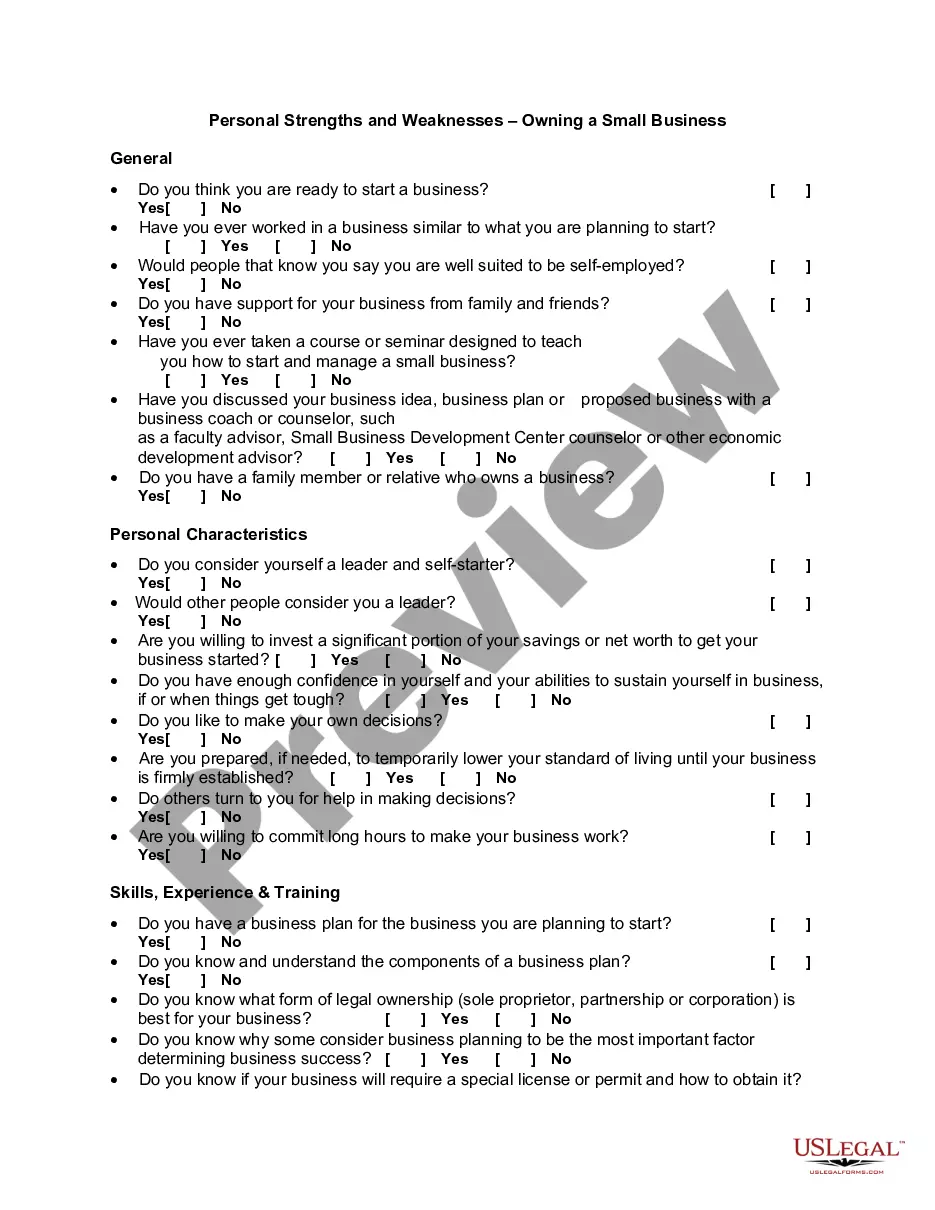

This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

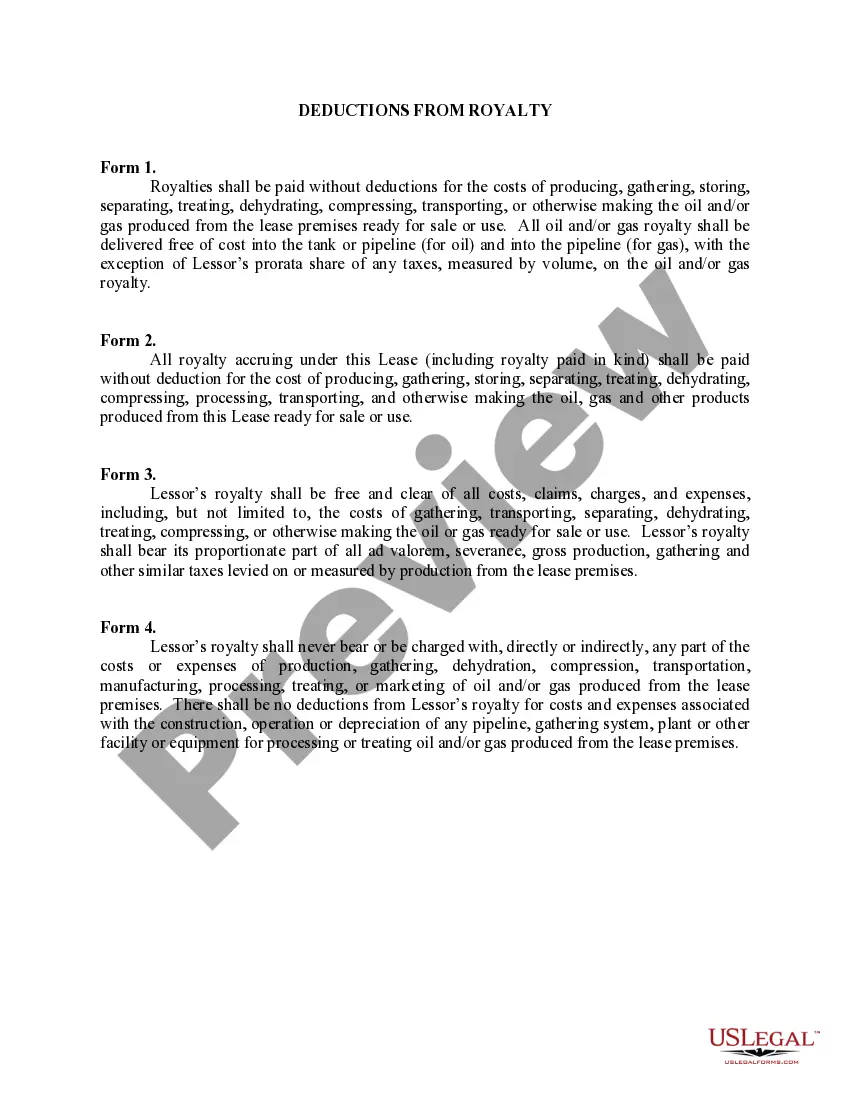

Massachusetts Deductions from Royalty refer to the various deductions that individuals or businesses can claim on their taxes in the state of Massachusetts related to royalties received. These deductions allow taxpayers to reduce their taxable income by deducting certain expenses associated with the generation of royalty income. Here are some relevant keywords and types of Massachusetts Deductions from Royalty: 1. Royalty Income: This deduction applies to any income derived from royalty payments, such as fees received for intellectual property rights, licensing, or creative works. 2. Massachusetts Source Income: Taxpayers can deduct expenses related to their royalty income generated from sources within Massachusetts. These may include expenses incurred for marketing, production, or promotion of the intellectual property within the state. 3. Production Costs: Individuals or businesses engaged in the production of royalty-generating works, such as films, music albums, or books, can deduct costs directly associated with the production process. This can include expenses for studio rentals, equipment, staff salaries, post-production, or distribution costs. 4. Marketing and Promotion: Deductions can be claimed for expenses incurred in marketing, advertising, and promotion of the royalty-earning works. This includes costs related to website development, advertising campaigns, public relations, trade shows, or other promotional activities aimed at maximizing the potential revenue from the intellectual property. 5. Legal and Professional Fees: Taxpayers can deduct fees paid to attorneys, accountants, or other professionals for services directly related to the generation and protection of royalty income. This includes legal services for copyright or patent registrations, licensing agreements, royalty audits, or financial management. 6. Home Office Expenses: If the royalty-generating activities are conducted from a home office, deductions can be claimed for a portion of rent, utilities, insurance, and other related expenses, based on the percentage of space used solely for business purposes. 7. Depreciation: Taxpayers can claim deductions for the depreciation of assets used in the production or licensing of the royalty-earning works. This may include equipment, software, or other capital assets that have a limited lifespan. It is important to note that each deduction may have specific eligibility criteria and documentation requirements. Taxpayers should consult with a tax professional or refer to the relevant Massachusetts tax regulations for detailed guidelines on claiming these deductions.Massachusetts Deductions from Royalty refer to the various deductions that individuals or businesses can claim on their taxes in the state of Massachusetts related to royalties received. These deductions allow taxpayers to reduce their taxable income by deducting certain expenses associated with the generation of royalty income. Here are some relevant keywords and types of Massachusetts Deductions from Royalty: 1. Royalty Income: This deduction applies to any income derived from royalty payments, such as fees received for intellectual property rights, licensing, or creative works. 2. Massachusetts Source Income: Taxpayers can deduct expenses related to their royalty income generated from sources within Massachusetts. These may include expenses incurred for marketing, production, or promotion of the intellectual property within the state. 3. Production Costs: Individuals or businesses engaged in the production of royalty-generating works, such as films, music albums, or books, can deduct costs directly associated with the production process. This can include expenses for studio rentals, equipment, staff salaries, post-production, or distribution costs. 4. Marketing and Promotion: Deductions can be claimed for expenses incurred in marketing, advertising, and promotion of the royalty-earning works. This includes costs related to website development, advertising campaigns, public relations, trade shows, or other promotional activities aimed at maximizing the potential revenue from the intellectual property. 5. Legal and Professional Fees: Taxpayers can deduct fees paid to attorneys, accountants, or other professionals for services directly related to the generation and protection of royalty income. This includes legal services for copyright or patent registrations, licensing agreements, royalty audits, or financial management. 6. Home Office Expenses: If the royalty-generating activities are conducted from a home office, deductions can be claimed for a portion of rent, utilities, insurance, and other related expenses, based on the percentage of space used solely for business purposes. 7. Depreciation: Taxpayers can claim deductions for the depreciation of assets used in the production or licensing of the royalty-earning works. This may include equipment, software, or other capital assets that have a limited lifespan. It is important to note that each deduction may have specific eligibility criteria and documentation requirements. Taxpayers should consult with a tax professional or refer to the relevant Massachusetts tax regulations for detailed guidelines on claiming these deductions.