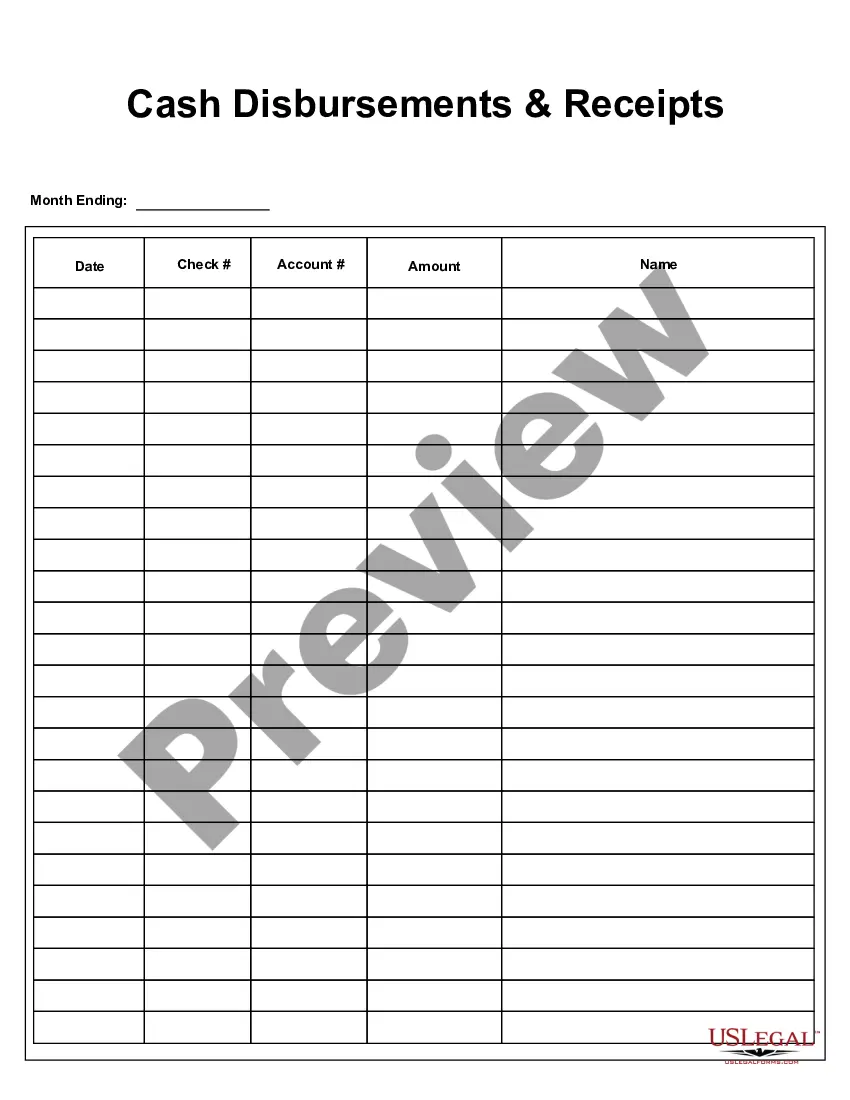

Massachusetts Cash Disbursements and Receipts refer to the financial transactions involving the outflow and inflow of funds in the Massachusetts state government. These transactions are crucial for tracking and managing the state's budgetary activities. In Massachusetts, there are several types of cash disbursements and receipts that play a vital role in the overall financial system. 1. Cash Disbursements: a. Payroll Disbursements: It involves the payment of salaries, wages, and employee benefits to the state government's employees. This includes salaries of teachers, law enforcement personnel, administrative staff, and more. b. Accounts Payable: Cash disbursements are made to settle outstanding bills and invoices owed by the state government to various vendors, suppliers, and contractors. c. Debt Repayment: Cash disbursements are allocated towards paying off debts, such as loans, bonds, or any other financial obligations of the Massachusetts government. d. Grants and Subsidies: Funds are disbursed to recipients, including local communities, nonprofit organizations, and educational institutions, as grants or subsidies for specific projects or programs. e. Capital Expenditures: Cash disbursements for infrastructure development projects, construction of new facilities, or the maintenance and repair of existing state-owned properties fall under this category. 2. Cash Receipts: a. Tax Revenues: Massachusetts cash receipts primarily come from various taxes, including income tax, sales tax, property tax, corporate tax, and excise tax. These revenues are collected by the Massachusetts Department of Revenue and contribute to the state's general fund. b. Federal Funds: Cash receipts may include grants, reimbursements, aids, and other financial support received from the federal government for specific purposes such as Medicaid, transportation projects, education, and social services. c. Fees and Licenses: Receipts from fees charged for licenses, permits, registrations, and other services provided by the state government, such as driver's licenses, professional licenses, and business permits. d. Lottery and Gambling Proceeds: Massachusetts cash receipts include revenue generated from the state-run lottery, casinos, and other gambling activities. e. Investment Income: Cash receipts may also arise from the interest and dividends earned on the state's investments or from returns on surplus funds invested. In summary, Massachusetts Cash Disbursements and Receipts encompass a wide range of financial transactions involving payroll, accounts payable, debt repayment, grants, capital expenditures, tax revenues, federal funds, fees and licenses, lottery proceeds, and investment income. These transactions are crucial for maintaining the state's financial stability, executing projects, and providing essential public services to the residents of Massachusetts.

Massachusetts Cash Disbursements and Receipts

Description

How to fill out Massachusetts Cash Disbursements And Receipts?

It is possible to spend several hours online trying to find the authorized papers template which fits the state and federal needs you need. US Legal Forms provides a large number of authorized forms which are examined by specialists. It is possible to download or print the Massachusetts Cash Disbursements and Receipts from our services.

If you already have a US Legal Forms bank account, you can log in and then click the Down load option. After that, you can full, edit, print, or indicator the Massachusetts Cash Disbursements and Receipts. Each and every authorized papers template you get is your own permanently. To have yet another duplicate of any purchased type, visit the My Forms tab and then click the related option.

If you use the US Legal Forms internet site the first time, adhere to the basic guidelines beneath:

- First, make certain you have chosen the best papers template for your county/city that you pick. Read the type description to make sure you have picked the correct type. If available, make use of the Preview option to search through the papers template as well.

- If you want to find yet another model from the type, make use of the Search industry to get the template that suits you and needs.

- When you have discovered the template you need, click Buy now to carry on.

- Choose the costs program you need, type in your accreditations, and sign up for your account on US Legal Forms.

- Total the deal. You should use your credit card or PayPal bank account to pay for the authorized type.

- Choose the file format from the papers and download it in your gadget.

- Make changes in your papers if required. It is possible to full, edit and indicator and print Massachusetts Cash Disbursements and Receipts.

Down load and print a large number of papers themes making use of the US Legal Forms website, that provides the biggest selection of authorized forms. Use expert and condition-particular themes to deal with your business or individual requirements.