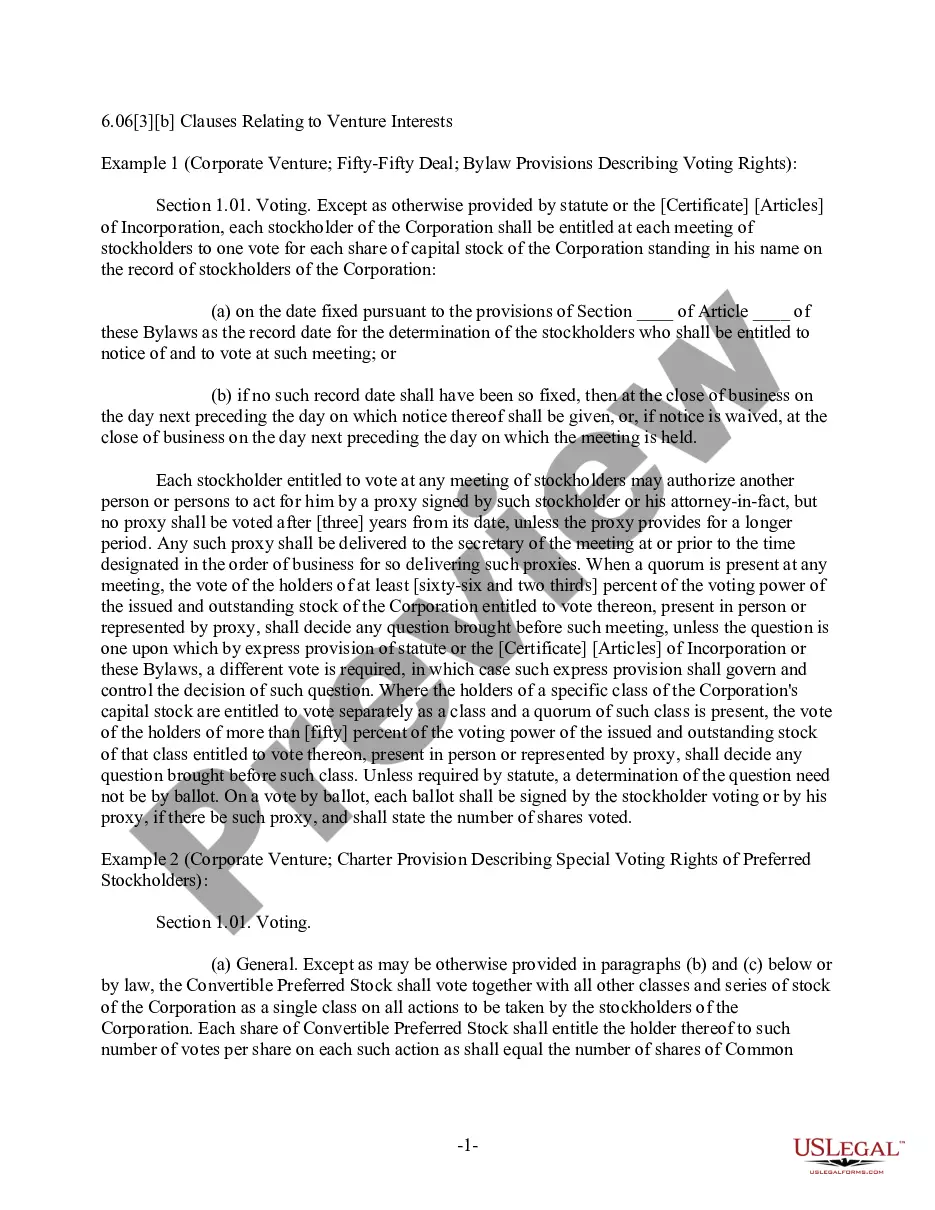

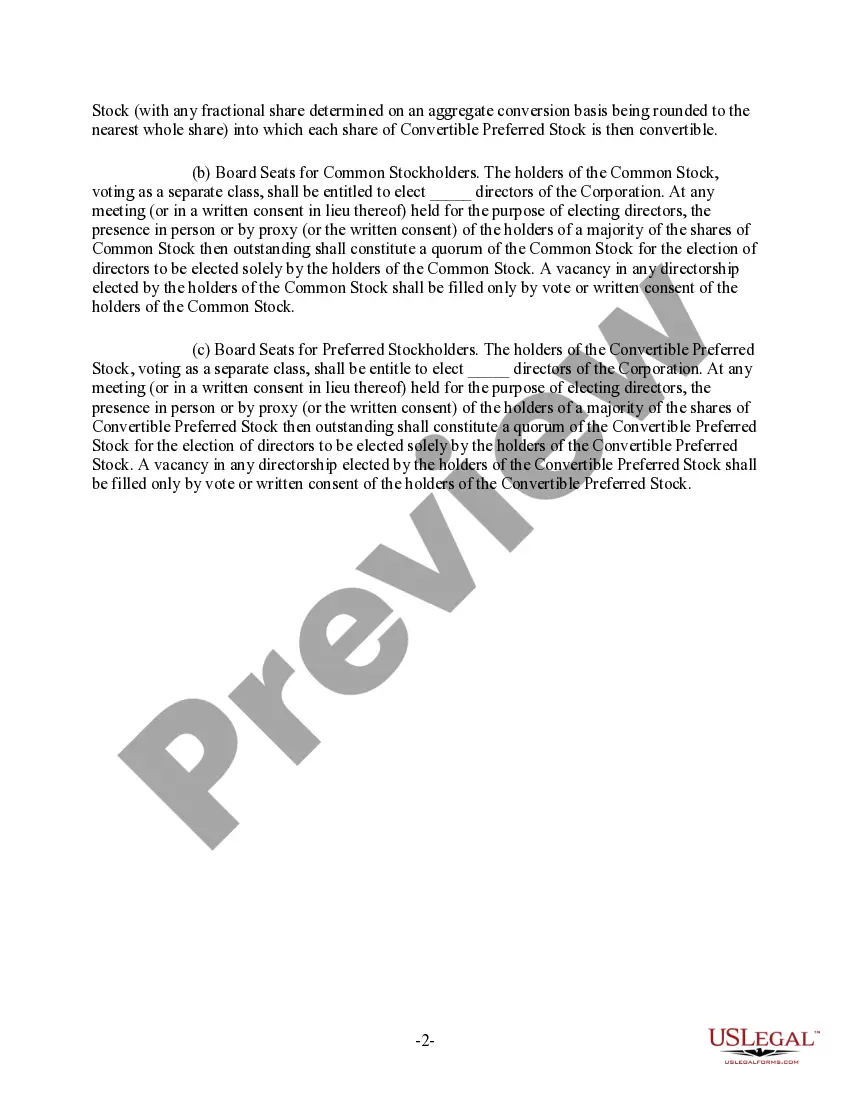

Massachusetts Clauses Relating to Venture Interests are legal provisions that govern the rights, obligations, and responsibilities of individuals or entities involved in venture capital investments or partnerships in the state of Massachusetts. These clauses are essential in protecting the interests of both the venture capitalists (VCs) and the entrepreneurs seeking funding or partnerships for their startups or business ventures. There are several types of Massachusetts Clauses Relating to Venture Interests, including: 1. Non-Disclosure Agreement (NDA): This clause ensures the confidentiality of proprietary or sensitive information shared between the venture capitalist and the entrepreneur during the investment process. It prevents either party from disclosing or using the information for any purpose other than evaluating the investment opportunity. 2. Independent Contractor Agreement: This clause defines the relationship between the venture capitalist and the entrepreneur as that of an independent contractor rather than an employer-employee. It clarifies that the entrepreneur is responsible for their own taxes, benefits, and liabilities, and that they are not entitled to employee benefits or protections. 3. Vesting Agreement: This clause outlines the conditions under which the entrepreneur's ownership in the startup or venture capital investment becomes fully vested. It often includes a vesting schedule specifying the amount of ownership the entrepreneur earns over time, usually tied to their continued involvement in the business. 4. Anti-Dilution Protection: This clause protects the venture capitalist from significant equity dilution in subsequent funding rounds. It provides the VC with additional shares or the ability to purchase additional shares at a discounted price if subsequent financing rounds occur at a lower valuation than the initial investment. 5. Drag-Along Rights: This clause grants the majority shareholders or venture capitalists the power to force minority shareholders to sell their shares in the event of a sale or merger of the company. It ensures that the VC can easily sell the entire business without facing resistance from minority shareholders. 6. Board Representation: This clause defines the rights of the venture capitalist to appoint board members or observe board meetings. It enables the VC to actively participate in the strategic decision-making process of the startup or business venture. 7. Liquidation Preference: This clause determines the priority order in which proceeds from a sale or liquidation of the company are distributed. It ensures that the venture capitalist receives a preferred return on their investment before any other stakeholders. 8. Right of First Refusal: This clause grants the venture capitalist the first opportunity to invest in subsequent funding rounds or purchase shares from existing shareholders. It allows the VC to maintain their ownership percentage and protect their investment from dilution. It is important to note that the specific clauses and their terms may vary depending on the nature of the venture, the parties involved, and the specific negotiation between the venture capitalist and the entrepreneur. These clauses provide a legal framework that outlines the expectations and obligations of both parties, facilitating a successful and mutually beneficial venture capital relationship in Massachusetts.

Massachusetts Clauses Relating to Venture Interests

Description

How to fill out Massachusetts Clauses Relating To Venture Interests?

Are you presently in the situation the place you require files for both organization or personal uses nearly every day time? There are plenty of lawful record themes available online, but getting types you can trust isn`t easy. US Legal Forms provides 1000s of type themes, much like the Massachusetts Clauses Relating to Venture Interests, that happen to be published to meet federal and state needs.

When you are currently informed about US Legal Forms internet site and have an account, just log in. Next, you are able to obtain the Massachusetts Clauses Relating to Venture Interests web template.

If you do not have an profile and need to begin to use US Legal Forms, follow these steps:

- Find the type you require and ensure it is for that proper area/state.

- Utilize the Review option to review the form.

- See the outline to actually have selected the correct type.

- If the type isn`t what you`re searching for, make use of the Research industry to obtain the type that meets your needs and needs.

- Once you obtain the proper type, click on Acquire now.

- Choose the prices strategy you desire, fill out the required information and facts to create your bank account, and pay for the order using your PayPal or bank card.

- Select a hassle-free paper format and obtain your duplicate.

Locate every one of the record themes you may have purchased in the My Forms menus. You can aquire a extra duplicate of Massachusetts Clauses Relating to Venture Interests whenever, if necessary. Just click on the needed type to obtain or produce the record web template.

Use US Legal Forms, probably the most considerable selection of lawful types, to save some time and steer clear of mistakes. The support provides appropriately created lawful record themes that you can use for an array of uses. Generate an account on US Legal Forms and begin creating your way of life a little easier.

Form popularity

FAQ

Structuring A Joint Venture Agreement: 8 Important Elements 8 Key Elements in a Joint Venture Agreement. ... The identity of the businesses involved. ... The purpose of the joint venture. ... Resources to be shared. ... Sharing of profits and losses. ... Rights and duties. ... Dispute resolution. ... Governance.

Since the joint venture is not a legal entity, it does not enter into contracts, hire employees, or have its own tax liabilities. These activities and obligations are handled through the co-venturers directly and are governed by contract law.

Rules for joint ventures Pay no more than 85% of the amount paid by the government to non-similarly situated firms for construction contracts. Pay no more than 75% of the amount paid by the government to non-similarly situated firms for special trade contracts.

Although a JV is a partnership in the colloquial sense of the word, it can be formed using any legal structure: Corporations, partnerships, limited liability companies (LLCs), and other business entities can all be employed.

Ing to Massachusetts' ?joint venture? theory, a defendant may be charged with a crime if he aided or abetted the person who committed the criminal act. (3) by agreement is willing and available to help the other if necessary. Commonwealth v. Cohen, 412 Mass.

Joint venture An agreement (written or oral) between the parties manifesting their intent to associate as joint venturers. Mutual contributions by the parties to the joint venture. Some degree of joint control over the single enterprise or project. A mechanism or provision for the sharing of profits or losses.

The common elements necessary to establish the existence of a joint venture are an express or implied contract, which includes the following elements: (1) a community of interest in the performance of the common purpose; (2) joint control or right of control; (3) a joint proprietary interest in the subject matter; (4) ...