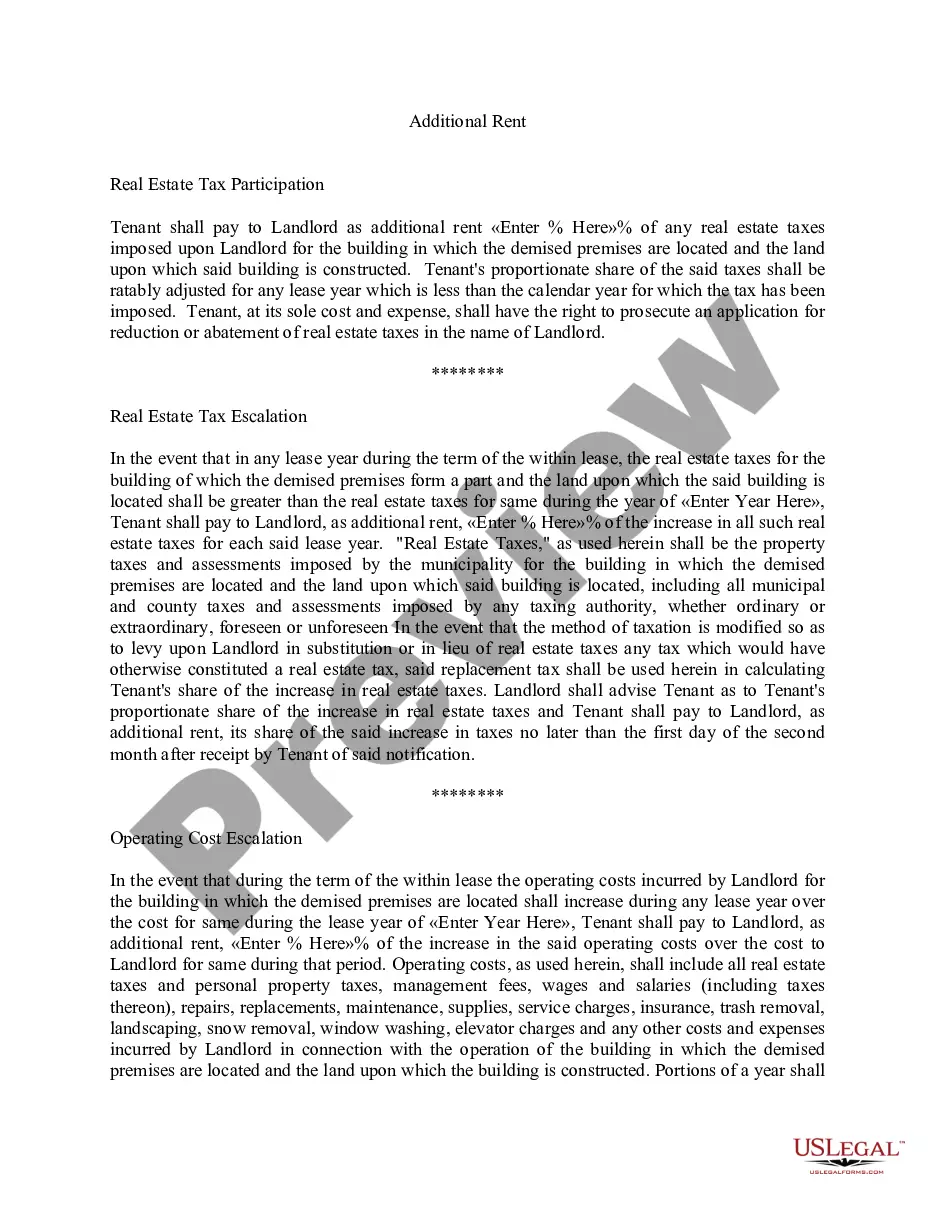

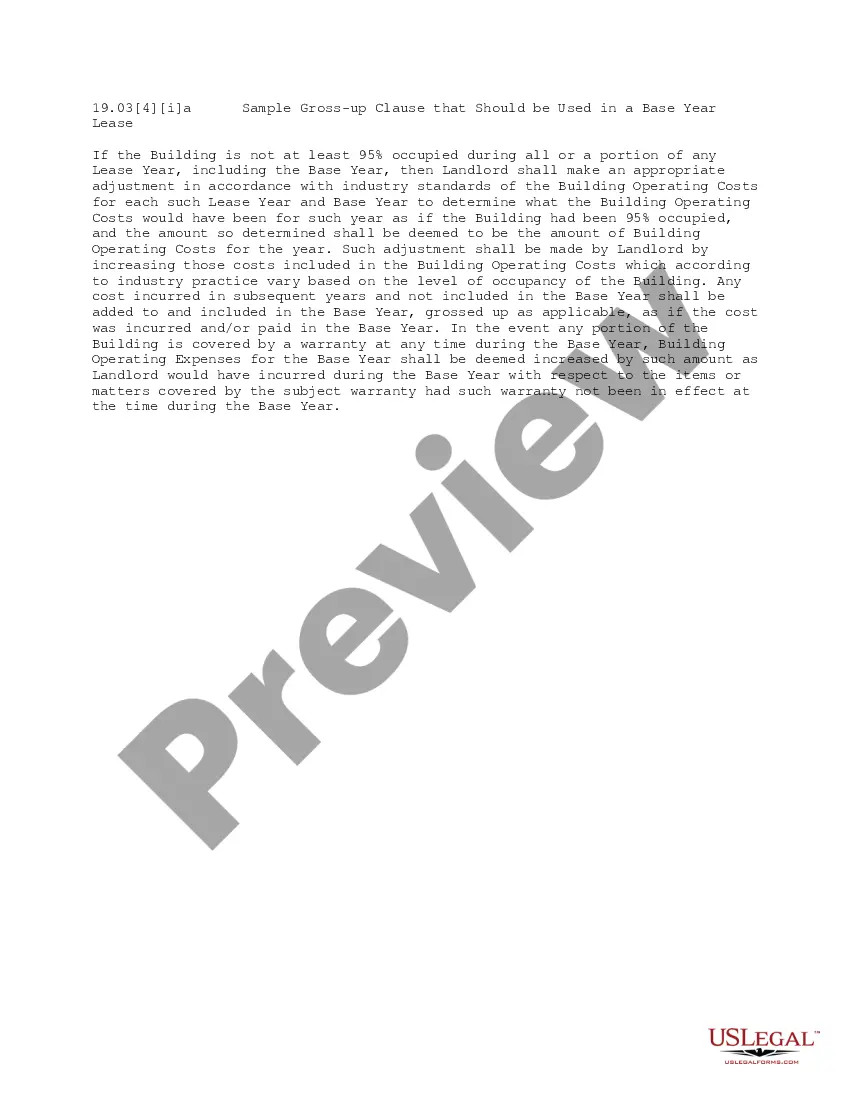

This form is a clause regarding additional rent element of an office lease providing for tax increases. The tax increases pertain to assessments and special assessments levied, assessed or imposed upon the building and/or the land under, including any land(s) dedicated to the use of, the building, by any governmental bodies or authorities.

Massachusetts Tax Increase Clause

Category:

State:

Multi-State

Control #:

US-OL19033GA

Format:

Word;

PDF

Instant download

Description

Free preview

How to fill out Tax Increase Clause?

Finding the right authorized papers design could be a have a problem. Naturally, there are a variety of web templates accessible on the Internet, but how do you obtain the authorized type you will need? Utilize the US Legal Forms internet site. The support delivers thousands of web templates, such as the Massachusetts Tax Increase Clause, which you can use for company and private requirements. All the types are examined by specialists and meet federal and state specifications.

Should you be currently signed up, log in to the account and then click the Down load switch to have the Massachusetts Tax Increase Clause. Make use of account to check from the authorized types you may have bought previously. Visit the My Forms tab of your own account and have another duplicate of the papers you will need.

Should you be a new customer of US Legal Forms, listed below are basic guidelines for you to follow:

- Initial, make certain you have selected the proper type to your city/region. You may look through the form making use of the Review switch and look at the form outline to make certain this is the best for you.

- If the type is not going to meet your expectations, use the Seach discipline to obtain the appropriate type.

- Once you are sure that the form would work, go through the Get now switch to have the type.

- Choose the pricing program you would like and enter in the essential info. Design your account and pay money for the transaction using your PayPal account or charge card.

- Select the data file file format and acquire the authorized papers design to the gadget.

- Complete, change and produce and signal the obtained Massachusetts Tax Increase Clause.

US Legal Forms is definitely the most significant catalogue of authorized types in which you will find different papers web templates. Utilize the company to acquire appropriately-made papers that follow status specifications.

Form popularity

FAQ

Short-term capital gains will now be taxed at 8.5%, instead of the previous 12%, effective as of January 1, 2023. Note, however, that if the Massachusetts ?millionaires tax? applies, its 4% surtax will bring the rate on short-term capital gains to 12.5%.

If you have a lease , the only way that a landlord can raise your rent before the lease ends is through what is called a "tax escalator clause." A tax escalator clause in a lease allows your landlord to pass on to you any increase in your landlord's property taxes by increasing your rent before the lease term ends.

Short-term capital gains will now be taxed at 8.5%, instead of the previous 12%, effective as of January 1, 2023. Note, however, that if the Massachusetts ?millionaires tax? applies, its 4% surtax will bring the rate on short-term capital gains to 12.5%.

You must be 70 or older. For Clauses 41C and 41C½, the eligible age may be reduced to 65 or older, by vote of the legislative body of your city or town. You must own and occupy the property as your domicile.

Under Proposition 2½, a municipality is subject to two property tax limits: Ceiling: The total annual property tax revenue raised by a municipality shall not exceed 2.5% of the assessed value of all taxable property contained in it.

2023, c. 50. The new law amended the estate tax by providing a credit of up to $99,600, thereby eliminating the tax for estates valued at $2 million or less and reducing the tax for estates valued at more than $2 million. Below, you will find answers to frequently asked questions regarding these recent changes.

The property tax levy limit cannot be increased more than the 2 ½ % over the prior years levy limit unless it gets voters' approval to override the cap. (Important note: Levy limit provisions of Proposition 2 ½ affect the total amount of taxes to be raised by a city or town and do not apply to individual tax bills.)

Effective November 1, 2023, FTB will accept signature alternative methods for taxpayers or their representatives to submit paper tax returns and other documents that require original signatures, except for Power of Attorney (POA) declarations and Tax Authorization Information (TIA) forms.