Massachusetts Letter to Stockholders regarding authorization and sale of preferred stock and stock transfer restriction to protect tax benefits

Description

How to fill out Letter To Stockholders Regarding Authorization And Sale Of Preferred Stock And Stock Transfer Restriction To Protect Tax Benefits?

Finding the right authorized papers web template can be quite a struggle. Obviously, there are tons of themes available on the net, but how would you discover the authorized kind you will need? Use the US Legal Forms web site. The assistance gives 1000s of themes, like the Massachusetts Letter to Stockholders regarding authorization and sale of preferred stock and stock transfer restriction to protect tax benefits, that you can use for company and private requires. Each of the types are examined by pros and meet up with state and federal requirements.

Should you be currently signed up, log in for your bank account and click the Acquire switch to obtain the Massachusetts Letter to Stockholders regarding authorization and sale of preferred stock and stock transfer restriction to protect tax benefits. Make use of your bank account to search from the authorized types you may have ordered previously. Check out the My Forms tab of your bank account and obtain yet another duplicate in the papers you will need.

Should you be a brand new user of US Legal Forms, listed here are easy instructions that you can stick to:

- Very first, be sure you have chosen the appropriate kind to your city/county. It is possible to look through the form making use of the Review switch and read the form description to make certain it is the best for you.

- If the kind will not meet up with your preferences, make use of the Seach area to find the proper kind.

- When you are certain the form is suitable, click on the Purchase now switch to obtain the kind.

- Choose the costs program you would like and type in the required details. Build your bank account and pay for the order making use of your PayPal bank account or credit card.

- Choose the file structure and download the authorized papers web template for your gadget.

- Total, modify and print out and indicator the obtained Massachusetts Letter to Stockholders regarding authorization and sale of preferred stock and stock transfer restriction to protect tax benefits.

US Legal Forms is the biggest catalogue of authorized types in which you can discover various papers themes. Use the service to download professionally-created papers that stick to express requirements.

Form popularity

FAQ

When Do Convertible Preference Shares Convert? Usually, convertible preference shares convert upon a liquidity event. A liquidity event is generally a share or business acquisition or an initial public offering (IPO). Preference shares usually convert into ordinary shares automatically on an IPO.

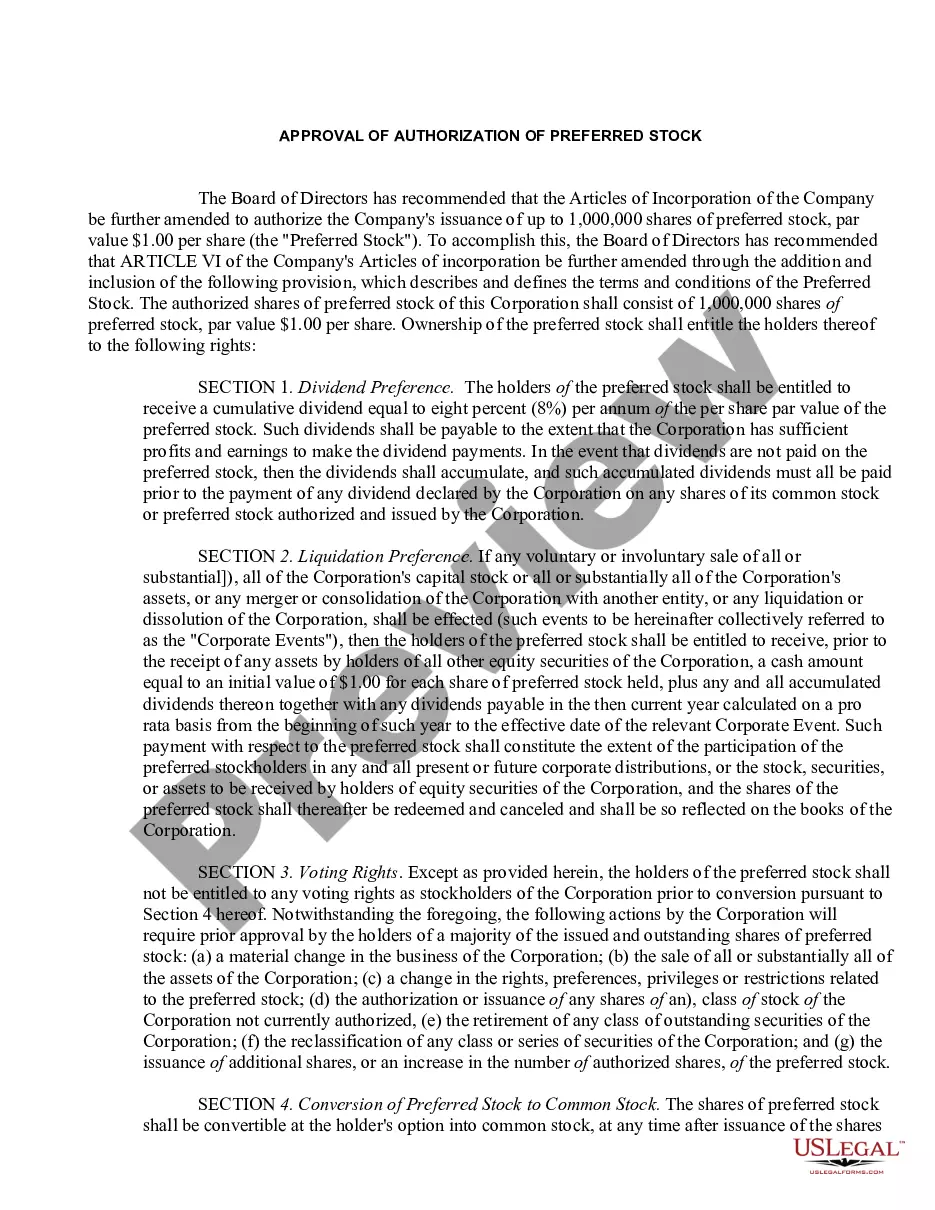

The conversion of the Preferred Stock is treated as an exchange of existing Preferred Stock for Common Stock in a transaction assumed to qualify as a tax-free reorganization under section 368(a)(1)(E).

Convertible preferred shares can be converted into common stock at a fixed conversion ratio. Once the market price of the company's common stock rises above the conversion price, it may be worthwhile for the preferred shareholders to convert and realize an immediate profit.

The conversion of preferred stock into common requires that any excess of the par value of the common shares issued over the carrying amount of the preferred being converted should be: reflected currently in income, but not as an extraordinary item.

The conversion of preferred stock into common stock is treated as a recapitalization for federal income tax purposes. [3] A single corporation recapitalization generally qualifies as a tax-free Type E reorganization (Section 368(a)(1)(E)).