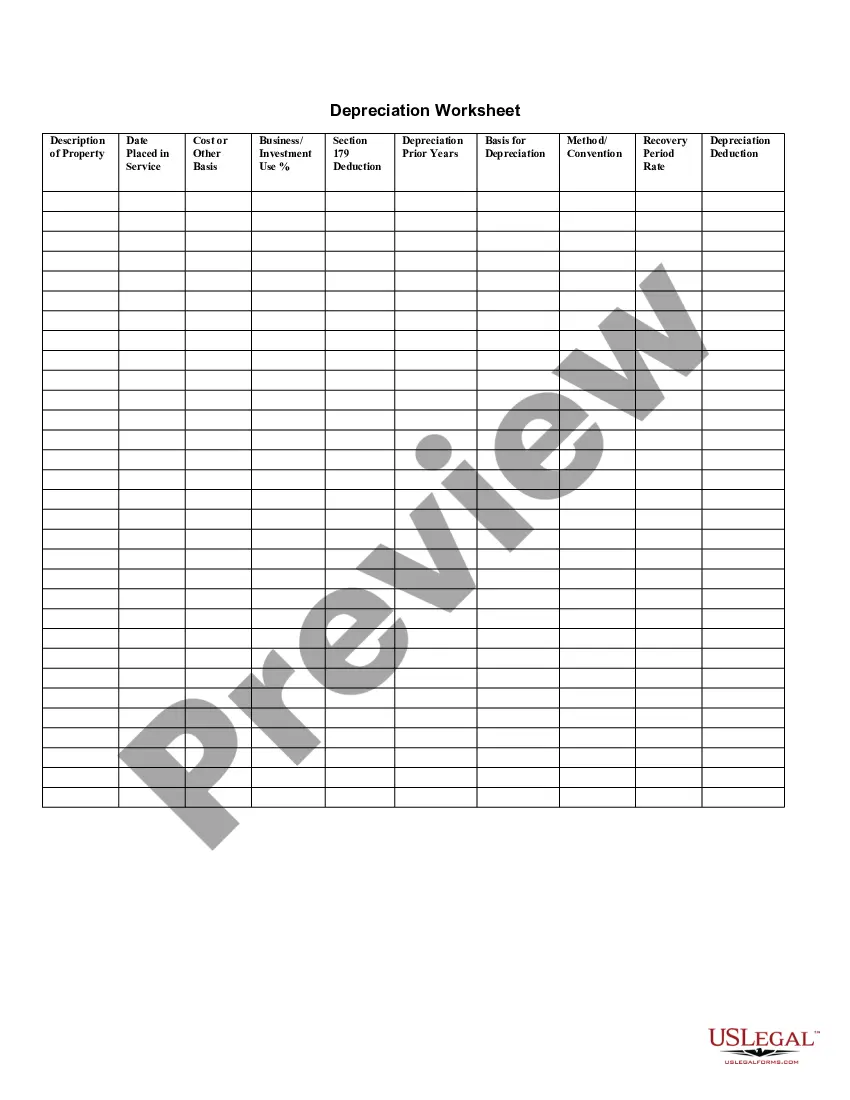

Massachusetts Depreciation Schedule

Description

How to fill out Depreciation Schedule?

Are you currently situated in a location where you require documentation for both business or personal aims nearly every day.

There are numerous legitimate template forms accessible online, yet finding reliable ones is challenging.

US Legal Forms provides thousands of form templates, including the Massachusetts Depreciation Schedule, that are crafted to comply with federal and state requirements.

Once you acquire the correct form, click Get now.

Choose the payment plan you prefer, fill in the required details to create your account, and complete the transaction using your PayPal or credit card.

- If you are already acquainted with the US Legal Forms website and possess an account, just Log In.

- Then, you can download the Massachusetts Depreciation Schedule template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Obtain the form you need and ensure that it is for the correct locality/county.

- Utilize the Review option to examine the form.

- Examine the description to confirm you have selected the right document.

- If the form is not what you are searching for, utilize the Search area to find the form that fits your needs and requirements.

Form popularity

FAQ

27, 2017, and placed in service during calendar year 2020, the depreciation limit under Sec. 280F(d)(7) is $18,100 for the first tax year; $16,100 for the second tax year; $9,700 for the third tax year; and $5,760 for each succeeding year, all unchanged from 2019. Under Sec.

Massachusetts adopts the change made by the CARES Act with respect to the depreciable life of QIP but has decoupled from the federal bonus depreciation rules. Consequently, the Massachusetts depreciation deduction for QIP must be calculated without regard to bonus depreciation.

Massachusetts generally follows current Code for § 62(a)(1), trade or business expense deductions, but Massachusetts specifically disallows the bonus depreciation deduction at IRC A§ 168(k).

As a general rule, Massachusetts does not adopt any federal personal income tax law changes incorporated into the IRC after January 1, 2005. However, certain specific Massachusetts personal income tax provisions, as set forth in MGL ch 62, § 1(c), automatically conform to the current IRC.

It was scheduled to go down to 40% in 2018 and 30% in 2019, and then not be available in 2020 and beyond. The Tax Cuts and Jobs Act, enacted at the end of 2018, increases first-year bonus depreciation to 100%. It goes into effect for any long-term assets placed in service after September 27, 2017.

The total section 179 deduction and depreciation you can deduct for a passenger automobile, including a truck or van, you use in your business and first placed in service in 2021 is $18,200, if the special depreciation allowance applies, or $10,200, if the special depreciation allowance does not apply.

Massachusetts allows corporations to expense certain depreciable business assets instead of treating them as capital expenditures. Taxpayers are allowed an I.R.C. §179 deduction in the same amount as allowed federally.

Id. Massachusetts generally follows current Code for § 62(a)(1), trade or business expense deductions, but Massachusetts specifically disallows the bonus depreciation deduction at IRC A§ 168(k).

For new or used passenger automobiles eligible for bonus depreciation in 2021, the first-year limitation is increased by an additional $8,000, to $18,200.

The portion of the business standard mileage rate that is treated as depreciation will be 27 cents per mile for 2020, 1 cent more than 2019, one of the few amounts that is increasing.