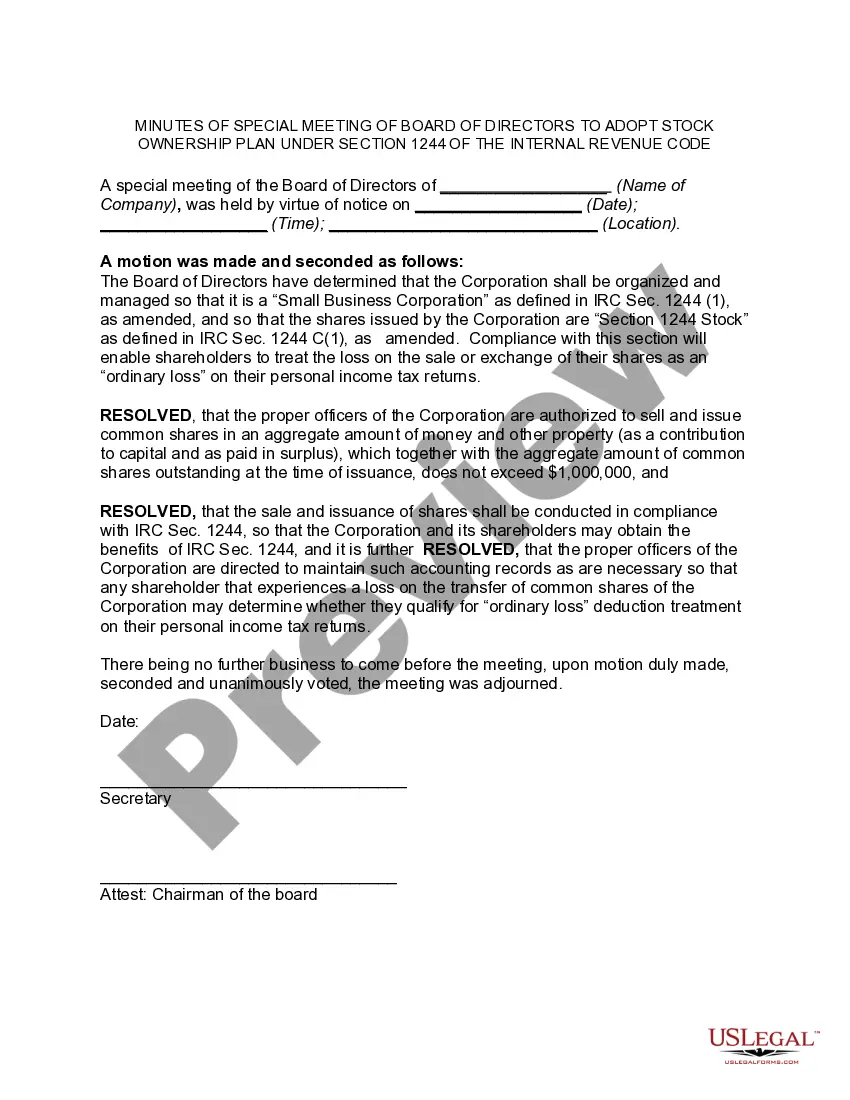

Massachusetts Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code

Description

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

How to fill out Minutes Of Special Meeting Of The Board Of Directors Of (Name Of Corporation) To Adopt Stock Ownership Plan Under Section 1244 Of The Internal Revenue Code?

If you need extensive, obtain, or print out authentic document templates, utilize US Legal Forms, the largest selection of legal forms available online.

Employ the site's simple and user-friendly search to locate the documents you require. Various templates for business and personal applications are organized by categories and states, or keywords.

Utilize US Legal Forms to obtain the Massachusetts Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code within just a few clicks.

Every legal document template you acquire is yours permanently. You have access to all forms you downloaded within your account. Visit the My documents section and select a form to print or download again.

Complete and download, and print the Massachusetts Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- If you are currently a US Legal Forms member, Log In to your account and click the Obtain button to locate the Massachusetts Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code.

- You can also access forms you previously submitted electronically from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Make sure you have selected the form for the correct city/state.

- Step 2. Use the Review feature to examine the form's details. Remember to read the description.

- Step 3. If you are not satisfied with the form, utilize the Search field at the top of the page to find other versions of the legal form template.

- Step 4. Once you have found the form you need, click the Obtain now button. Choose the pricing plan you prefer and input your details to register for the account.

- Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the deal.

- Step 6. Select the format of the legal form and download it to your device.

- Step 7. Fill out, edit, and print or sign the Massachusetts Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code.

Form popularity

FAQ

In order to qualify as §1244 stock, the stock must be issued, and the consideration paid by the shareholder must consist of money or other property, not services. Stock and other securities are not "other property" for this purpose.

1244(b)). Any loss in excess of the limit is a capital loss, subject to the capital loss rules. Thus, if the potential loss exceeds the $50,000 (or $100,000) limit, the stock should be disposed of in more than one year to maximize the ordinary loss treatment.

An ordinary loss from the sale or worthlessness of Section 1244 stock is reported on Form 4797, and if the total loss exceeds the maximum amount that can be treated as an ordinary loss for the year, the transaction should also be reported on Form 8949.

1244 stock is available only to individuals and partners in partnerships. The ruling held that if IRC Sec. 1244 stock is issued to S corporations, such corporations and their shareholders may not treat losses on such stock as ordinary losses. This is so notwithstanding IRC Sec.

Qualifying for Section 1244 StockThe stock must be issued by U.S. corporations and can be either a common or preferred stock.The corporation's aggregate capital must not have exceeded $1 million when the stock was issued and the corporation cannot derive more than 50% of its income from passive investments.More items...

Section 1244 stock is a stock transaction pursuant to the Internal Revenue Code provision that allows shareholders of an eligible small business corporation to treat up to $50,000 of losses (or, in the case of a husband and wife filing a joint return, $100,000) from the sale of stock as ordinary losses instead of

Qualifying for Section 1244 StockThe stock must be issued by U.S. corporations and can be either a common or preferred stock.The corporation's aggregate capital must not have exceeded $1 million when the stock was issued and the corporation cannot derive more than 50% of its income from passive investments.More items...

Section 1244 stock is a stock transaction pursuant to the Internal Revenue Code provision that allows shareholders of an eligible small business corporation to treat up to $50,000 of losses (or, in the case of a husband and wife filing a joint return, $100,000) from the sale of stock as ordinary losses instead of

Corporations, trusts, estates and trustees in bankruptcy are not eligible to claim a Section 1244 loss. A Section 1244 loss can be claimed only by an individual or partnership to whom the stock was issued and who has continuously held the stock until it is sold or is determined to be worthless.