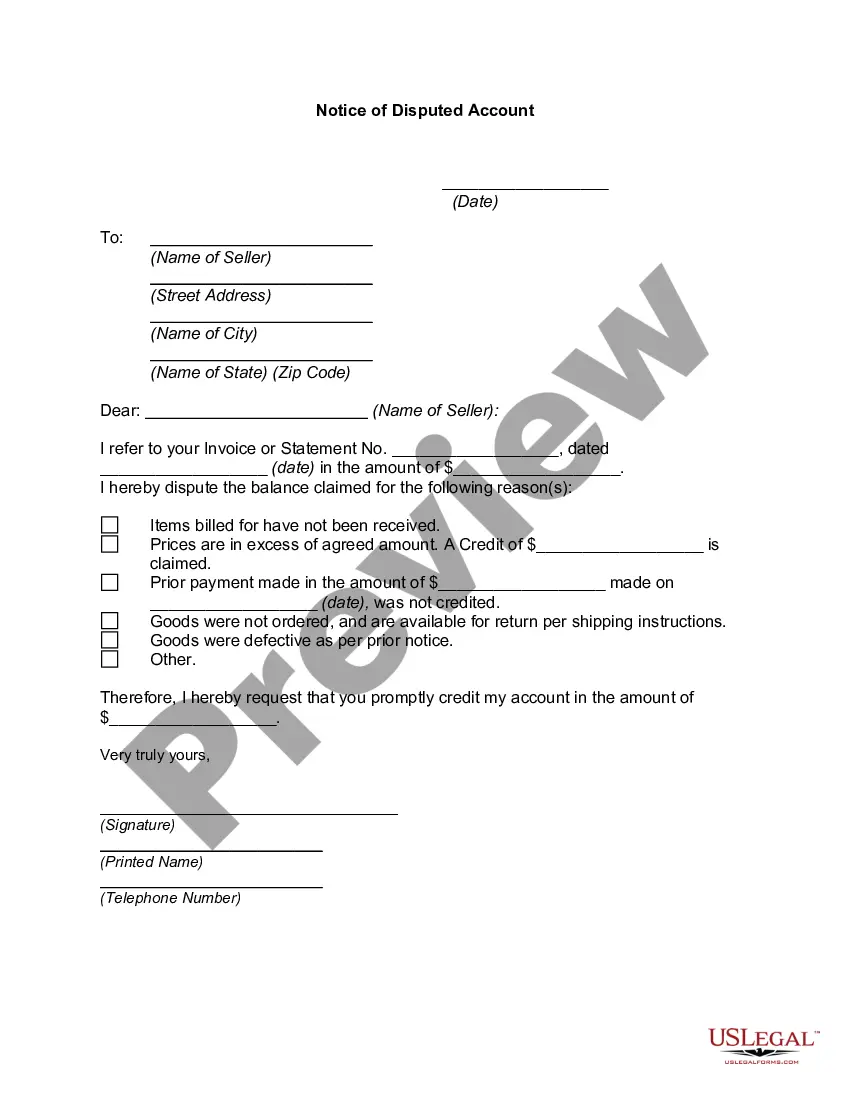

The Massachusetts Notice of Disputed Account is an essential legal document that allows consumers in Massachusetts to contest and dispute any incorrect or inaccurate information appearing on their credit reports. This notice is governed by the Fair Credit Reporting Act (FCRA) and serves as an important tool for individuals to protect their rights and maintain accurate credit information. When disputing an account, it is crucial to understand the different types of Massachusetts Notice of Disputed Account that can be filed, depending on the nature of the dispute: 1. Initial Notice of Disputed Account: This is the first step consumers should take when they discover inaccurate information on their credit reports. It involves notifying the credit reporting agencies, such as Equifax, Experian, and TransUnion, about the disputed account and providing copies of any supporting documentation. 2. Follow-up Notice of Disputed Account: If the initial notice does not lead to a satisfactory resolution and the incorrect information remains on the credit report, consumers may need to file a follow-up notice. This notice reiterates the dispute and the consumer's rights under the FCRA, emphasizing the urgency for the credit reporting agencies to investigate the account further. 3. Notice of Disputed Account to the Creditor: In some cases, it may be necessary to directly notify the creditor associated with the disputed account. This notice should outline the inaccuracies found in their reporting and request that they investigate and correct the information. The process of filing a Massachusetts Notice of Disputed Account typically involves providing comprehensive details about the disputed account, such as the account number, creditor's name, and the specific inaccuracies in question. It is essential to include supporting evidence, such as payment receipts, contracts, or correspondence, that demonstrates the discrepancy between the reported information and the consumer's records. Once the notices are sent, the credit reporting agencies and creditors are legally obligated to conduct a thorough investigation within 30 days. They must review the evidence provided and correct any erroneous information, update the consumer's credit report, and notify the consumer of the outcome. In conclusion, the Massachusetts Notice of Disputed Account plays a crucial role in protecting consumer rights and ensuring accurate credit reporting. By understanding the various types of notices and following the proper procedures, individuals can take control of their credit information and rectify any inaccuracies that may impact their financial well-being.

Massachusetts Notice of Disputed Account

Description

How to fill out Massachusetts Notice Of Disputed Account?

If you wish to obtain, retrieve, or print legal document templates, use US Legal Forms, the most significant repository of legal forms available online.

Leverage the website’s straightforward and user-friendly search to find the documents you require. Various templates for business and personal use are sorted by categories and states, or keywords.

Use US Legal Forms to find the Massachusetts Notice of Disputed Account in just a few clicks.

Every legal document template you purchase is yours indefinitely. You will have access to every form you downloaded in your account. Navigate to the My documents section and select a form to print or download again.

Complete and download, and print the Massachusetts Notice of Disputed Account with US Legal Forms. There are countless professional and state-specific forms you can use for your business or personal needs.

- If you are currently a US Legal Forms user, Log In to your account and click the Download button to access the Massachusetts Notice of Disputed Account.

- You can also retrieve forms you previously downloaded from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to review the form’s content. Remember to check the description.

- Step 3. If you are not satisfied with the document, utilize the Search field at the top of the screen to find other forms in the legal document library.

- Step 4. Once you have identified the form you need, click the Buy now button. Select the subscription plan you prefer and enter your information to create an account.

- Step 5. Complete the purchase. You can use your credit card or PayPal account to finalize the transaction.

- Step 6. Choose the format of the legal document and download it to your device.

- Step 7. Fill out, edit, and print or sign the Massachusetts Notice of Disputed Account.

Form popularity

FAQ

In Massachusetts, the statute of limitations for collecting most debts is generally six years. After this period, creditors may not be able to enforce collection actions legally. If you are navigating disputes involving debt, such as a Massachusetts Notice of Disputed Account, understanding these timeframes can be crucial for resolving your obligations effectively.

A Massachusetts debt validation notice is a letter sent by a creditor to confirm the existence and validity of a debt. This notice typically outlines the amount owed and provides details about the creditor. If you receive such a notice, especially in conjunction with a Massachusetts Notice of Disputed Account, take it seriously and consider reaching out to clarify any uncertainties.

A letter from the Massachusetts Department of Revenue may arise from various tax-related issues including, but not limited to, assessments, payment plans, or audits. It is imperative to review the letter carefully as it may contain critical information regarding your tax obligations, potentially linked to a Massachusetts Notice of Disputed Account. Addressing the concerns outlined promptly will help avoid complications.

The Massachusetts Department of Revenue is the state agency responsible for managing tax collection and enforcement in Massachusetts. This agency administers state taxes, issues regulations, and provides guidance to taxpayers. Understanding its role and functions can help you navigate any correspondence, including matters tied to a Massachusetts Notice of Disputed Account.

Typically, you can go back up to three years to file for back taxes in Massachusetts. However, if you fail to file, the Department of Revenue may pursue collections for an extended period. Being proactive when dealing with tax matters and consulting resources from platforms like USLegalForms can streamline the process, especially concerning a Massachusetts Notice of Disputed Account.

The Massachusetts Department of Revenue might send you a letter for various reasons, including tax assessments, corrections, or notices regarding unpaid taxes. A letter may also arise from an audit process or an update about your tax situation. If you receive a Massachusetts Notice of Disputed Account, responding quickly helps clarify your position and resolve any misunderstandings.

The statute of limitations for tax collection in Massachusetts usually lasts for six years from the time the tax return was filed. This period can sometimes extend based on various factors like unfiled returns or fraudulent filings. Being aware of this timeline is essential if you receive notices, such as a Massachusetts Notice of Disputed Account, which may alter your obligations.

A letter ruling from the Massachusetts Department of Revenue serves as a written statement providing guidance on specific tax questions. This ruling is usually requested when uncertainties about tax laws arise, potentially affecting your tax obligations. It's vital to refer to the guidance, especially if engaged in disputes that could lead to further complications, such as a Massachusetts Notice of Disputed Account.

In Massachusetts, you can typically claim a tax refund for up to three years from the original return filing date. If you missed this time frame, options may still exist to appeal or address disputes, especially if you received a Massachusetts Notice of Disputed Account. Timely action on tax matters helps minimize complications and potential issues.

Receiving a letter from the Department of Revenue typically indicates a matter related to your taxes or an account dispute. This correspondence might be related to an unpaid tax balance, a refund issue, or a formal notice such as a Massachusetts Notice of Disputed Account. Engaging with this letter promptly will ensure you address any possible issues or disputes regarding your financial obligations.