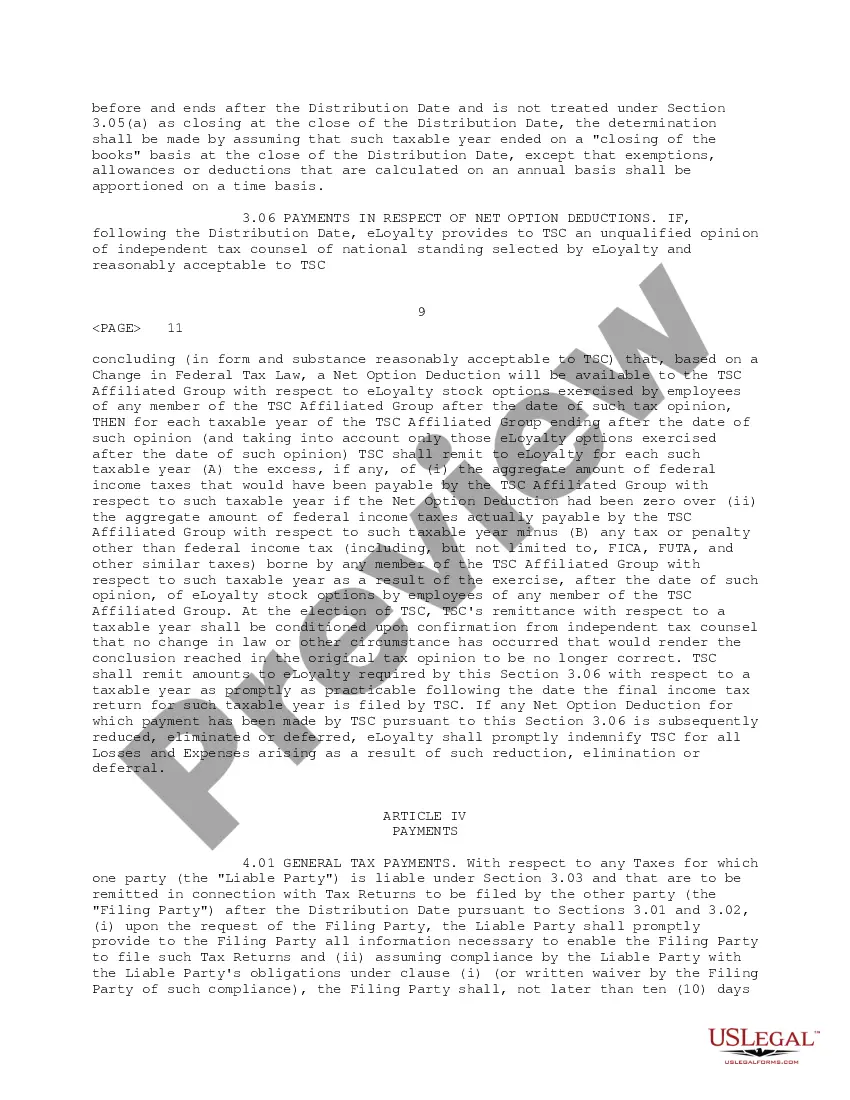

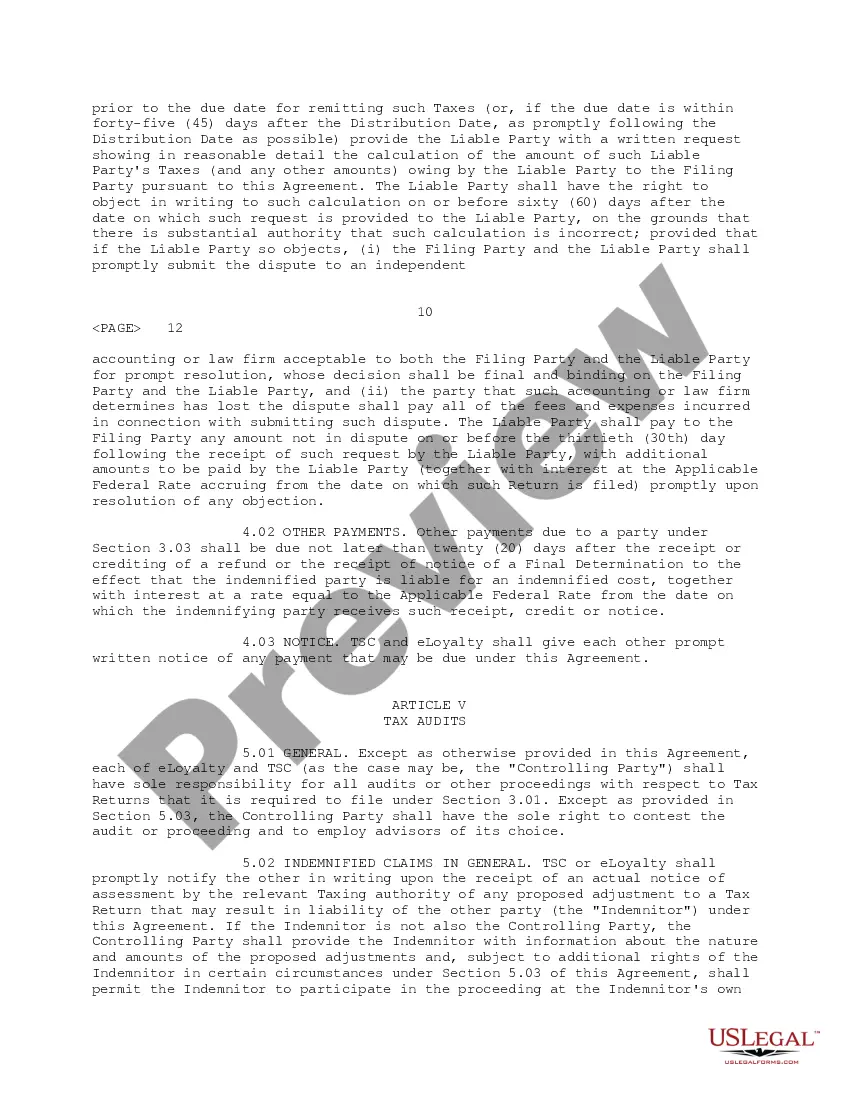

Massachusetts Tax Sharing and Disaffiliation Agreement is a legal agreement that outlines the terms and conditions related to the sharing and disaffiliation of tax liabilities between two or more entities in the state of Massachusetts. This agreement is primarily used when there is a change in the ownership, control, or structure of a business entity, which affects the distribution of tax liabilities. Keywords: Massachusetts, Tax Sharing, Disaffiliation Agreement, legal agreement, tax liabilities, ownership, control, structure, business entity. There are different types of Massachusetts Tax Sharing and Disaffiliation Agreements based on the specific circumstances of the agreement. Some of these types include: 1. Corporate Disaffiliation Agreement: This type of agreement is used when there is a change in ownership or control of a corporation, leading to the disaffiliation of its tax liabilities. It outlines the responsibilities of the parties involved in terms of the payment and allocation of taxes. 2. Partnership Disaffiliation Agreement: Partnership entities utilize this type of agreement when there is a change in the structure or ownership of the partnership, resulting in a need to distribute tax liabilities differently. The agreement defines the new tax sharing arrangements and the obligations of each partner. 3. Real Estate Disaffiliation Agreement: When there is a transfer of real estate holdings, such as residential or commercial properties, this agreement comes into play. It establishes how the tax liabilities related to the properties will be shared or reassigned among the parties involved. 4. Mergers and Acquisitions Disaffiliation Agreement: This type of agreement is used in situations where two companies merge or when one company acquires another. It addresses the allocation of tax liabilities between the merging entities or the acquiring and acquired entities. 5. Disaffiliation Agreement for Non-Profit Organizations: Non-profit organizations may utilize this agreement when there is a significant change in their structure, such as a merger or disaffiliation of branches or subsidiaries. It outlines the distribution of tax liabilities to ensure compliance with relevant tax laws. In summary, Massachusetts Tax Sharing and Disaffiliation Agreement is a vital legal document used to establish new tax liability arrangements when there is a change in ownership, control, or structure of a business entity in Massachusetts. The agreement type may vary depending on the specific circumstances, such as corporate disaffiliation, partnership disaffiliation, real estate disaffiliation, mergers and acquisitions, or non-profit organization restructuring.

Massachusetts Tax Sharing and Disaffiliation Agreement

Description

How to fill out Massachusetts Tax Sharing And Disaffiliation Agreement?

Are you currently in the place in which you need papers for sometimes company or personal purposes virtually every time? There are a lot of lawful papers layouts accessible on the Internet, but locating types you can rely on is not simple. US Legal Forms gives 1000s of form layouts, just like the Massachusetts Tax Sharing and Disaffiliation Agreement, which can be written in order to meet state and federal needs.

Should you be previously familiar with US Legal Forms site and possess a merchant account, basically log in. Next, you can obtain the Massachusetts Tax Sharing and Disaffiliation Agreement web template.

If you do not provide an profile and wish to begin to use US Legal Forms, abide by these steps:

- Find the form you will need and make sure it is for your right area/area.

- Utilize the Preview switch to analyze the shape.

- Look at the outline to actually have selected the correct form.

- When the form is not what you`re trying to find, utilize the Lookup area to obtain the form that fits your needs and needs.

- If you find the right form, click on Acquire now.

- Pick the prices plan you desire, fill in the necessary details to generate your account, and buy an order with your PayPal or Visa or Mastercard.

- Decide on a practical data file file format and obtain your version.

Get all of the papers layouts you might have purchased in the My Forms menus. You may get a more version of Massachusetts Tax Sharing and Disaffiliation Agreement whenever, if necessary. Just go through the needed form to obtain or produce the papers web template.

Use US Legal Forms, one of the most extensive selection of lawful kinds, to save lots of some time and stay away from blunders. The service gives appropriately manufactured lawful papers layouts that you can use for a variety of purposes. Make a merchant account on US Legal Forms and start generating your daily life a little easier.