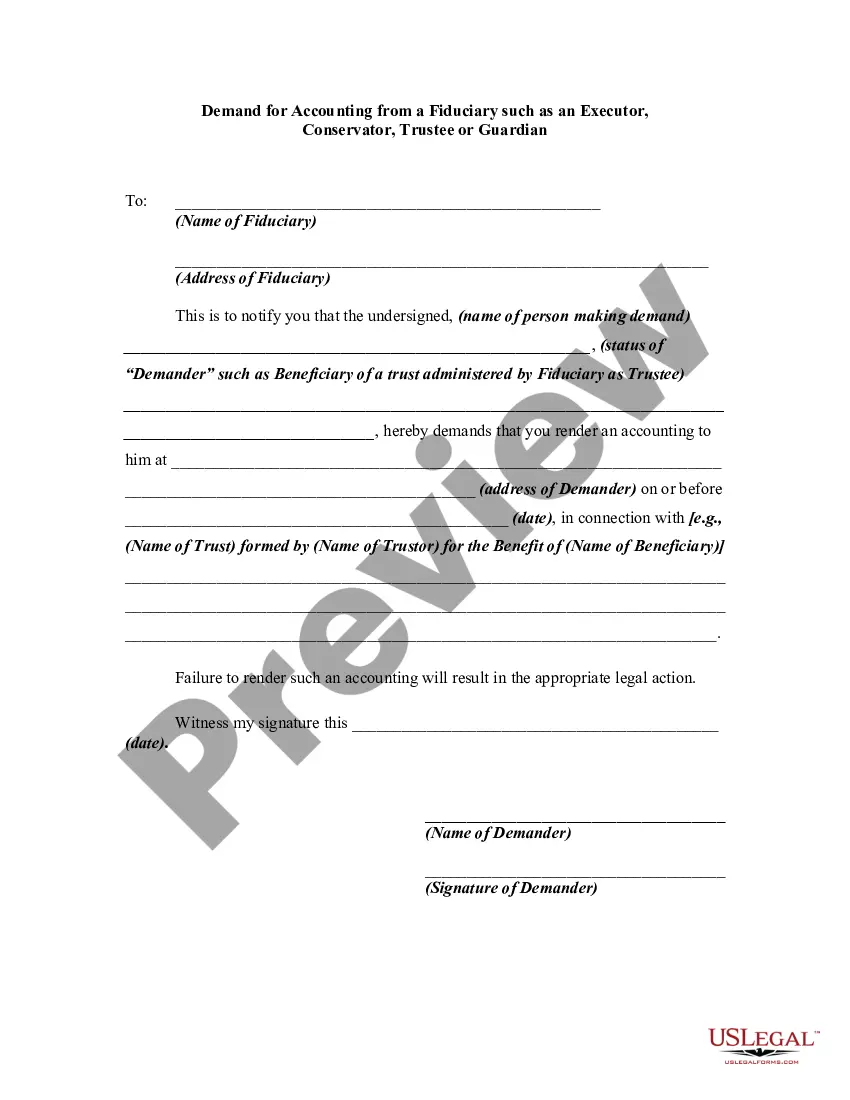

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

Maryland Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian is a legal process that allows beneficiaries, wards, or interested parties to request a detailed report of the financial activities conducted by a fiduciary. A fiduciary is an individual or entity entrusted with the management and protection of another person's assets or interests, and they have a legal obligation to act in the best interests of the beneficiary or ward. The demand for accounting serves as a mechanism to ensure transparency and accountability. It allows beneficiaries, wards, or interested parties to monitor and review the fiduciary's financial transactions, ensuring that they have been handled properly and in compliance with the applicable laws and regulations. This demand for accounting provides an opportunity to detect any financial irregularities, mismanagement, or breach of fiduciary duty. In Maryland, there are several types of demand for accounting that can be made depending on the specific fiduciary involved: 1. Executor Demand for Accounting: This pertains to the fiduciary responsible for administering the estate of a deceased person. Beneficiaries or interested parties can demand an accounting of the executor's actions, including the collection, management, and distribution of assets, payment of debts, and any related expenses. 2. Conservator Demand for Accounting: In cases where an individual has been deemed incapacitated and a conservator has been appointed to manage their financial affairs, interested parties can demand an accounting of the conservator's actions. This includes reviewing income, expenses, investments, and any other financial transactions made on behalf of the incapacitated person. 3. Trustee Demand for Accounting: Trustees are responsible for managing trusts, ensuring the fulfillment of its terms and the distribution of assets to the beneficiaries. Beneficiaries or interested parties can submit a demand for accounting to review the trustee's financial actions, including asset management, income distribution, expenses, and compliance with the trust document. 4. Legal Guardian Demand for Accounting: When a person is unable to handle their personal and financial affairs, a court may appoint a legal guardian. A demand for accounting can be made by interested parties to evaluate the financial transactions and decisions made by the legal guardian on behalf of the incapacitated person. Relevant keywords associated with Maryland Demand for Accounting from a Fiduciary include: Maryland fiduciary accounting, beneficiary rights in Maryland, fiduciary duty, demand for accounting process, legal guardianship, Maryland executor accounting, Maryland trustee accounting, Maryland conservator accounting, fiduciary responsibilities, fiduciary breach, Maryland estate administration, Maryland trust administration.