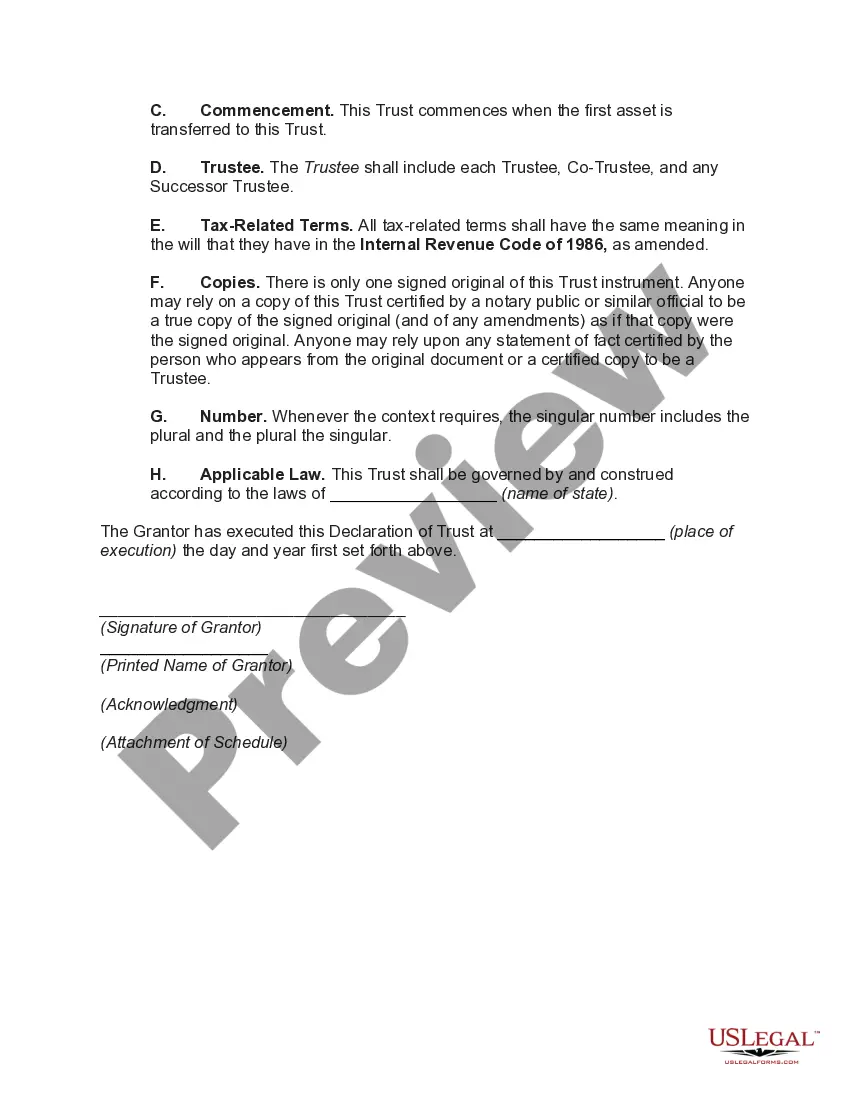

Massachusetts Granter Retained Annuity Trust (GREAT) is a specific type of irrevocable trust that allows individuals in Massachusetts to transfer assets while retaining an annuity payment stream for a specified period. It is a valuable estate planning tool that helps individuals minimize estate taxes and transfer wealth to beneficiaries. A Massachusetts GREAT is established when a granter (the individual creating the trust) transfers assets into the trust, while also designating themselves as the beneficiary. The granter then receives annual annuity payments from the trust for a predetermined period, typically between 2 and 20 years. At the end of the annuity period, any remaining trust assets pass on to the named beneficiaries. The primary purpose of a Massachusetts GREAT is to reduce the granter's taxable estate while transferring assets to beneficiaries. By retaining the annuity interest, the granter effectively freezes the asset's value for the purpose of calculating estate taxes. Any growth in the assets during the annuity period passes on to beneficiaries outside the granter's taxable estate, thus minimizing estate tax liability. Massachusetts offers various types of Granter Retained Annuity Trusts, including: 1. Standard GREAT: This is the most common type of GREAT. It involves the granter receiving a fixed annuity payment based on the initial value of the assets transferred into the trust. 2. Zeroed-Out GREAT: In this variation, the granter structures the annuity payment so that it equals the present value of the assets transferred into the trust. This results in a taxable gift of zero, making it an attractive option for those seeking to minimize gift taxes. 3. Rolling GREAT: With a rolling GREAT, the granter establishes a series of Grants that successively distribute the remaining assets from the previous GREAT. This strategy allows for continued wealth transfer while maintaining control over the assets. 4. Granter Retained Unit rust (GUT): A GUT functions similarly to a GREAT but provides for annuity payments based on a fixed percentage of the trust's assets, recalculated annually. This can be attractive when assets are expected to appreciate significantly over time. 5. Net Income with Makeup Charitable Remainder GREAT (TIMEOUT): This type of GREAT allows for the granter to receive annuity payments based on the trust's net income, with the remaining trust assets passing to a charitable organization upon termination. When establishing a Massachusetts Granter Retained Annuity Trust, it is crucial to consult with a qualified estate planning attorney or financial advisor experienced in trust planning in Massachusetts. They can help determine the appropriate type of GREAT based on individual circumstances and ensure compliance with state laws and regulations.

Massachusetts Grantor Retained Annuity Trust

Description

How to fill out Massachusetts Grantor Retained Annuity Trust?

If you want to total, acquire, or printing authorized file web templates, use US Legal Forms, the largest selection of authorized kinds, which can be found on the web. Make use of the site`s simple and easy hassle-free research to find the files you need. Different web templates for organization and individual reasons are sorted by classes and suggests, or key phrases. Use US Legal Forms to find the Massachusetts Grantor Retained Annuity Trust within a few clicks.

Should you be presently a US Legal Forms consumer, log in to your account and click on the Download option to find the Massachusetts Grantor Retained Annuity Trust. You can also entry kinds you previously downloaded within the My Forms tab of your respective account.

If you use US Legal Forms initially, follow the instructions below:

- Step 1. Be sure you have chosen the shape for that proper metropolis/country.

- Step 2. Use the Review solution to examine the form`s content. Do not overlook to see the explanation.

- Step 3. Should you be unsatisfied with all the form, take advantage of the Look for industry near the top of the monitor to discover other models from the authorized form template.

- Step 4. After you have discovered the shape you need, click on the Buy now option. Select the prices strategy you prefer and add your accreditations to sign up for an account.

- Step 5. Approach the purchase. You should use your Мisa or Ьastercard or PayPal account to perform the purchase.

- Step 6. Choose the file format from the authorized form and acquire it on the gadget.

- Step 7. Complete, modify and printing or signal the Massachusetts Grantor Retained Annuity Trust.

Every authorized file template you acquire is your own forever. You may have acces to every form you downloaded with your acccount. Go through the My Forms area and select a form to printing or acquire once again.

Be competitive and acquire, and printing the Massachusetts Grantor Retained Annuity Trust with US Legal Forms. There are millions of expert and status-distinct kinds you can utilize for your organization or individual needs.