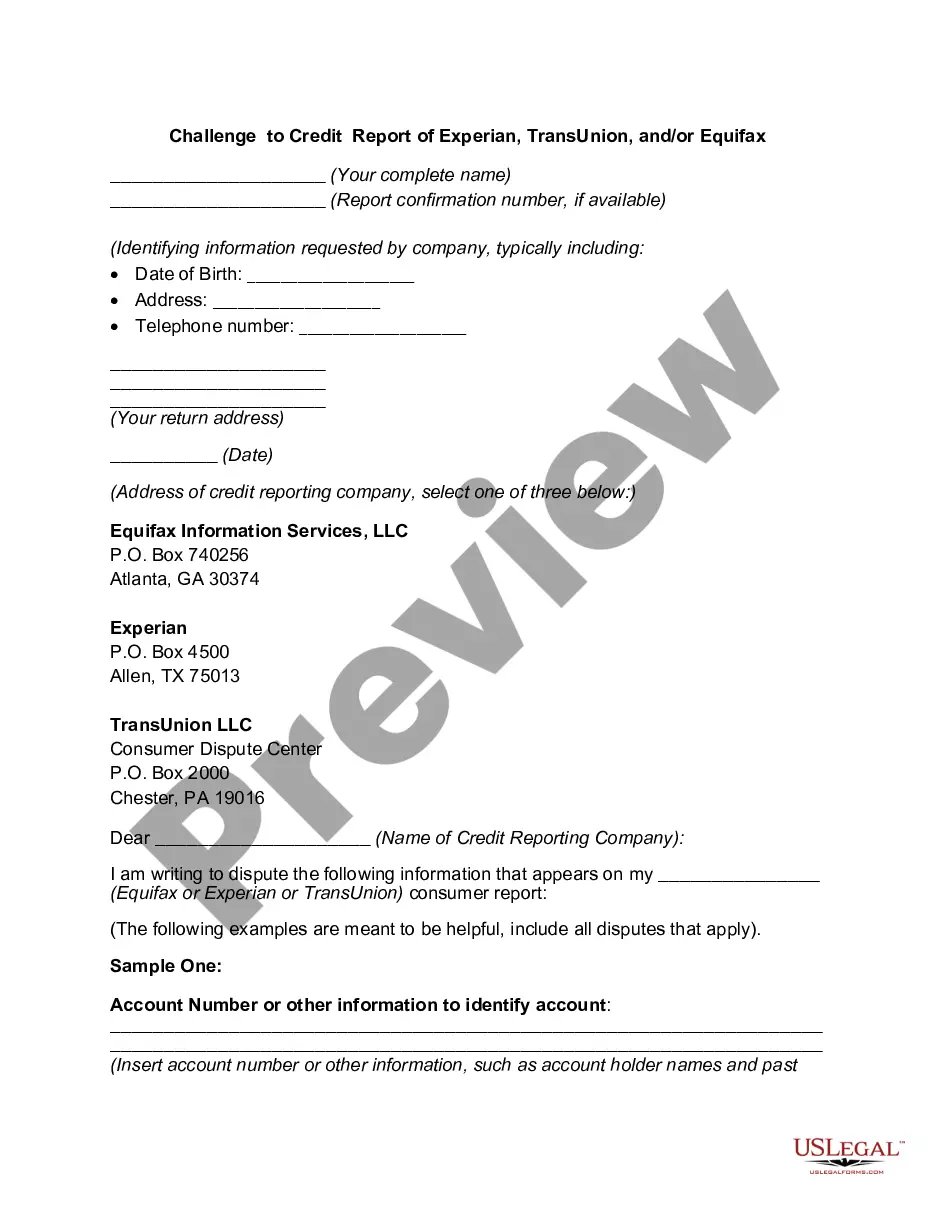

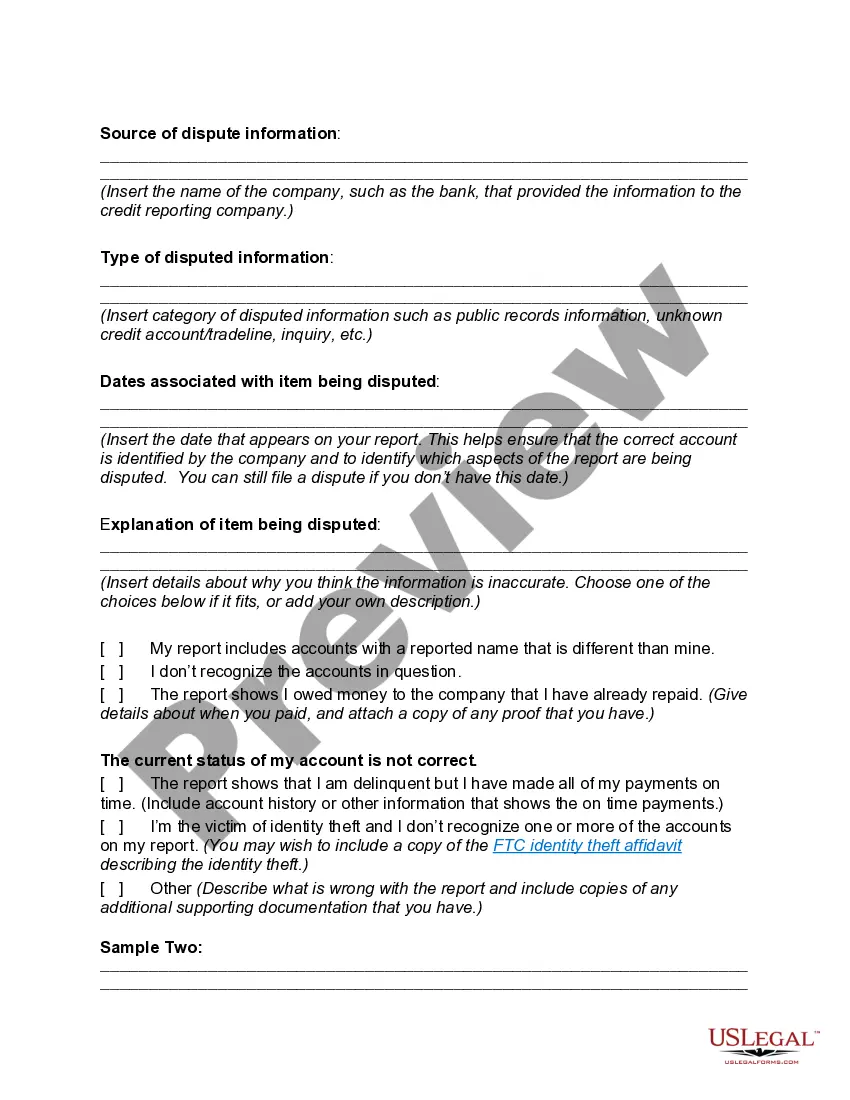

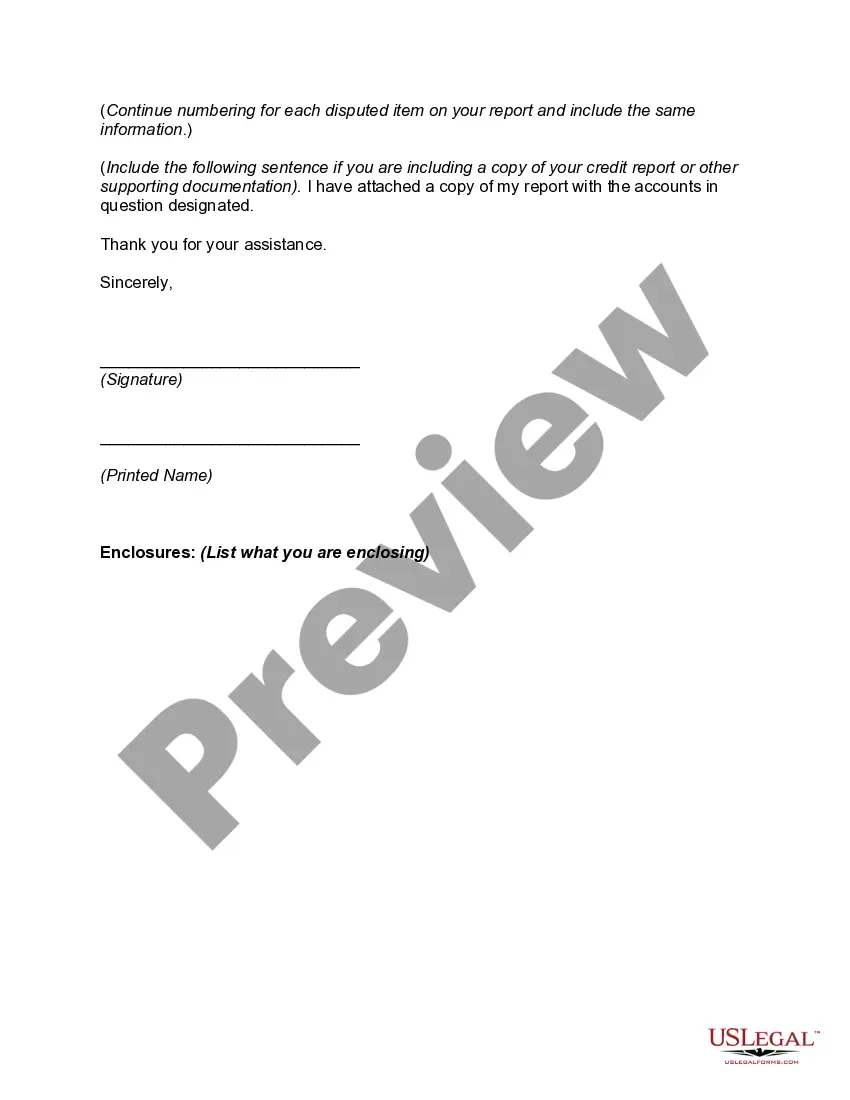

Massachusetts Challenge crediting Report of Experian, TransUnion, and/or Equifax: Understanding Your Rights In Massachusetts, consumers have the right to challenge inaccuracies or errors on their credit reports maintained by major credit reporting agencies such as Experian, TransUnion, and Equifax. This process, known as a Massachusetts Challenge crediting Report, enables individuals to rectify any misinformation that may be negatively impacting their creditworthiness. By addressing inaccurate information, consumers can protect their financial reputation and ensure fair access to credit opportunities. Key Points: 1. Massachusetts Consumer Protection Laws: The Massachusetts Fair Credit Reporting Act and the Federal Fair Credit Reporting Act grant consumers the right to dispute inaccurate information on their credit reports. These acts hold credit reporting agencies responsible for maintaining accurate records and providing consumers with a fair and transparent process to rectify errors. 2. Types of Inaccuracies: Errors on credit reports can range from incorrect personal identifying information (e.g., wrong address, misspelled name) to erroneous account details (e.g., accounts not belonging to the consumer, duplicate entries). Challenging these inaccuracies is crucial as they can significantly impact credit scores and affect loan approvals, interest rates, insurance premiums, and even employment opportunities. 3. Initiating a Massachusetts Challenge crediting Report: To begin the challenge process, consumers should obtain a copy of their credit reports from Experian, TransUnion, and Equifax. Reviewing these reports thoroughly is essential to identify any incorrect information that requires rectification. 4. Filing a Dispute: Consumers can file a dispute with the credit reporting agency that listed the inaccuracies. This can typically be done online, over the phone, or via mail. When filing a dispute, it is important to provide clear and specific information explaining the inaccuracies, along with any supporting documentation such as payment receipts or correspondence with creditors. 5. Investigation by Credit Reporting Agencies: Once a dispute is filed, the credit reporting agency is obligated to conduct a reasonable investigation within a specific timeframe (generally 30 days). During this investigation, they will contact the data furnished, such as a lender or creditor, and request verification or correction of the disputed information. 6. Resolving the Dispute: Upon completion of the investigation, the credit reporting agency should provide a written response detailing the outcome. If the information is found to be inaccurate, it must be corrected or removed from the credit report. The agency should also provide an updated credit report reflecting the changes made. However, if the investigation finds the information to be accurate, consumers still have options to add a brief statement of explanation to their credit reports to contextualize the dispute. 7. Seeking Legal Assistance: If the credit reporting agency fails to address the inaccuracies or the dispute resolution process does not yield satisfactory results, consumers can consider seeking legal assistance. Massachusetts provides avenues for legal action against credit reporting agencies that fail to comply with their obligations under the law, including potential damages and attorney fees. By understanding their rights and using the Massachusetts Challenge crediting Report process effectively, consumers in Massachusetts can take proactive steps to ensure their credit reports accurately reflect their financial history, leading to improved creditworthiness and increased financial opportunities.

Massachusetts Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Massachusetts Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

You can invest hours on the web searching for the legal file design that fits the federal and state requirements you require. US Legal Forms supplies a huge number of legal forms which are examined by professionals. You can actually acquire or print out the Massachusetts Challenge to Credit Report of Experian, TransUnion, and/or Equifax from the service.

If you already possess a US Legal Forms profile, it is possible to log in and click on the Download option. Afterward, it is possible to total, change, print out, or sign the Massachusetts Challenge to Credit Report of Experian, TransUnion, and/or Equifax. Each legal file design you purchase is the one you have forever. To obtain yet another copy for any bought type, visit the My Forms tab and click on the related option.

If you use the US Legal Forms web site the first time, keep to the straightforward directions listed below:

- First, make sure that you have chosen the right file design for your area/city of your choosing. Read the type information to make sure you have picked out the proper type. If available, utilize the Preview option to search throughout the file design as well.

- In order to discover yet another edition of the type, utilize the Search field to find the design that meets your requirements and requirements.

- Once you have discovered the design you desire, click Purchase now to carry on.

- Choose the costs program you desire, type your references, and register for a merchant account on US Legal Forms.

- Complete the deal. You can use your Visa or Mastercard or PayPal profile to cover the legal type.

- Choose the format of the file and acquire it to your device.

- Make changes to your file if needed. You can total, change and sign and print out Massachusetts Challenge to Credit Report of Experian, TransUnion, and/or Equifax.

Download and print out a huge number of file layouts utilizing the US Legal Forms web site, which provides the biggest assortment of legal forms. Use professional and status-specific layouts to tackle your company or personal needs.