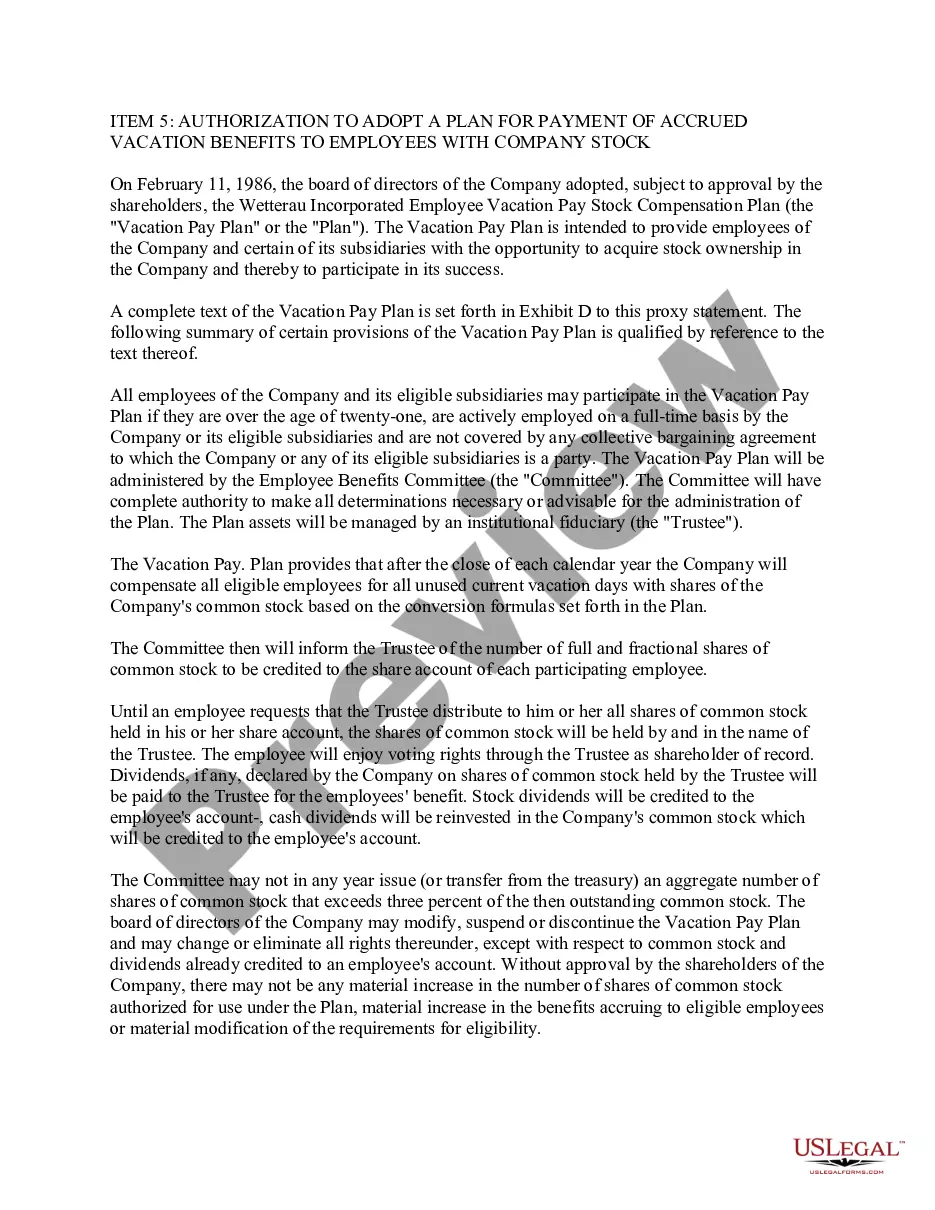

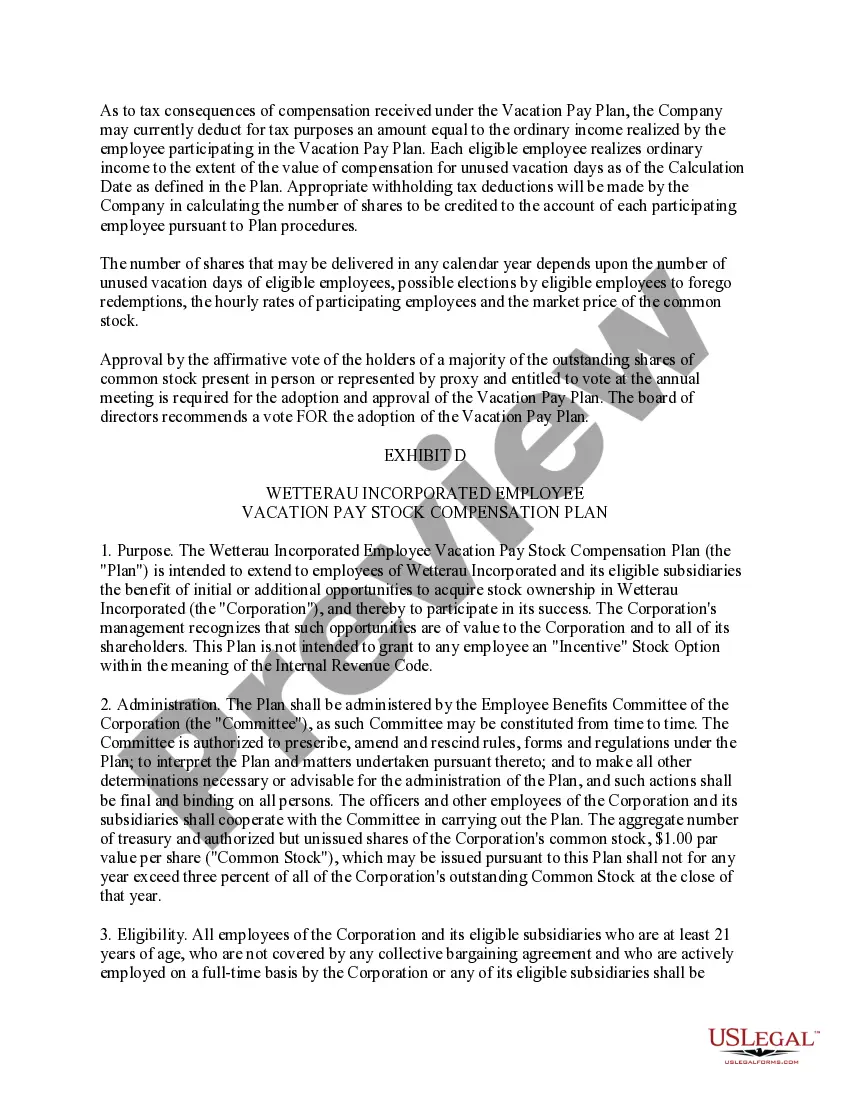

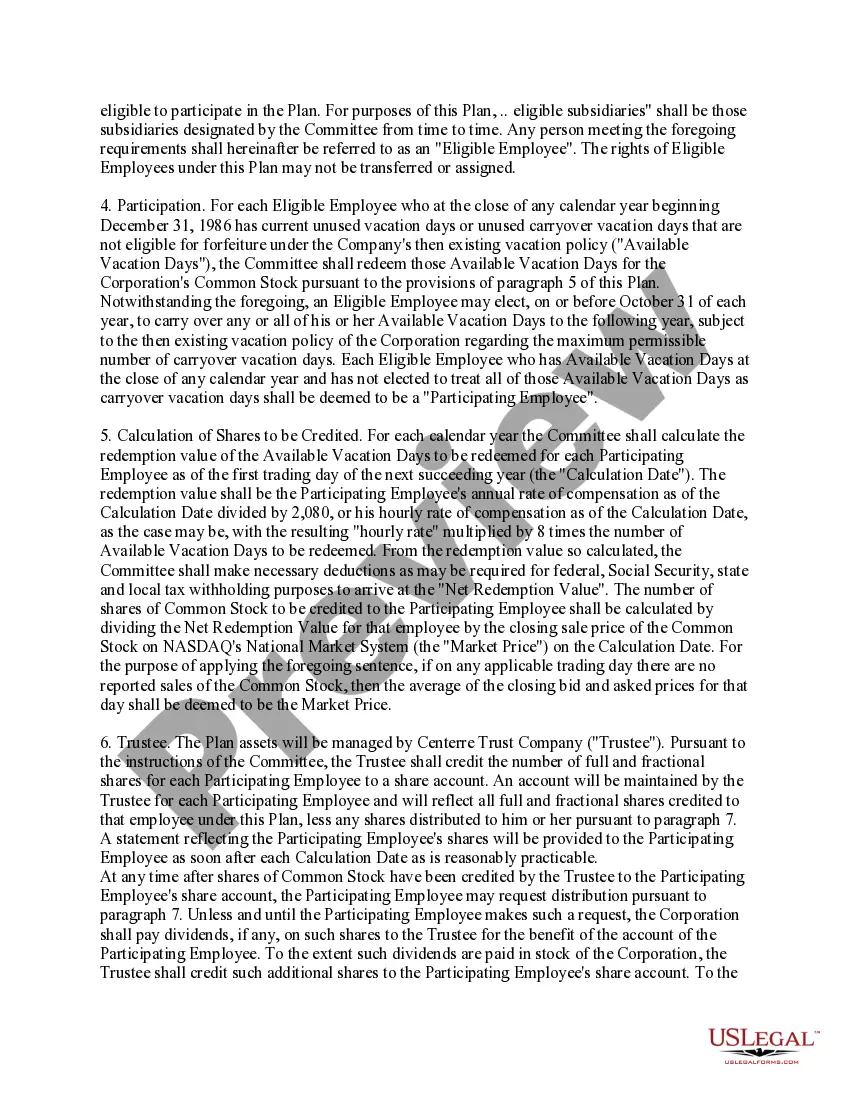

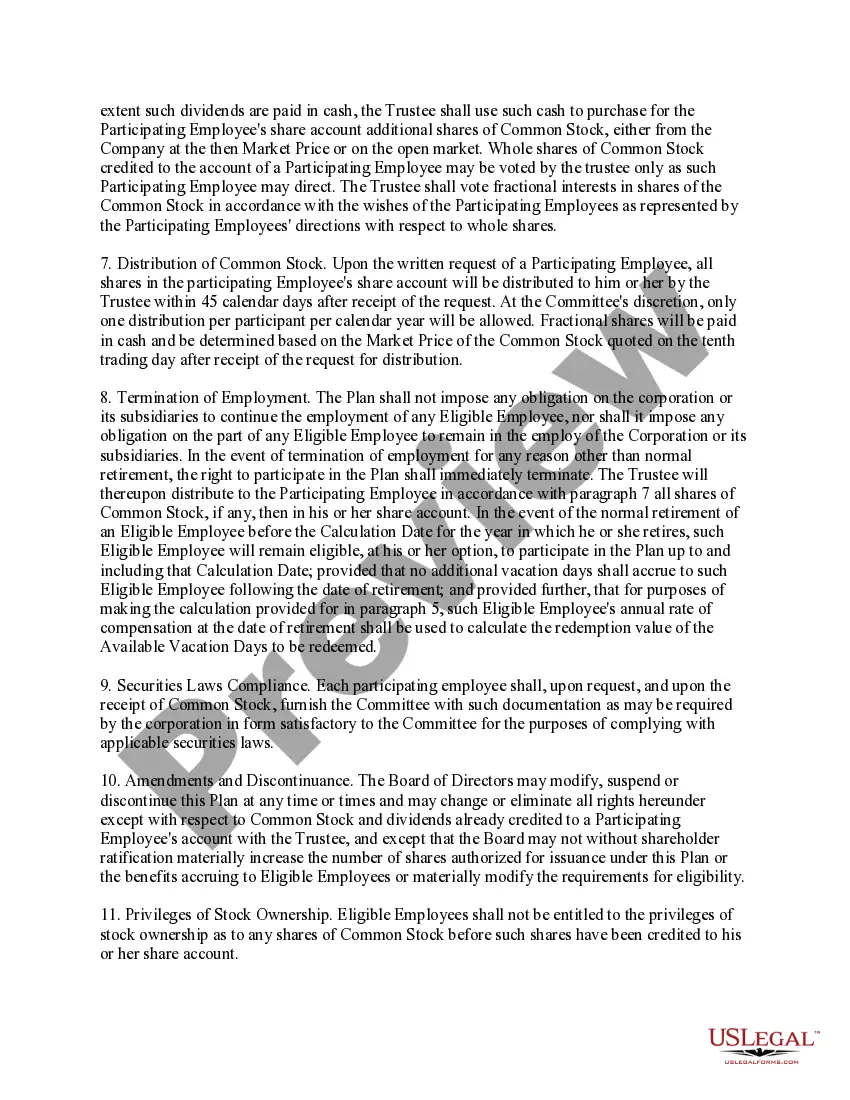

Title: Massachusetts Authorization to Adopt a Plan for Payment of Accrued Vacation Benefits to Employees with Company Stock: A Comprehensive Description Introduction: In Massachusetts, employers have the option to adopt a specific plan for the payment of accrued vacation benefits to employees who possess company stock. This authorization allows employers to provide a unique benefit structure to their employees, ensuring the efficient utilization of accrued vacation benefits while leveraging the value of company stocks. This article aims to provide a detailed description of this Massachusetts authorization, emphasizing its significance, benefits, legal requirements, and potential variants. 1. Understanding Massachusetts Authorization: Massachusetts employers can adopt a plan that enables employees holding company stock to receive their accrued vacation benefits in a manner tailored to their stock holdings. This authorization recognizes the importance of providing employees with alternative means to maximize the value and utility of their accrued vacation benefits. 2. Advantages of Massachusetts Authorization: By adopting a plan for payment of accrued vacation benefits to employees with company stock, employers can enhance employee satisfaction, increase employee retention, and create incentives for employees to acquire company stock. Additionally, such plans align employees' vested interests with the long-term success and growth of the company, fostering a sense of ownership and commitment. 3. Key Legal Requirements: a. Plan Documentation: Employers must formulate and maintain a comprehensive plan document that details the structure, terms, and conditions of the payment arrangement. This document should include eligibility criteria, vesting schedules, valuation methodology, and the process for executing the transactions. b. Compliance with State and Federal Laws: Employers must ensure that their plans comply with all relevant state and federal laws, such as the Massachusetts Wage Act, federal securities laws, ERICA (Employee Retirement Income Security Act), and any applicable regulations and reporting requirements. c. Equal Treatment: Employers should ensure that employees with company stock are not disadvantaged compared to employees without company stock. Implementation of any payment plan should not result in discrimination or preferential treatment among employees. 4. Possible Variants of Massachusetts Authorization: Though the general concept remains the same, different types of plans can be formulated to suit employers' specific needs. Some possible variations include: a. Percentage Conversion: Employees may have the option to convert a certain percentage of their accrued vacation benefits into company stock. b. Cash-Equivalent Option: Employees can choose to receive a cash equivalent of the value of their accrued vacation benefits, calculated based on the current market value of the company stock. c. Stock Purchase Option: Companies can offer employees the opportunity to purchase additional stock using their accrued vacation benefits at discounted prices. Conclusion: The Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock offers employers an opportunity to enhance employee engagement and align the workforce's interests with the company's growth. By understanding the legal requirements and exploring various plan variants, employers can tailor their approach to fit their unique organizational structure, while providing employees with an attractive incentive to invest in the company's success.

Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock with copy of plan

Description

How to fill out Massachusetts Authorization To Adopt A Plan For Payment Of Accrued Vacation Benefits To Employees With Company Stock With Copy Of Plan?

If you want to full, download, or print out authorized papers web templates, use US Legal Forms, the biggest selection of authorized types, which can be found online. Make use of the site`s easy and convenient search to obtain the paperwork you need. Various web templates for enterprise and personal functions are categorized by types and claims, or key phrases. Use US Legal Forms to obtain the Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock with copy of plan in just a number of clicks.

When you are currently a US Legal Forms buyer, log in for your account and click the Acquire option to obtain the Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock with copy of plan. Also you can gain access to types you in the past acquired within the My Forms tab of your account.

If you use US Legal Forms initially, refer to the instructions below:

- Step 1. Make sure you have chosen the form for that proper metropolis/land.

- Step 2. Make use of the Preview option to check out the form`s articles. Never forget to read through the description.

- Step 3. When you are unsatisfied together with the kind, take advantage of the Search area near the top of the monitor to discover other types in the authorized kind format.

- Step 4. When you have discovered the form you need, select the Acquire now option. Pick the prices strategy you prefer and put your accreditations to register for the account.

- Step 5. Approach the purchase. You can utilize your credit card or PayPal account to finish the purchase.

- Step 6. Pick the structure in the authorized kind and download it in your gadget.

- Step 7. Total, change and print out or sign the Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock with copy of plan.

Every authorized papers format you get is the one you have forever. You have acces to each and every kind you acquired in your acccount. Select the My Forms segment and pick a kind to print out or download once more.

Remain competitive and download, and print out the Massachusetts Authorization to adopt a plan for payment of accrued vacation benefits to employees with company stock with copy of plan with US Legal Forms. There are many professional and status-particular types you can use for your enterprise or personal requirements.