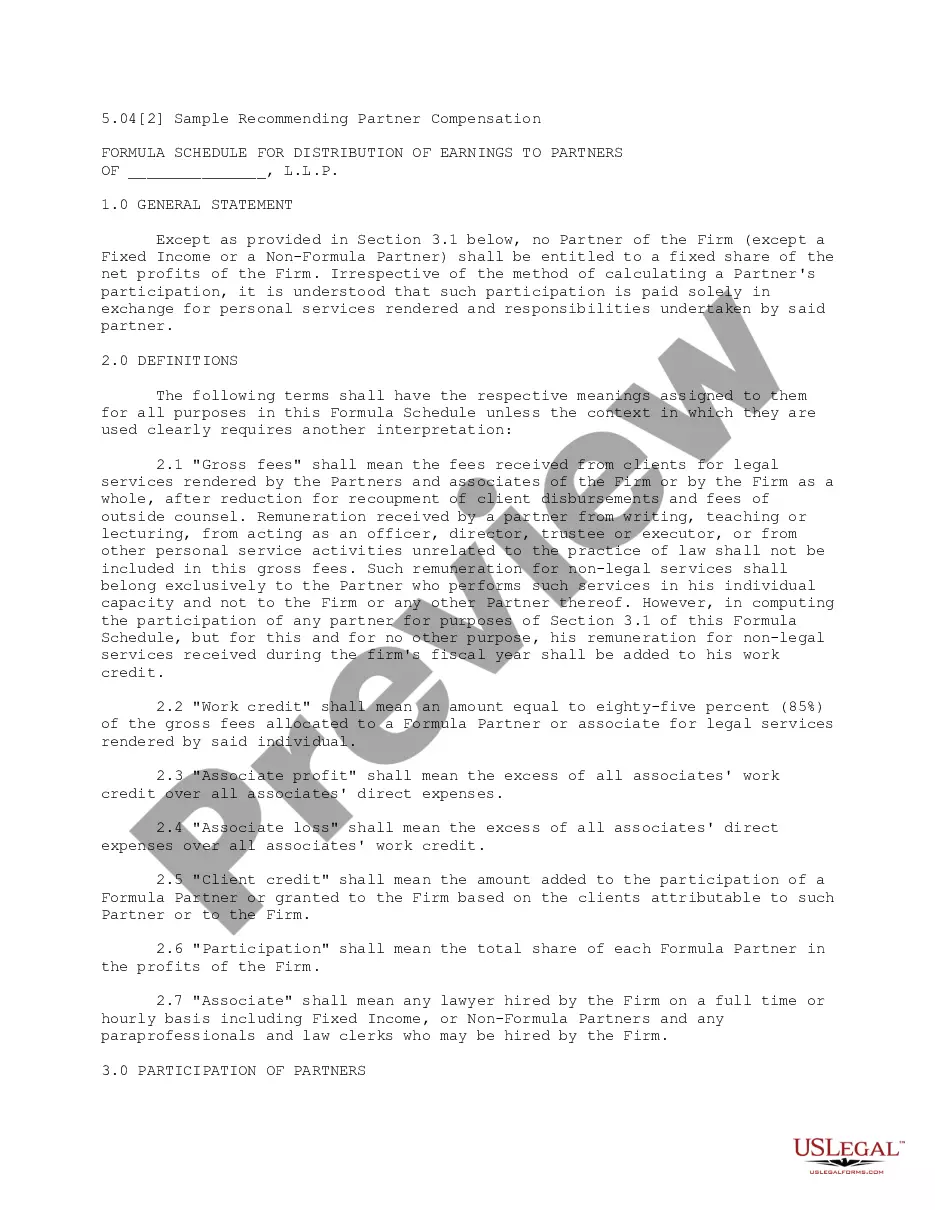

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

Massachusetts Formula System for Distribution of Earnings to Partners

Category:

State:

Multi-State

Control #:

US-L05041A

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out Formula System For Distribution Of Earnings To Partners?

Are you within a placement the place you need to have documents for possibly organization or individual purposes just about every day? There are a variety of authorized papers web templates available on the Internet, but discovering ones you can trust isn`t simple. US Legal Forms offers thousands of develop web templates, like the Massachusetts Formula System for Distribution of Earnings to Partners, which are written to fulfill state and federal requirements.

When you are previously informed about US Legal Forms web site and have an account, merely log in. Following that, you may acquire the Massachusetts Formula System for Distribution of Earnings to Partners format.

Unless you provide an profile and would like to begin using US Legal Forms, abide by these steps:

- Discover the develop you require and make sure it is for that proper metropolis/county.

- Make use of the Review option to check the form.

- Read the outline to actually have selected the right develop.

- When the develop isn`t what you are trying to find, utilize the Lookup area to find the develop that meets your needs and requirements.

- Whenever you find the proper develop, simply click Purchase now.

- Opt for the costs plan you want, submit the required details to generate your account, and purchase an order making use of your PayPal or charge card.

- Select a practical data file structure and acquire your duplicate.

Get each of the papers web templates you may have purchased in the My Forms food list. You can obtain a further duplicate of Massachusetts Formula System for Distribution of Earnings to Partners anytime, if needed. Just click the essential develop to acquire or print out the papers format.

Use US Legal Forms, the most comprehensive variety of authorized types, to conserve time and steer clear of mistakes. The support offers expertly made authorized papers web templates which can be used for an array of purposes. Make an account on US Legal Forms and commence creating your lifestyle a little easier.

Form popularity

FAQ

The apportionment percentage is determined by adding the taxpayer's receipts factor, property factor and payroll factor together and dividing the sum by three.

The net income for a partnership is divided between the partners as called for in the partnership agreement. The income summary account is closed to the respective partner capital accounts. The respective drawings accounts are closed to the partner capital accounts.

Ordinarily, a partner is not taxed on a current distribution because it represents a withdrawal of his previously taxed share of partnership income or a return of his capital contribution.

A partnership must file an annual information return to report the income, deductions, gains, losses, etc., from its operations, but it does not pay income tax. Instead, it "passes through" profits or losses to its partners.

A partnership is not taxable on the income of the entity. Each partner includes his or her share of the partnership's income or loss on his or her tax return. Get more information and filing requirements for general partnerships and limited partnerships.

Generally, a partnership doesn't pay tax on its income but ?passes through? any profits or losses to its partners. Partners must include partnership items on their tax returns.

Partnerships are considered pass-through entities. That means that any income or losses are passed through the partnership to the individual owners, who are then responsible to account for that income or loss on their income tax returns.