In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

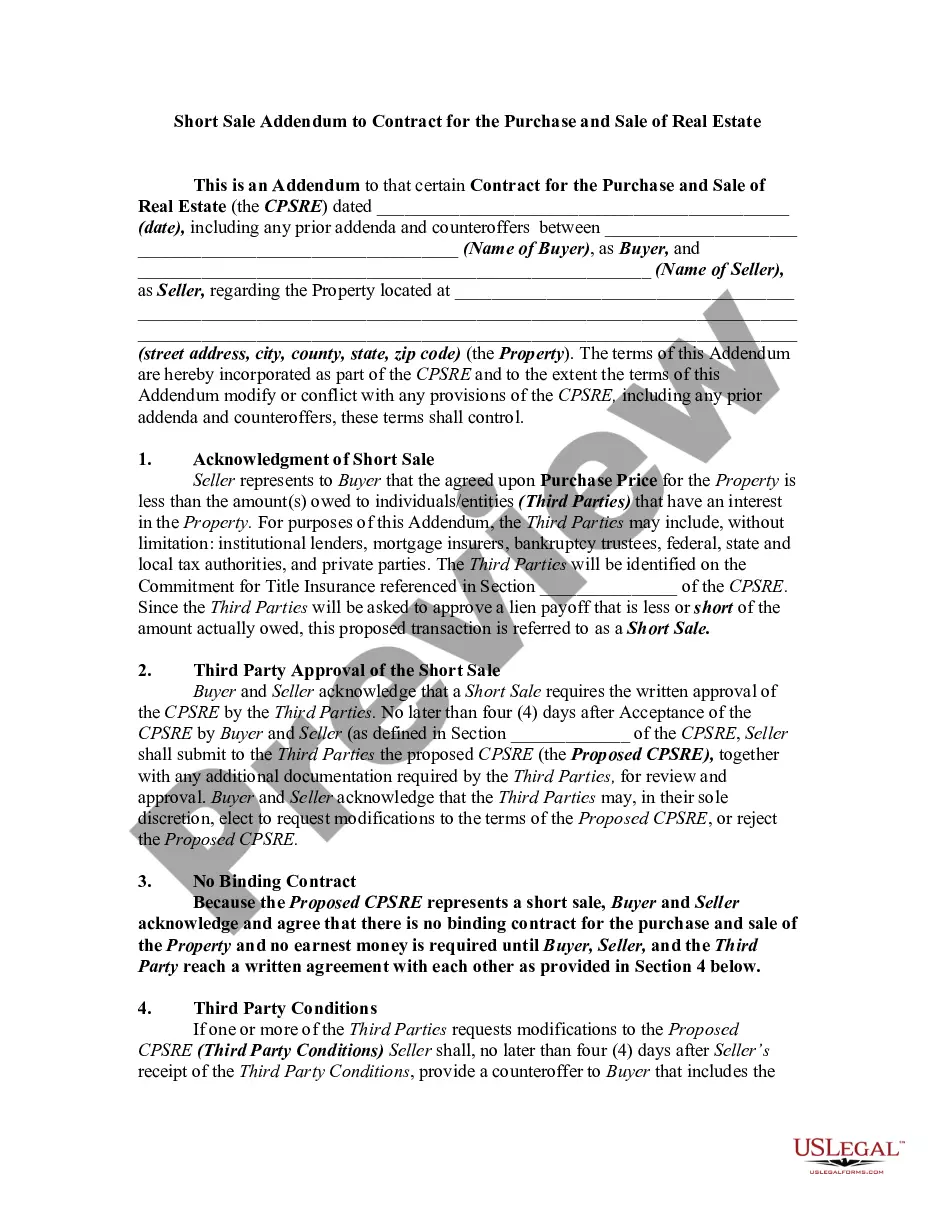

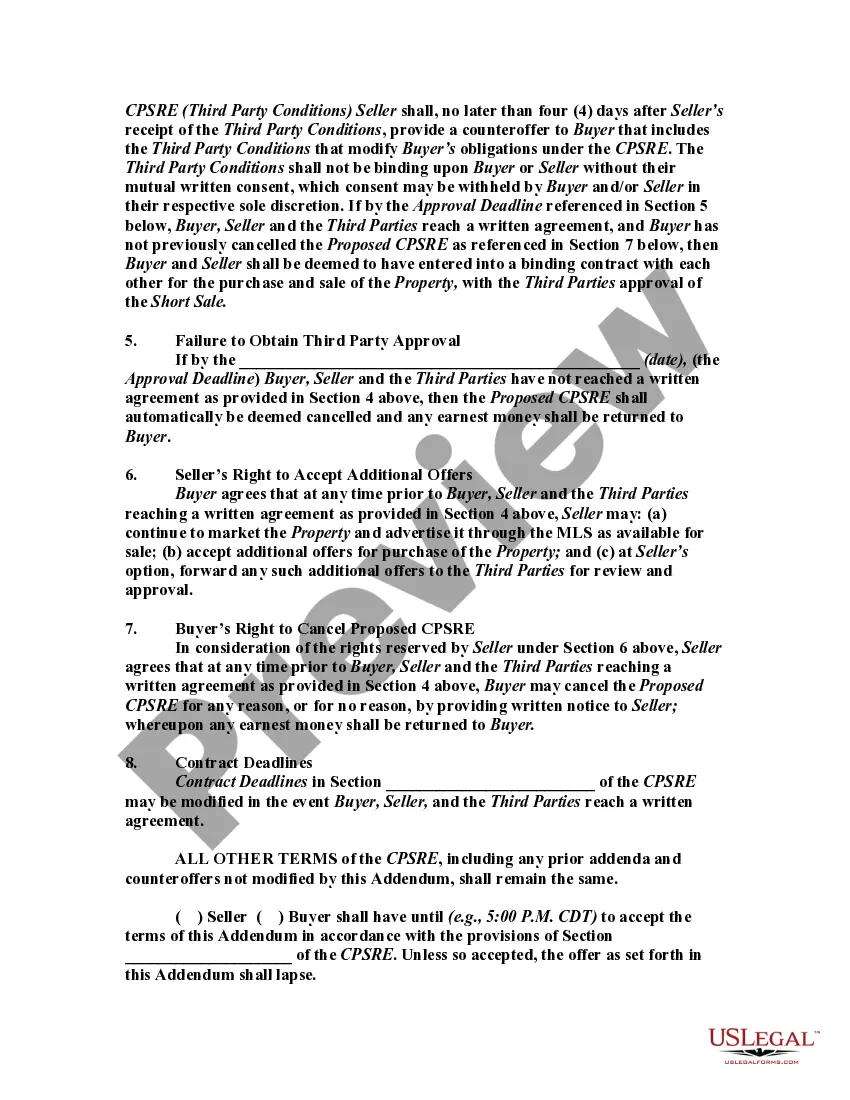

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Maryland Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a crucial document used in real estate transactions involving the sale of a property under short sale conditions in the state of Maryland. This addendum provides additional terms and conditions specific to short sales, which are a way for homeowners to sell their property at a price below the outstanding mortgage balance. The addendum outlines various key aspects that are unique to short sales, ensuring that both the buyer and seller are aware of these conditions. It is important to note that there may be different types or versions of the Maryland Short Sale Addendum, each tailored to specific circumstances or requirements. Some possible variations may include: 1. Maryland Short Sale Addendum for Residential Properties: Typically used when the property in question is a single-family home, condominium, or townhouse. 2. Maryland Short Sale Addendum for Commercial Properties: Designed specifically for short sale transactions involving commercial real estate properties, such as office buildings, retail spaces, or industrial facilities. 3. Maryland Short Sale Addendum for Investment Properties: This type of addendum is employed when the property being sold is an investment property, such as a rental property or multiplex, and not the seller's primary residence. The core elements covered in the Maryland Short Sale Addendum generally include: 1. Short Sale Approval Contingency: Specifies that the transaction is contingent upon the seller obtaining approval from their lender(s) for the short sale. It includes deadlines for obtaining this approval and the option for the buyer to terminate the contract if approval is not received within the stipulated timeframe. 2. Listing Agreement and Marketing: Addresses the obligations and responsibilities of both the seller and listing agent regarding marketing efforts and providing details about the property to potential buyers. 3. Third-Party Fees and Liens: Clarifies the allocation of costs related to short sales, such as unpaid property taxes, homeowner association fees, or any other outstanding liens on the property. 4. Property Condition and Inspections: Outlines the condition of the property and establishes the buyer's right to conduct inspections. It may address any potential remediation or repairs needed, and how these will be handled in the short sale process. 5. Seller Contributions and Financial Obligations: Details any financial obligations of the seller, including potential contributions toward closing costs or lender-required repairs. 6. Short Sale Negotiation and Communication: Outlines how the negotiation process with the seller's lender will occur and addresses confidentiality regarding sensitive financial information. It is essential to consult with a qualified real estate professional or legal counsel when dealing with short sales in Maryland to ensure compliance with local laws and regulations, as well as to obtain the appropriate and up-to-date version of the Maryland Short Sale Addendum relevant to the specific property type.The Maryland Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a crucial document used in real estate transactions involving the sale of a property under short sale conditions in the state of Maryland. This addendum provides additional terms and conditions specific to short sales, which are a way for homeowners to sell their property at a price below the outstanding mortgage balance. The addendum outlines various key aspects that are unique to short sales, ensuring that both the buyer and seller are aware of these conditions. It is important to note that there may be different types or versions of the Maryland Short Sale Addendum, each tailored to specific circumstances or requirements. Some possible variations may include: 1. Maryland Short Sale Addendum for Residential Properties: Typically used when the property in question is a single-family home, condominium, or townhouse. 2. Maryland Short Sale Addendum for Commercial Properties: Designed specifically for short sale transactions involving commercial real estate properties, such as office buildings, retail spaces, or industrial facilities. 3. Maryland Short Sale Addendum for Investment Properties: This type of addendum is employed when the property being sold is an investment property, such as a rental property or multiplex, and not the seller's primary residence. The core elements covered in the Maryland Short Sale Addendum generally include: 1. Short Sale Approval Contingency: Specifies that the transaction is contingent upon the seller obtaining approval from their lender(s) for the short sale. It includes deadlines for obtaining this approval and the option for the buyer to terminate the contract if approval is not received within the stipulated timeframe. 2. Listing Agreement and Marketing: Addresses the obligations and responsibilities of both the seller and listing agent regarding marketing efforts and providing details about the property to potential buyers. 3. Third-Party Fees and Liens: Clarifies the allocation of costs related to short sales, such as unpaid property taxes, homeowner association fees, or any other outstanding liens on the property. 4. Property Condition and Inspections: Outlines the condition of the property and establishes the buyer's right to conduct inspections. It may address any potential remediation or repairs needed, and how these will be handled in the short sale process. 5. Seller Contributions and Financial Obligations: Details any financial obligations of the seller, including potential contributions toward closing costs or lender-required repairs. 6. Short Sale Negotiation and Communication: Outlines how the negotiation process with the seller's lender will occur and addresses confidentiality regarding sensitive financial information. It is essential to consult with a qualified real estate professional or legal counsel when dealing with short sales in Maryland to ensure compliance with local laws and regulations, as well as to obtain the appropriate and up-to-date version of the Maryland Short Sale Addendum relevant to the specific property type.