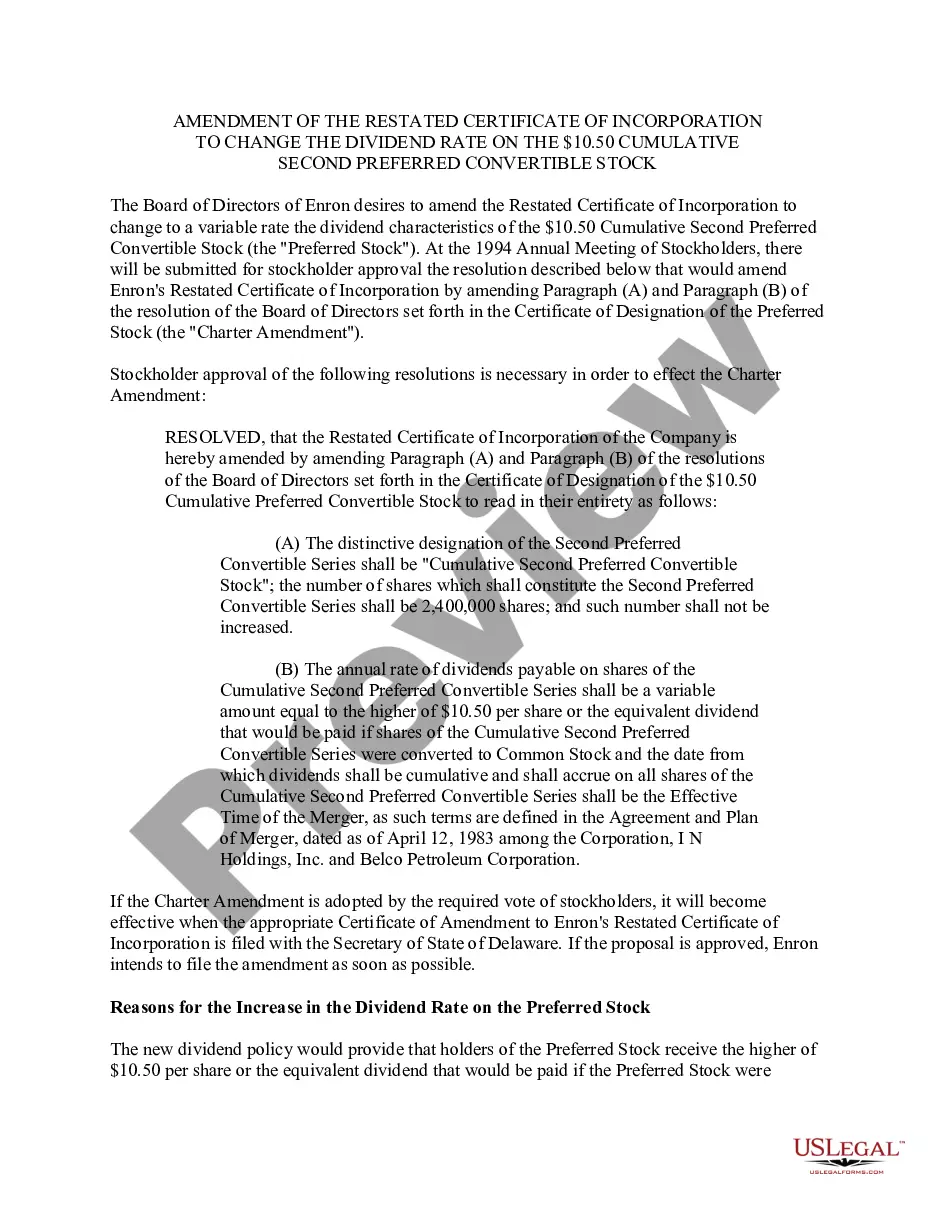

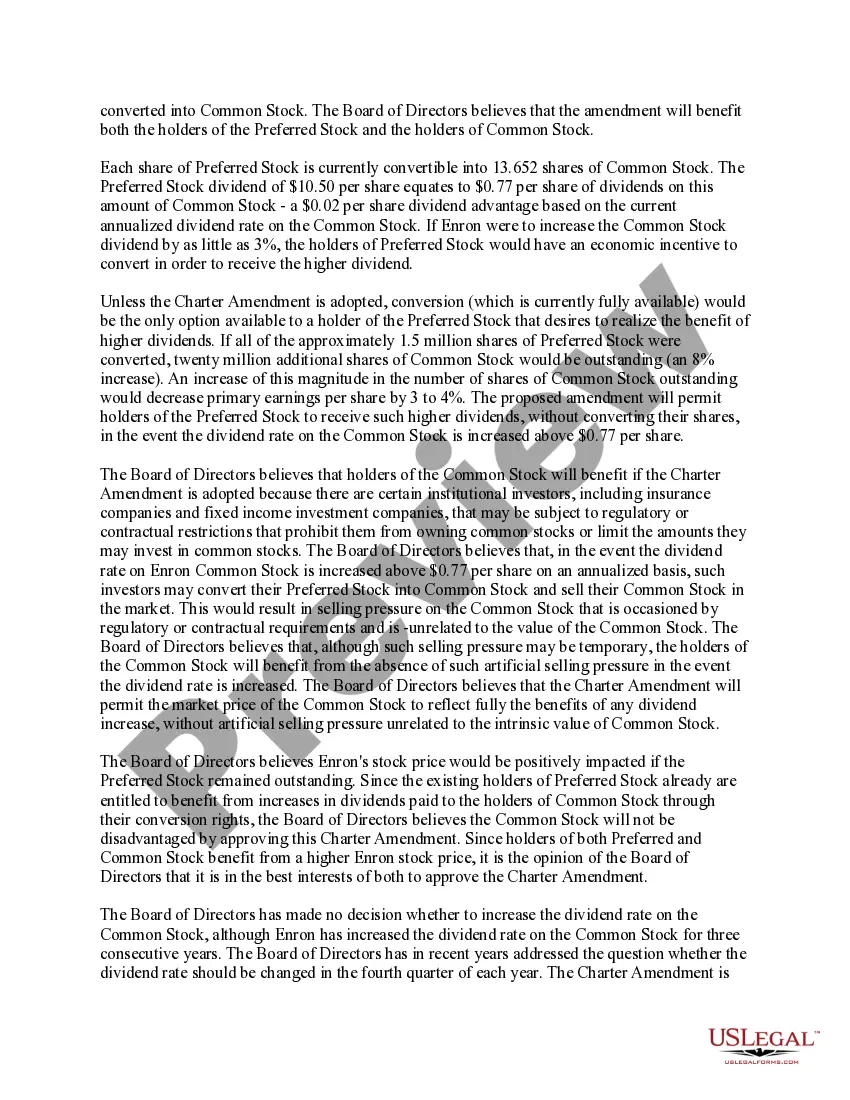

Massachusetts Amendment of Restated Certificate of Incorporation is a legal document that allows a company to make changes to its existing certificate of incorporation. In this specific case, the amendment is related to the dividend rate on $10.50 cumulative second preferred convertible stock. This means that the company is seeking to modify the amount of dividends paid out to holders of this specific type of stock. The purpose of this amendment is to adjust the dividend rate on the $10.50 cumulative second preferred convertible stock, potentially increasing or decreasing it based on the company's financial performance or other relevant factors. This change could affect the dividend payments received by shareholders who hold this specific type of stock. The Massachusetts Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock is an important decision that requires proper documentation and shareholder approval. By issuing this amendment, the company aims to align the dividend rate with its current financial situation and potential growth prospects. It is important to note that this specific type of amendment applies to the $10.50 cumulative second preferred convertible stock. There might be other amendments related to different classes or types of stock issued by the company, but this particular amendment solely focuses on modifying the dividend rate on this specific stock. In conclusion, the Massachusetts Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock is a significant legal process that allows a company to adjust the dividends paid to holders of this specific type of stock. The purpose of such an amendment is to ensure that the dividend rate is in line with the company's current financial situation and growth prospects.

Massachusetts Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Massachusetts Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

If you need to full, obtain, or printing lawful document web templates, use US Legal Forms, the greatest selection of lawful forms, that can be found on-line. Use the site`s simple and practical research to find the paperwork you will need. Various web templates for organization and specific uses are sorted by groups and suggests, or keywords. Use US Legal Forms to find the Massachusetts Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock in just a handful of click throughs.

When you are currently a US Legal Forms customer, log in for your bank account and click the Download button to obtain the Massachusetts Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. You can even gain access to forms you previously acquired within the My Forms tab of your respective bank account.

If you work with US Legal Forms the first time, follow the instructions beneath:

- Step 1. Ensure you have chosen the shape for the right town/region.

- Step 2. Make use of the Preview solution to check out the form`s articles. Do not overlook to read through the outline.

- Step 3. When you are not satisfied together with the type, make use of the Search discipline towards the top of the display to locate other models in the lawful type template.

- Step 4. After you have discovered the shape you will need, go through the Purchase now button. Opt for the prices strategy you prefer and put your references to register to have an bank account.

- Step 5. Process the deal. You may use your charge card or PayPal bank account to finish the deal.

- Step 6. Find the structure in the lawful type and obtain it on your product.

- Step 7. Total, modify and printing or signal the Massachusetts Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

Each lawful document template you buy is your own property eternally. You possess acces to every type you acquired within your acccount. Click the My Forms segment and pick a type to printing or obtain once again.

Contend and obtain, and printing the Massachusetts Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock with US Legal Forms. There are many skilled and condition-specific forms you can use for your personal organization or specific needs.