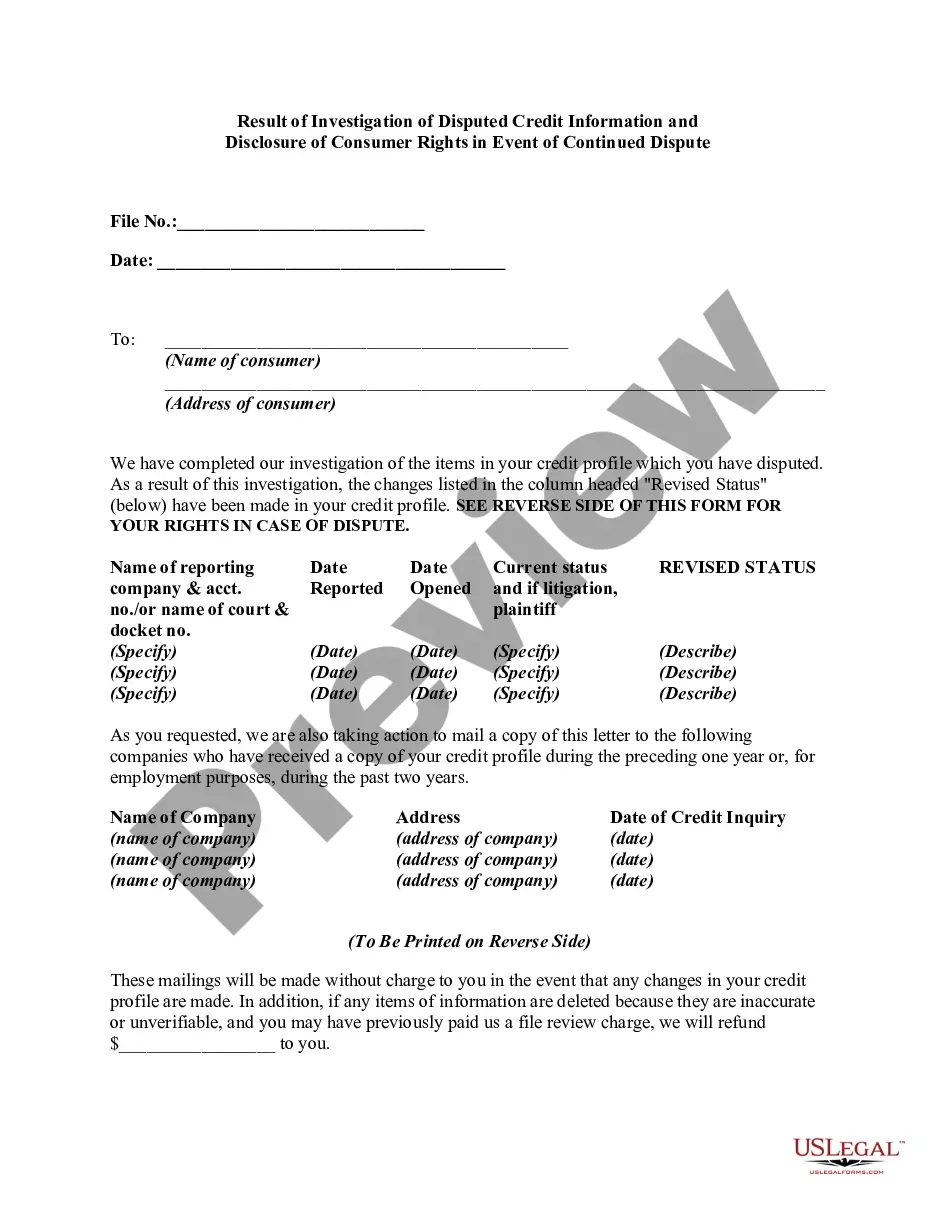

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

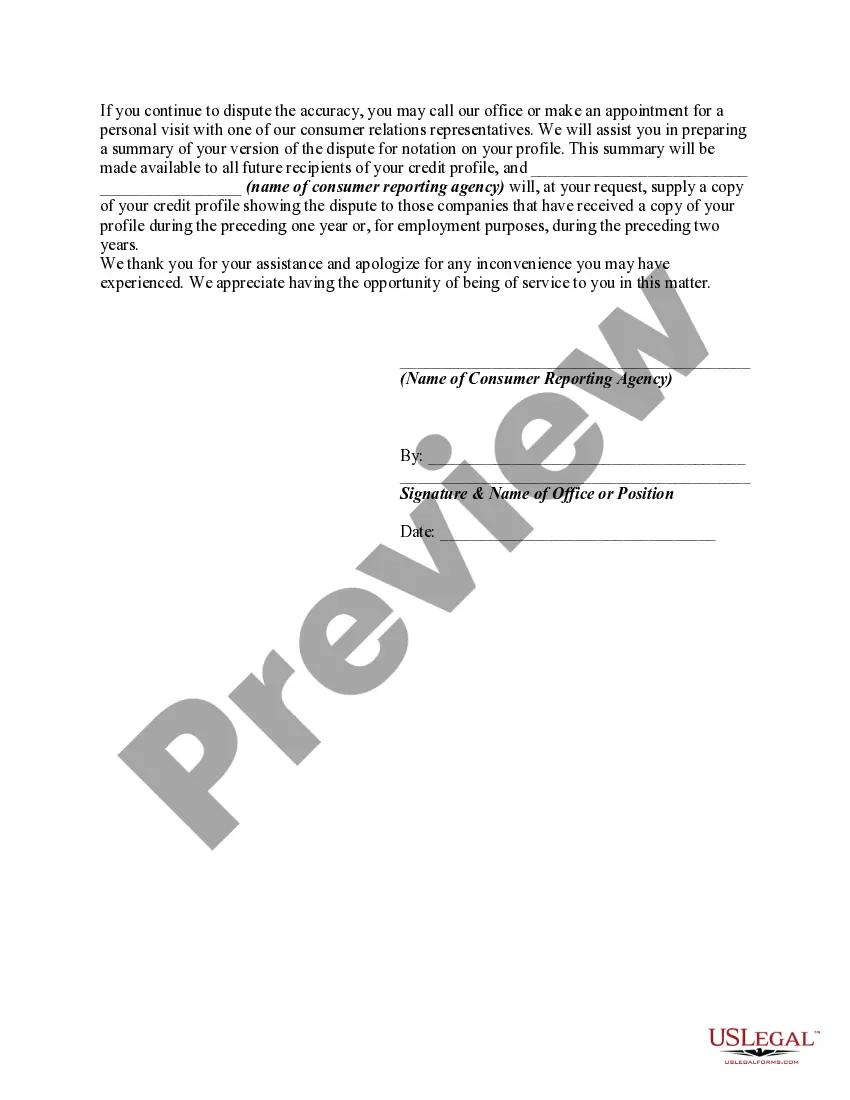

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Maryland's Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in the Event of Continued Dispute Keywords: Maryland, result of investigation, disputed credit information, disclosure, consumer rights, continued dispute Introduction: Maryland's laws and regulations empower consumers by providing them with certain rights regarding disputed credit information. This article aims to provide a detailed description of the investigation process and the outcomes that individuals may expect in Maryland. Additionally, it sheds light on the disclosure of consumer rights, enabling individuals to take informed action in case of a continued dispute. 1. Investigation Process for Disputed Credit Information in Maryland: When a consumer identifies an error or discrepancy on their credit report in Maryland, they have the right to dispute and request a thorough investigation. The process involves the following steps: 1.1 Submission of Dispute: The consumer initiates the investigation by submitting a dispute to the credit reporting agency (CRA) providing the erroneous information. 1.2 Investigation Period: The CRA undertakes an investigation within a specific timeframe (e.g., 30 days) to verify the accuracy of the disputed information. This may involve contacting the creditor or collection agency responsible for reporting the information. 1.3 Communication of Results: Once the investigation is complete, the consumer receives a written result from the CRA, providing details on the outcome of their dispute. This result includes: 1.3.1 Verified Information: If the disputed information is verified during the investigation, it will remain on the credit report as accurate. 1.3.2 Deleted Information: If the investigation finds the disputed information to be inaccurate or unverifiable, the CRA must delete it from the credit report. 1.3.3 Modified Information: In some cases, if the disputed information is found to be partially accurate or incomplete, the CRA must modify it to reflect the accurate details provided during the investigation. 2. Consumer Rights in the Event of a Continued Dispute: If the consumer remains dissatisfied with the results of the investigation or believes the issue persists, Maryland provides additional consumer rights: 2.1 Statement of Dispute: Consumers have the right to submit a 'Statement of Dispute' to the CRA, expressing their disagreement with the investigation's outcome. This statement will become a permanent part of their credit report. 2.2 Legal Recourse: If the consumer feels the CRA, creditor, or collection agency has mishandled the dispute process, violated federal or state laws, or failed to address inaccuracies, they may seek legal recourse. Consulting an attorney specializing in credit reporting or consumer protection can help determine the appropriate course of action. 2.3 Continuous Monitoring: Maintaining regular monitoring of credit reports allows consumers to identify any potential discrepancies or errors promptly. This practice helps in detecting further issues and facilitates taking immediate action. Conclusion: Maryland's investigation process for disputed credit information offers a comprehensive approach to resolving inaccuracies on credit reports. By understanding their consumer rights, individuals can actively participate in the dispute resolution process and take appropriate action if the dispute persists. Staying informed of these rights and regularly monitoring credit reports are crucial steps towards achieving accurate and fair credit information.Title: Maryland's Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in the Event of Continued Dispute Keywords: Maryland, result of investigation, disputed credit information, disclosure, consumer rights, continued dispute Introduction: Maryland's laws and regulations empower consumers by providing them with certain rights regarding disputed credit information. This article aims to provide a detailed description of the investigation process and the outcomes that individuals may expect in Maryland. Additionally, it sheds light on the disclosure of consumer rights, enabling individuals to take informed action in case of a continued dispute. 1. Investigation Process for Disputed Credit Information in Maryland: When a consumer identifies an error or discrepancy on their credit report in Maryland, they have the right to dispute and request a thorough investigation. The process involves the following steps: 1.1 Submission of Dispute: The consumer initiates the investigation by submitting a dispute to the credit reporting agency (CRA) providing the erroneous information. 1.2 Investigation Period: The CRA undertakes an investigation within a specific timeframe (e.g., 30 days) to verify the accuracy of the disputed information. This may involve contacting the creditor or collection agency responsible for reporting the information. 1.3 Communication of Results: Once the investigation is complete, the consumer receives a written result from the CRA, providing details on the outcome of their dispute. This result includes: 1.3.1 Verified Information: If the disputed information is verified during the investigation, it will remain on the credit report as accurate. 1.3.2 Deleted Information: If the investigation finds the disputed information to be inaccurate or unverifiable, the CRA must delete it from the credit report. 1.3.3 Modified Information: In some cases, if the disputed information is found to be partially accurate or incomplete, the CRA must modify it to reflect the accurate details provided during the investigation. 2. Consumer Rights in the Event of a Continued Dispute: If the consumer remains dissatisfied with the results of the investigation or believes the issue persists, Maryland provides additional consumer rights: 2.1 Statement of Dispute: Consumers have the right to submit a 'Statement of Dispute' to the CRA, expressing their disagreement with the investigation's outcome. This statement will become a permanent part of their credit report. 2.2 Legal Recourse: If the consumer feels the CRA, creditor, or collection agency has mishandled the dispute process, violated federal or state laws, or failed to address inaccuracies, they may seek legal recourse. Consulting an attorney specializing in credit reporting or consumer protection can help determine the appropriate course of action. 2.3 Continuous Monitoring: Maintaining regular monitoring of credit reports allows consumers to identify any potential discrepancies or errors promptly. This practice helps in detecting further issues and facilitates taking immediate action. Conclusion: Maryland's investigation process for disputed credit information offers a comprehensive approach to resolving inaccuracies on credit reports. By understanding their consumer rights, individuals can actively participate in the dispute resolution process and take appropriate action if the dispute persists. Staying informed of these rights and regularly monitoring credit reports are crucial steps towards achieving accurate and fair credit information.