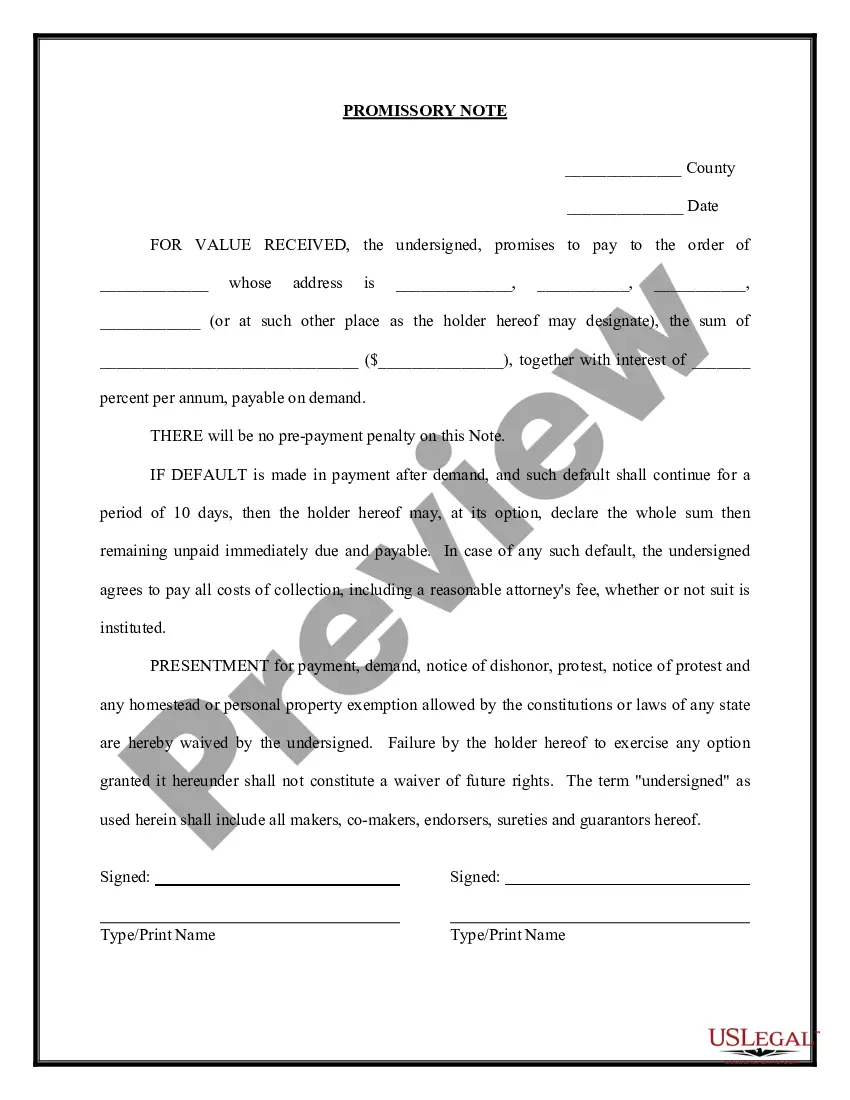

A Maryland Promissory Note — Payable on Demand is a legally binding document that outlines the terms and conditions of a loan agreement between a lender and a borrower. This type of promissory note is used when the lender requires repayment of the loan amount on demand, which means that the borrower must repay the loan as soon as the lender requests it. A Maryland Promissory Note — Payable on Demand contains essential information such as the names and contact information of both parties involved, the loan amount, the interest rate (if applicable), and the repayment terms. The repayment terms may include details about the repayment schedule, late payment penalties, and any additional fees or charges. It is important to note that there are different types of Maryland Promissory Notes — Payable on Demand that can be used depending on the specific circumstances of the loan agreement. These include: 1. Personal Promissory Note — Payable on Demand: This type of promissory note is used for loans between individuals, such as friends or family members. It provides a formal agreement to ensure both parties are protected and know the terms of the loan. 2. Business Promissory Note — Payable on Demand: This promissory note is used for loans between businesses. It ensures that the loan amount and repayment terms are clearly defined, reducing the risk of misunderstandings or disputes. 3. Secured Promissory Note — Payable on Demand: In some cases, the lender may require collateral to secure the loan. This type of promissory note details the collateral provided by the borrower and the consequences of defaulting on the loan. 4. Unsecured Promissory Note — Payable on Demand: This promissory note is used when the lender does not require any collateral. It is typically based on the borrower's creditworthiness and serves as a promise of repayment. When drafting a Maryland Promissory Note — Payable on Demand, it is essential to consult with a legal professional to ensure compliance with state laws and to tailor the document to meet the specific needs of the lender and borrower. This helps protect both parties and ensures a smooth loan transaction.

Maryland Promissory Note - Payable on Demand

Description

How to fill out Maryland Promissory Note - Payable On Demand?

US Legal Forms - one of many greatest libraries of legal types in the United States - offers a wide array of legal papers themes you may download or produce. Making use of the web site, you can find a huge number of types for enterprise and specific functions, categorized by classes, states, or search phrases.You can find the most recent types of types just like the Maryland Promissory Note - Payable on Demand in seconds.

If you already have a monthly subscription, log in and download Maryland Promissory Note - Payable on Demand through the US Legal Forms library. The Down load option will show up on each and every type you see. You have access to all in the past acquired types in the My Forms tab of your account.

In order to use US Legal Forms the first time, listed here are basic directions to obtain started:

- Be sure you have selected the correct type for your town/county. Select the Review option to examine the form`s content. Read the type explanation to actually have selected the correct type.

- If the type doesn`t satisfy your demands, utilize the Search field towards the top of the display screen to get the the one that does.

- Should you be satisfied with the shape, validate your option by simply clicking the Acquire now option. Then, opt for the costs prepare you prefer and offer your qualifications to register to have an account.

- Approach the deal. Utilize your bank card or PayPal account to perform the deal.

- Find the structure and download the shape on your own product.

- Make changes. Fill out, revise and produce and indication the acquired Maryland Promissory Note - Payable on Demand.

Every design you included with your bank account does not have an expiry time and is your own property permanently. So, if you wish to download or produce yet another version, just go to the My Forms area and click on the type you require.

Gain access to the Maryland Promissory Note - Payable on Demand with US Legal Forms, the most comprehensive library of legal papers themes. Use a huge number of specialist and express-specific themes that meet up with your business or specific needs and demands.