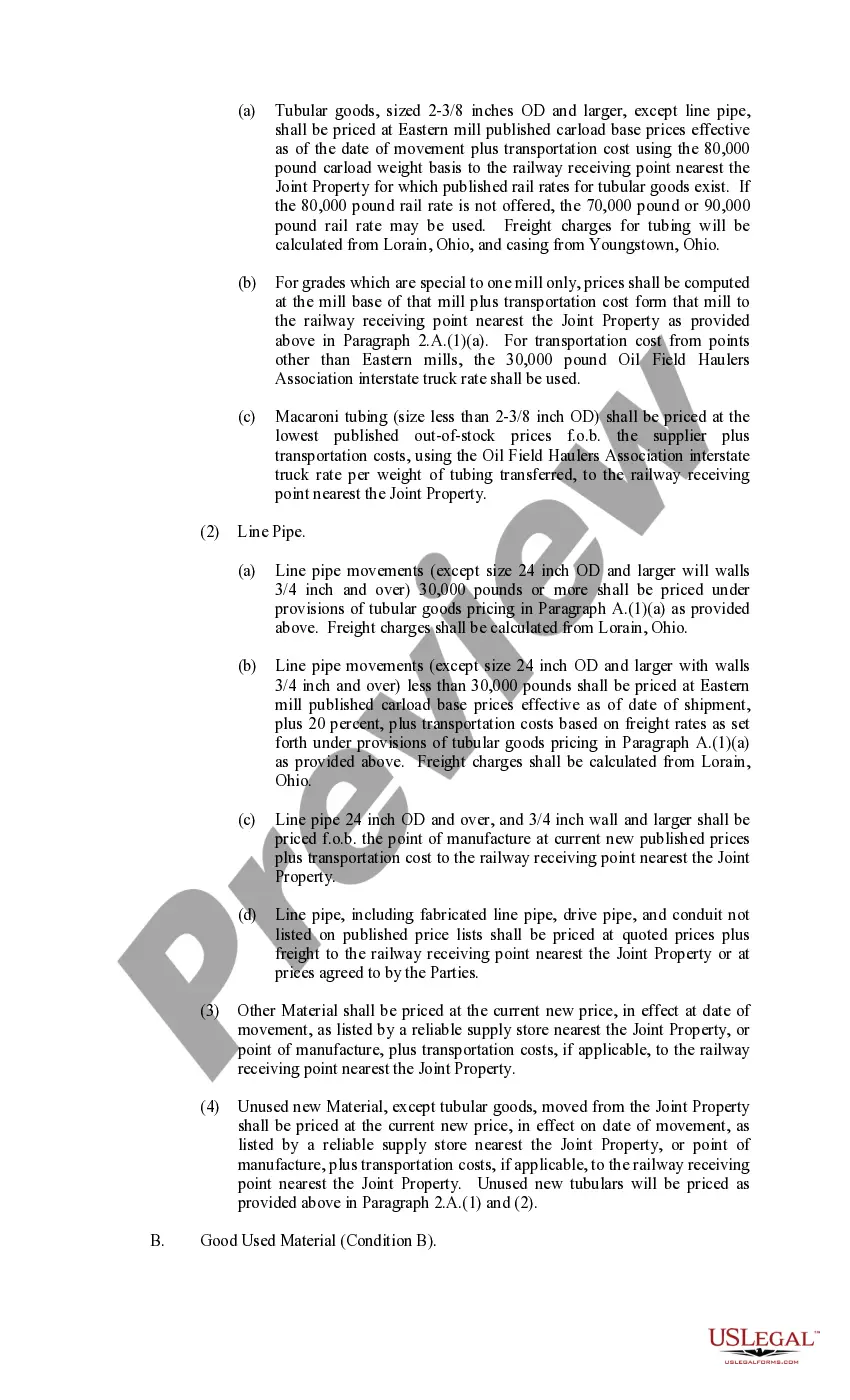

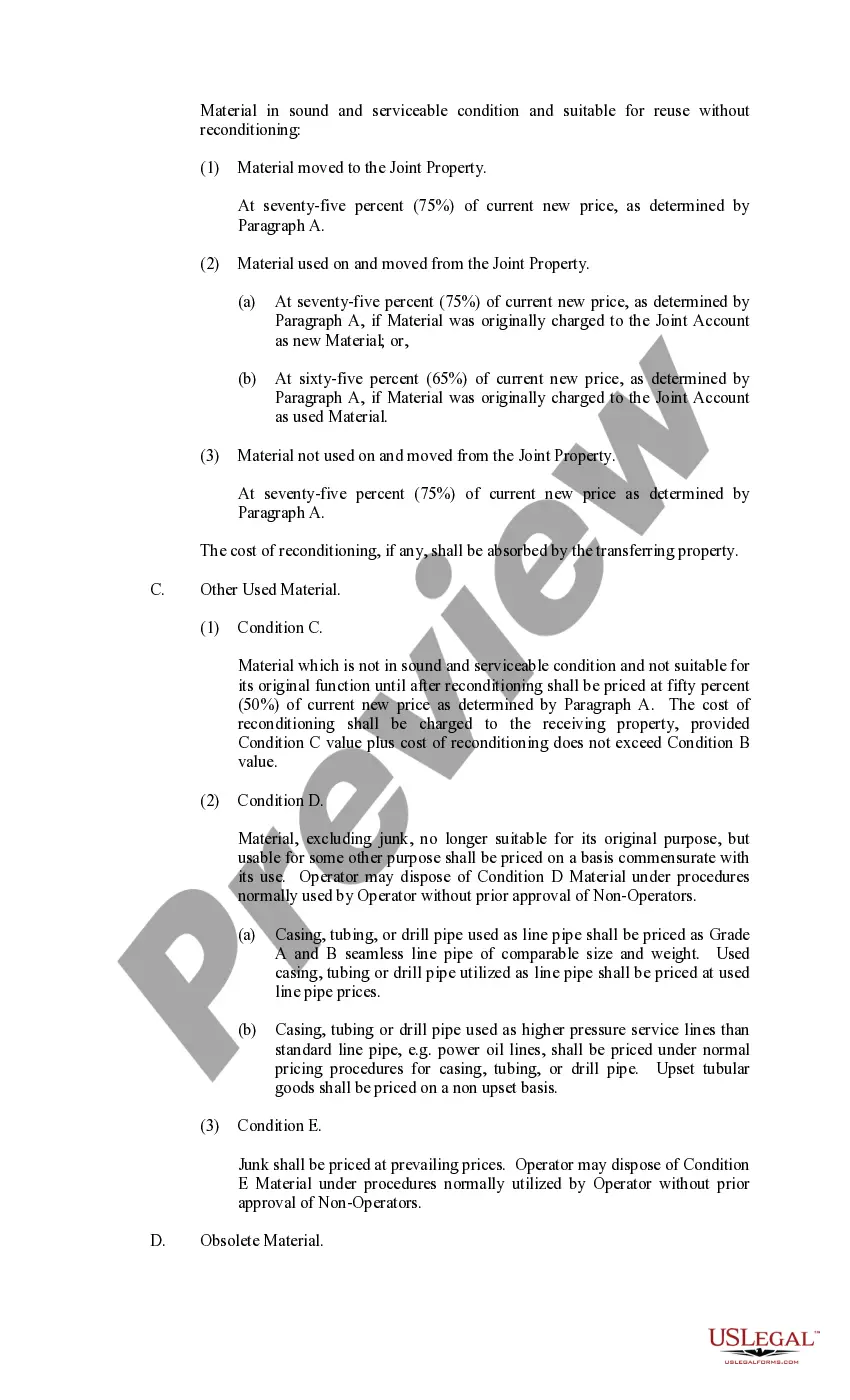

Massachusetts Exhibit C Accounting Procedure Joint Operations is a set of guidelines and procedures followed by businesses and organizations in the state of Massachusetts. These procedures are specifically designed to govern joint operations between companies and ensure accurate financial reporting and accounting practices. The term "joint operations" refers to situations where two or more entities collaborate to achieve a mutual goal while sharing resources, risks, and rewards. In Massachusetts, Exhibit C denotes the accounting procedures specifically drafted and approved by the Secretary of the Executive Office for Administration and Finance. This accounting procedure outlines various aspects of joint operations, including financial reporting, cost allocation, revenue recognition, and other related accounting practices. It ensures that participating entities properly account for their contributions, expenses, revenues, and any potential gains or losses resulting from the joint venture. The Massachusetts Exhibit C Accounting Procedure Joint Operations are of several types, each catering to specific industries, partnerships, or business structures. Some commonly known types include: 1. Joint Venture Exhibit C: This procedure is applicable when two or more entities enter into a contractual agreement to carry out a specific project or venture. The joint venture partners are required to adhere to the accounting procedures outlined in this Exhibit C to report and account for their contributions and financial activities. 2. Consortium Exhibit C: When multiple companies or organizations collaborate to achieve a shared objective, such as research and development projects, educational programs, or infrastructure initiatives, the Consortium Exhibit C comes into play. This accounting procedure ensures that all consortium members follow consistent accounting practices to accurately report their financial transactions and obligations. 3. Public-Public Partnership Exhibit C: In instances where two or more public sector entities join forces providing public services or execute public works projects, the Public-Public Partnership Exhibit C sets the accounting standards. This procedure allows public entities to effectively manage joint operations, allocate costs, and fulfill reporting requirements transparently. 4. Public-Private Partnership Exhibit C: When a government entity collaborates with a private business or organization to carry out projects of public interest, the Public-Private Partnership Exhibit C governs the accounting practices. This procedure ensures that funds provided by the government and private partners are accurately accounted for, and the financial records remain transparent. Ultimately, Massachusetts Exhibit C Accounting Procedure Joint Operations serves as a crucial tool for businesses, government entities, and organizations engaged in various collaborative ventures in Massachusetts. It establishes a clear framework for accounting practices, enabling accurate financial reporting, promoting transparency, and ensuring compliance under the state's accounting regulations.

Massachusetts Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Massachusetts Exhibit C Accounting Procedure Joint Operations?

Finding the right legal papers web template could be a battle. Obviously, there are tons of templates available on the net, but how would you discover the legal develop you will need? Make use of the US Legal Forms internet site. The services delivers 1000s of templates, like the Massachusetts Exhibit C Accounting Procedure Joint Operations, which you can use for business and private needs. All of the forms are checked by specialists and meet up with state and federal demands.

Should you be previously signed up, log in to the account and click the Download option to get the Massachusetts Exhibit C Accounting Procedure Joint Operations. Make use of account to look throughout the legal forms you possess purchased earlier. Go to the My Forms tab of the account and obtain one more duplicate of your papers you will need.

Should you be a new consumer of US Legal Forms, listed here are simple directions that you should comply with:

- Initial, make certain you have selected the right develop for your personal town/county. It is possible to look through the form while using Preview option and read the form information to ensure it will be the best for you.

- If the develop is not going to meet up with your requirements, take advantage of the Seach industry to find the right develop.

- Once you are sure that the form is suitable, click the Acquire now option to get the develop.

- Pick the prices prepare you want and enter the needed details. Create your account and purchase your order utilizing your PayPal account or charge card.

- Opt for the file formatting and acquire the legal papers web template to the product.

- Comprehensive, change and printing and indicator the attained Massachusetts Exhibit C Accounting Procedure Joint Operations.

US Legal Forms is the most significant local library of legal forms in which you will find numerous papers templates. Make use of the service to acquire professionally-produced papers that comply with state demands.

Form popularity

FAQ

The correct answer is option B) APB Opinions. The pronouncement issued by the Accounting Principles Board is called the APB Opinions. Which of the following pronouncements were issued by ... study.com ? explanation ? which-of-th... study.com ? explanation ? which-of-th...

Established in 1973, the Financial Accounting Standards Board (FASB) is the independent, private- sector, not-for-profit organization based in Norwalk, Connecticut, that establishes financial accounting and reporting standards for public and private companies and not-for-profit organizations that follow Generally ... About the FASB fasb.org ? facts fasb.org ? facts

Joint venture accounting involves sharing of financial data relevant to enterprises that are engaged in a joint venture. Gain full visibility into capital and operating expenses using joint-venture software from SAP.

CAP is the predecessor of the Accounting Principles Board, itself a predecessor to the Financial Accounting Standards Board. Its formation and activities were early efforts to rationalize and legitimize the reporting of business performance. However, it is widely regarded as having failed. Committee on Accounting Procedure - Wikipedia Wikipedia ? wiki ? Committee_on_Acco... Wikipedia ? wiki ? Committee_on_Acco...

The pronouncements that were issued by the Committee on Accounting Procedures were related to the issues faced in accounting and reporting by the organizations. This committee was established to set the standards related to accounting in the U.S.

In response to the SEC's Accounting Series Release No. 4, the American Institute of Accountants () reorganized its Committee on Accounting Procedure (CAP) in 1939 and increased it from 8 to 22 members, all accounting practitioners except for three academicians. The Richard C. Adkerson Gallery on the SEC Role in Accounting ... sechistorical.org ? museum ? galleries ? rca sechistorical.org ? museum ? galleries ? rca