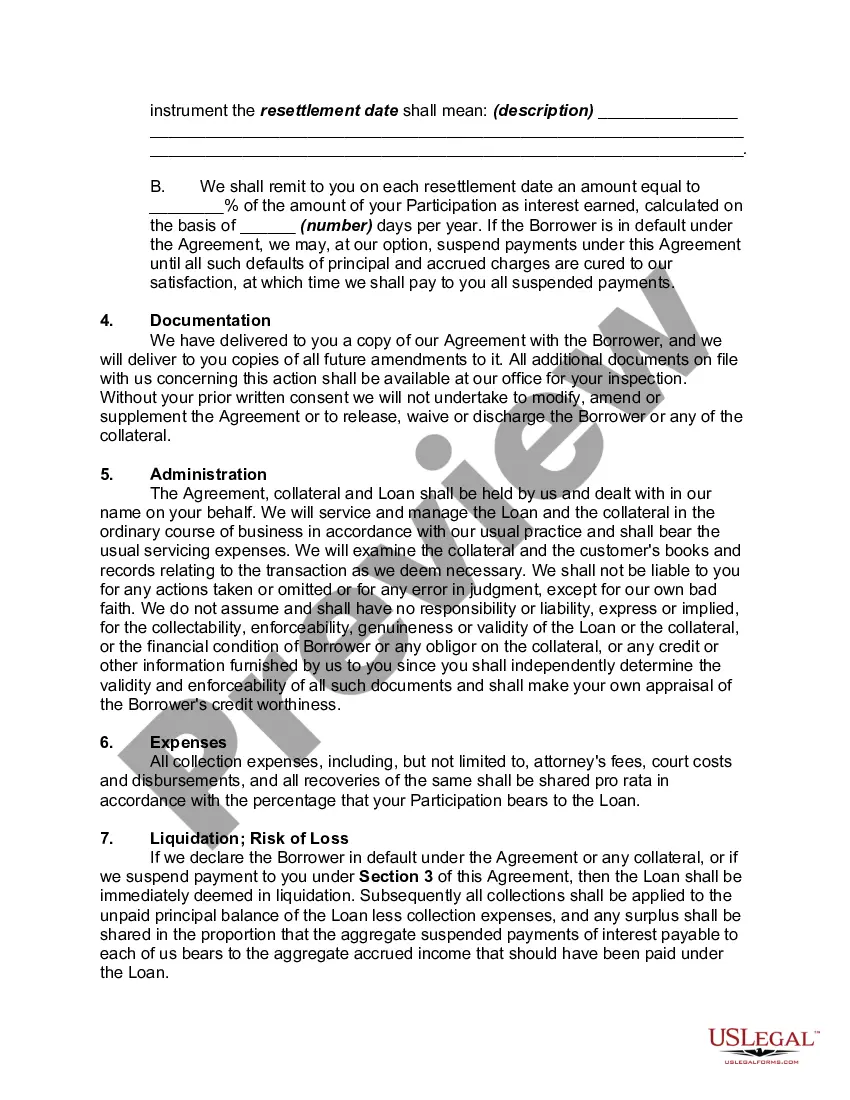

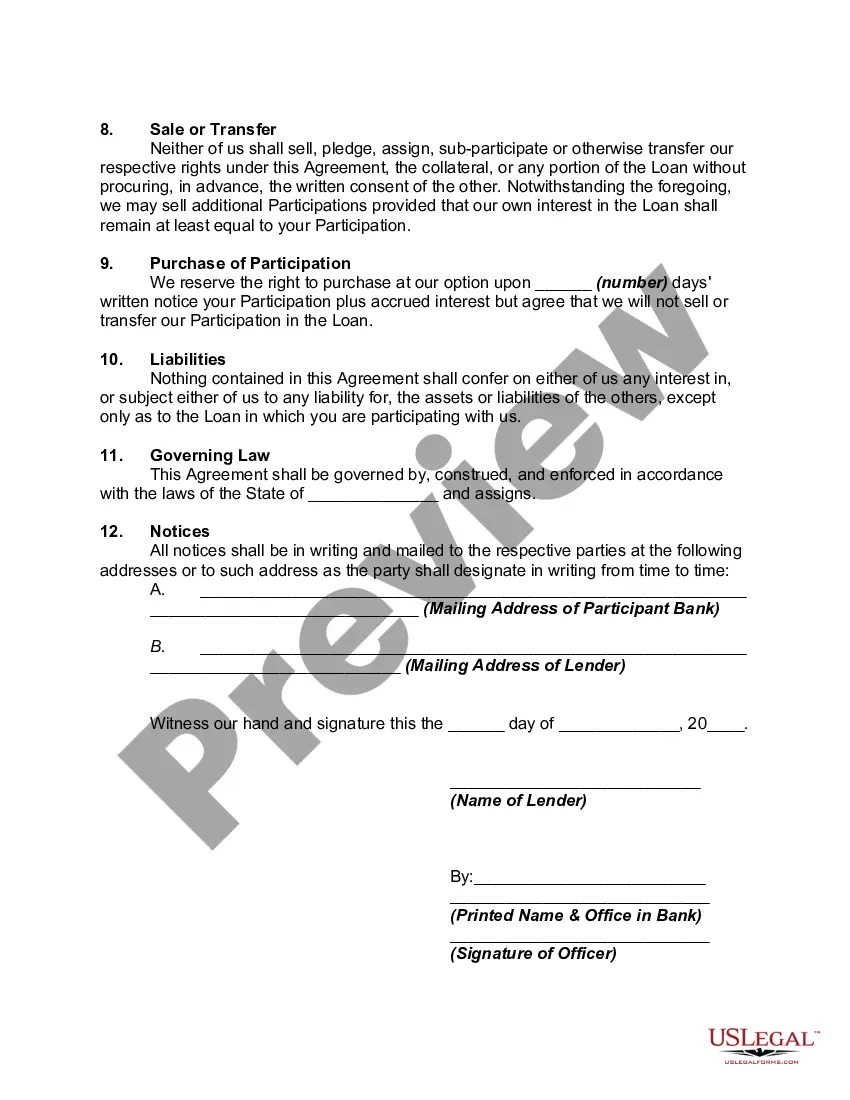

Participation loans are loans made by multiple lenders to a single borrower. Several banks, for example, might chip in to fund one extremely large loan, with one of the banks taking the role of the "lead bank." This lending institution then recruits other banks to participate and share the risks and profits. The lead bank typically originates the loan, takes responsibility for the loan servicing of the participation loan, organizes and manages the participation, and deals directly with the borrower.

Participations in the loan are sold by the lead bank to other banks. A separate contract called a loan participation agreement is structured and agreed among the banks. Loan participations can either be made with equal risk sharing for all loan participants, or on a senior/subordinated basis, where the senior lender is paid first and the subordinate loan participation paid only if there is sufficient funds left over to make the payments.

In Maryland, a Participating or Participation Loan Agreement is a legal contract that outlines the terms and conditions between multiple parties involved in a secured loan agreement. This agreement allows a lender, called a participant, to join the original lender in providing a loan to a borrower, and share in the risks and benefits associated with the loan. The Maryland Participating or Participation Loan Agreement is often used in situations where a borrower requires a substantial amount of financing that a single lender might not be willing or able to provide. By entering into this agreement, the original lender can share the loan with another lender, known as a participant, who is willing to share in the loan obligations. There are three main types of Maryland Participating or Participation Loan Agreements commonly used: 1. Doubly Secured Participating Loan Agreement: This type of agreement is typically used when the participant is granted a subordinate lien on the borrower's collateral, in addition to the lien already held by the original lender. In the event of default or foreclosure, the participant will have the right to claim a share of the collateral's proceeds after the original lender is repaid. 2. Non-Doubly Secured Participating Loan Agreement: Unlike the doubly secured agreement, this type does not grant the participant a subordinate lien on the borrower's collateral. Instead, the participant relies solely on the borrower's ability to repay the loan. In case of default, the participant will not have direct access to the collateral. 3. Mezzanine Participating Loan Agreement: This type of agreement is commonly used in real estate financing. It allows the participant to provide an additional layer of debt capital to the borrower, secured by a second mortgage on the property. In this arrangement, the participant's loan is subordinate to the original lender's loan, but it has priority over the borrower's equity. The Maryland Participating or Participation Loan Agreement is crucial in clearly defining the responsibilities and obligations of all parties involved. It covers crucial aspects such as the loan amount, interest rates, repayment terms, default provisions, and the allocation of risks and rewards between the original lender and the participant(s). This agreement helps protect the interests of all parties involved and ensures transparency in the lending process. It is essential for borrowers, lenders, and participants to carefully review and negotiate the terms of the Maryland Participating or Participation Loan Agreement before finalizing the loan transaction. Seeking legal advice and conducting due diligence are critical steps to ensure compliance with Maryland laws and regulations, as well as to safeguard the interests of all involved parties.In Maryland, a Participating or Participation Loan Agreement is a legal contract that outlines the terms and conditions between multiple parties involved in a secured loan agreement. This agreement allows a lender, called a participant, to join the original lender in providing a loan to a borrower, and share in the risks and benefits associated with the loan. The Maryland Participating or Participation Loan Agreement is often used in situations where a borrower requires a substantial amount of financing that a single lender might not be willing or able to provide. By entering into this agreement, the original lender can share the loan with another lender, known as a participant, who is willing to share in the loan obligations. There are three main types of Maryland Participating or Participation Loan Agreements commonly used: 1. Doubly Secured Participating Loan Agreement: This type of agreement is typically used when the participant is granted a subordinate lien on the borrower's collateral, in addition to the lien already held by the original lender. In the event of default or foreclosure, the participant will have the right to claim a share of the collateral's proceeds after the original lender is repaid. 2. Non-Doubly Secured Participating Loan Agreement: Unlike the doubly secured agreement, this type does not grant the participant a subordinate lien on the borrower's collateral. Instead, the participant relies solely on the borrower's ability to repay the loan. In case of default, the participant will not have direct access to the collateral. 3. Mezzanine Participating Loan Agreement: This type of agreement is commonly used in real estate financing. It allows the participant to provide an additional layer of debt capital to the borrower, secured by a second mortgage on the property. In this arrangement, the participant's loan is subordinate to the original lender's loan, but it has priority over the borrower's equity. The Maryland Participating or Participation Loan Agreement is crucial in clearly defining the responsibilities and obligations of all parties involved. It covers crucial aspects such as the loan amount, interest rates, repayment terms, default provisions, and the allocation of risks and rewards between the original lender and the participant(s). This agreement helps protect the interests of all parties involved and ensures transparency in the lending process. It is essential for borrowers, lenders, and participants to carefully review and negotiate the terms of the Maryland Participating or Participation Loan Agreement before finalizing the loan transaction. Seeking legal advice and conducting due diligence are critical steps to ensure compliance with Maryland laws and regulations, as well as to safeguard the interests of all involved parties.