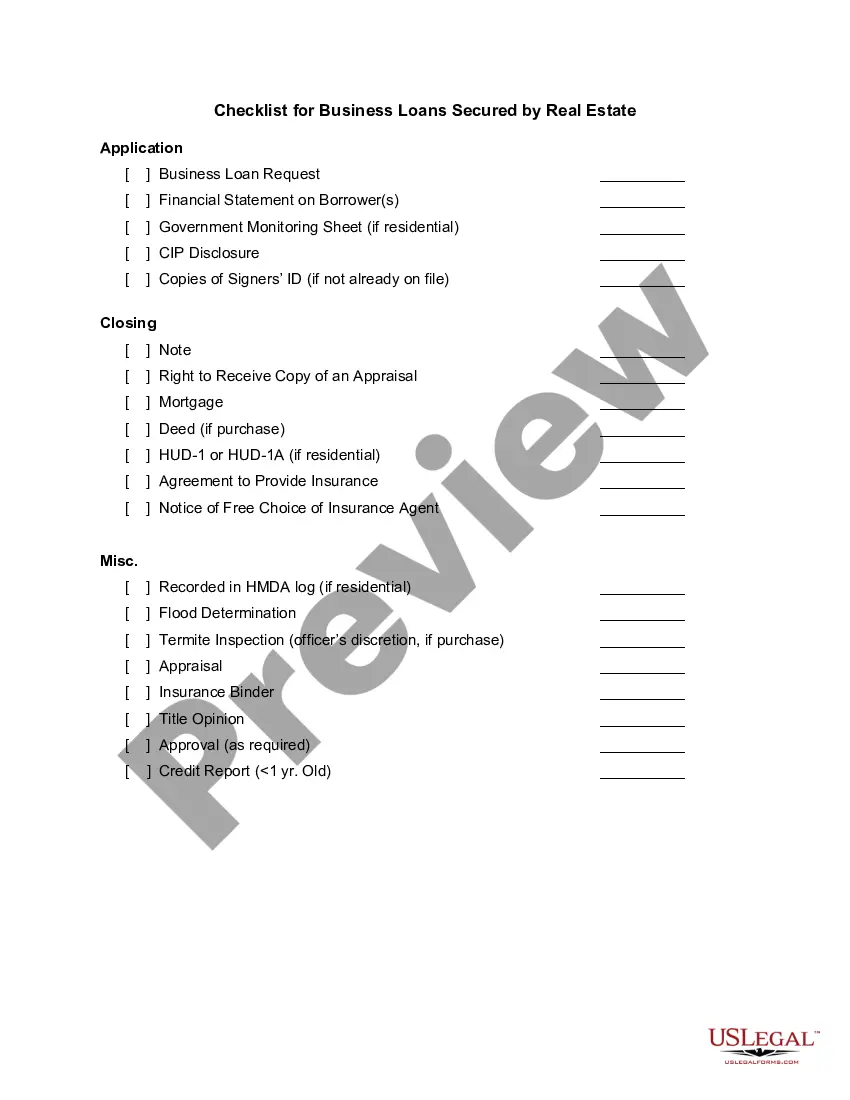

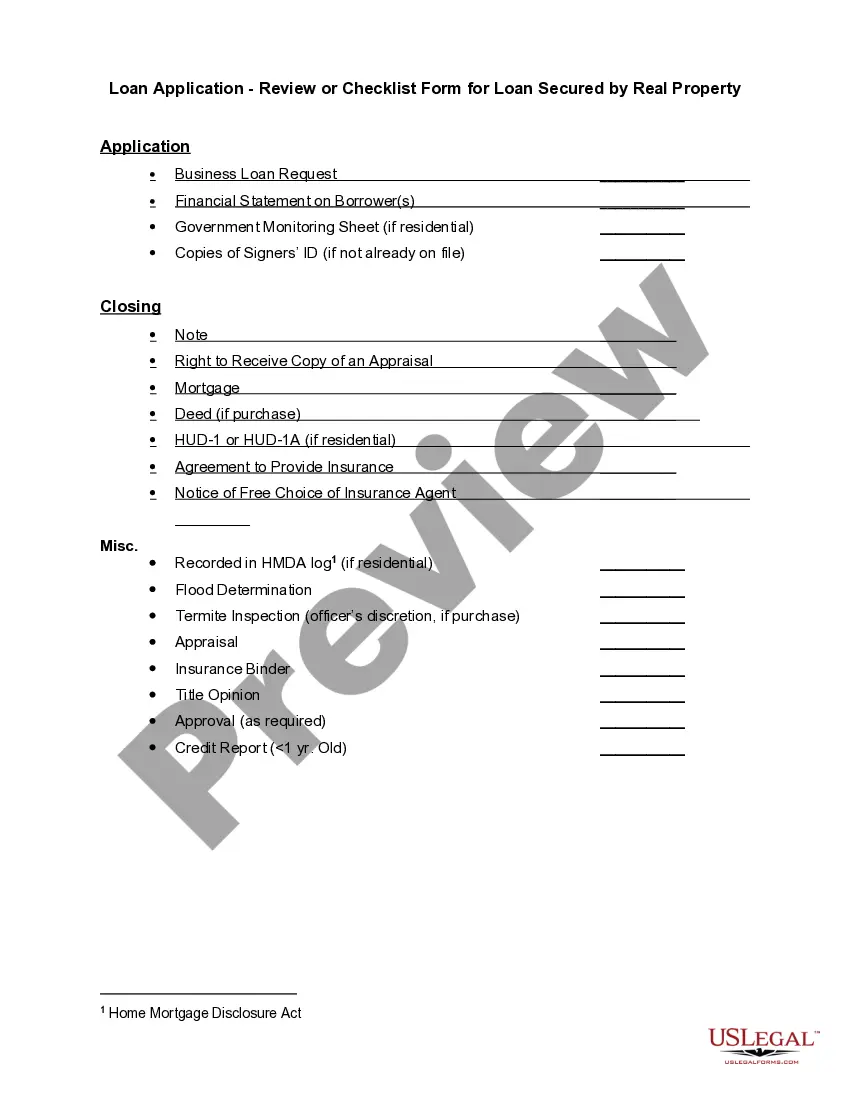

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Massachusetts Checklist for Real Estate Loans

State:

Multi-State

Control #:

US-CRE897

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Checklist For Real Estate Loans?

Choosing the right legitimate record format might be a struggle. Needless to say, there are a variety of layouts accessible on the Internet, but how can you obtain the legitimate form you want? Use the US Legal Forms internet site. The service delivers thousands of layouts, for example the Massachusetts Checklist for Real Estate Loans, which can be used for company and private needs. All of the forms are inspected by pros and fulfill state and federal needs.

When you are currently registered, log in to your profile and click on the Down load key to find the Massachusetts Checklist for Real Estate Loans. Make use of profile to search throughout the legitimate forms you may have acquired previously. Check out the My Forms tab of the profile and get an additional version in the record you want.

When you are a whole new user of US Legal Forms, listed here are straightforward guidelines so that you can adhere to:

- Very first, make sure you have chosen the appropriate form to your metropolis/region. You may check out the form while using Preview key and read the form outline to make certain this is the right one for you.

- When the form does not fulfill your preferences, make use of the Seach field to find the proper form.

- When you are sure that the form is acceptable, go through the Acquire now key to find the form.

- Opt for the rates program you need and type in the required information. Create your profile and buy an order with your PayPal profile or charge card.

- Opt for the document structure and obtain the legitimate record format to your product.

- Comprehensive, modify and printing and sign the acquired Massachusetts Checklist for Real Estate Loans.

US Legal Forms may be the biggest catalogue of legitimate forms where you will find a variety of record layouts. Use the company to obtain professionally-manufactured files that adhere to status needs.