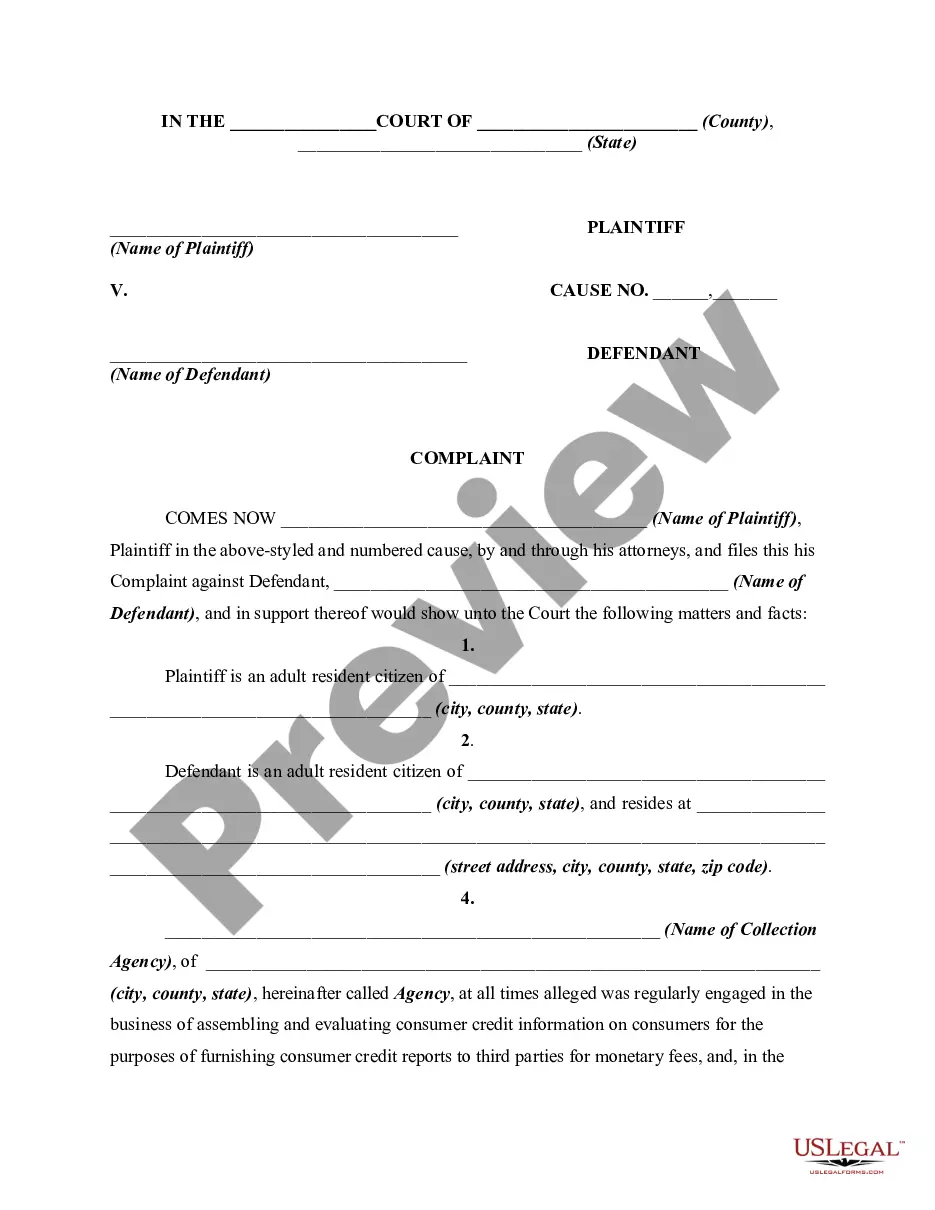

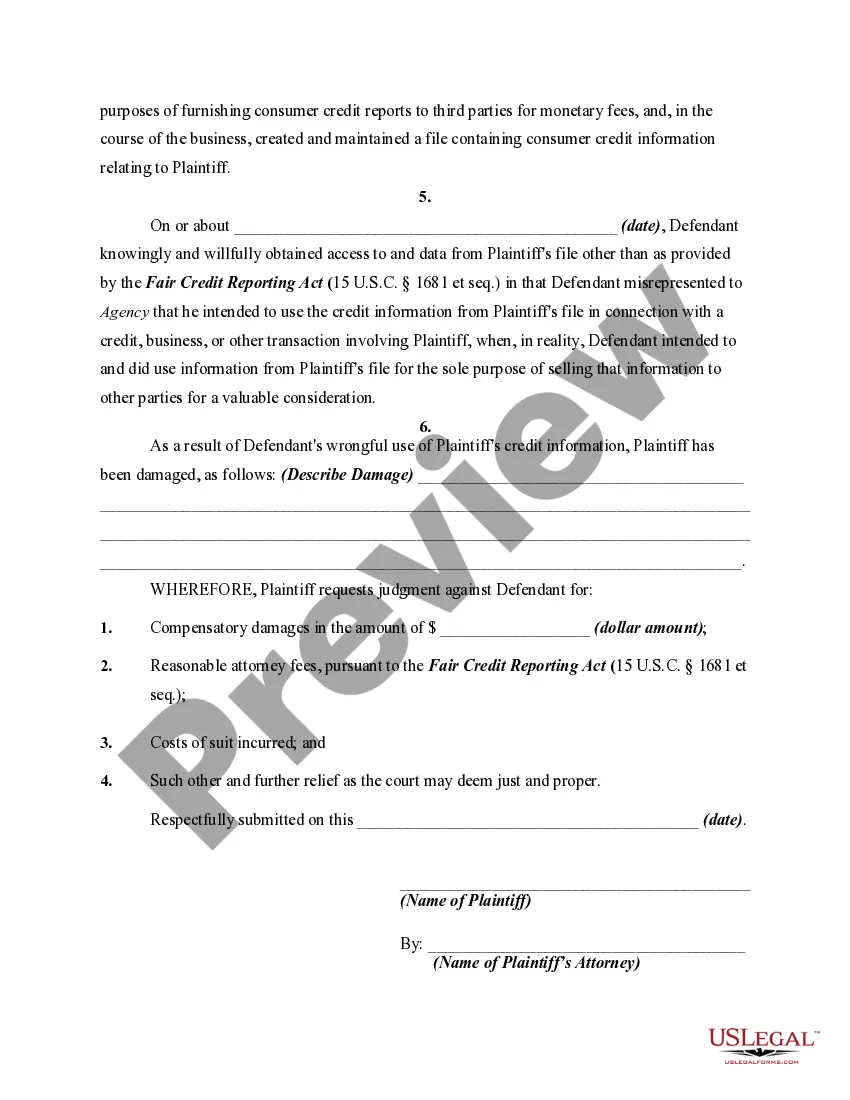

The Fair Credit Reporting Act regulates the use of information on a consumer's personal and financial condition. The most typical transaction which this Act would cover would be where a person applies for a personal loan or other consumer credit. Consumer credit is credit for personal, family, or household use, and not for business or commercial transactions. The purpose of the Act is to insure that consumer information obtained and used is done in such a way as to insure its confidentiality, accuracy, relevancy and proper utilization. Credit reporting bureaus are not permitted to disclose information to persons not having a legitimate use for this information. It is a federal crime to obtain or to furnish a credit report for an improper purpose.

Maryland Complaint by Consumer against Wrongful User of Credit Information can refer to various legal actions taken by individuals who believe that their credit information has been used improperly or without authorization. These complaints aim to protect consumers' rights and ensure fair practices in credit reporting. The following are potential types of complaints that fall under this category: 1. Identity Theft: This type of complaint arises when an individual discovers that their credit information has been used fraudulently by someone else without their knowledge or consent. It can involve unauthorized credit card transactions, loan applications, or other fraudulent activities using the victim's personal information. 2. Unauthorized Credit Inquiry: Consumers can file complaints when they suspect that a credit inquiry has been made on their credit report without a permissible purpose. This may include instances where a lender or any other party accesses a consumer's credit report without proper authorization or a legitimate reason. 3. Inaccurate Reporting: This type of complaint involves disputing inaccurate or false information on a credit report. Consumers may find incorrect account balances, late payments, or inaccurate personal details that negatively impact their creditworthiness. They can file complaints against the credit reporting agencies or the entities providing the incorrect information. 4. Failure to Update Information: Consumers can file complaints against credit reporting agencies or information furnishes if they fail to update their credit information, even after legitimate requests for corrections or updates have been made. This applies to situations where outdated or inaccurate information continues to affect a consumer's creditworthiness. 5. Violation of Fair Credit Reporting Act (FCRA): Consumers can file complaints when they believe that their rights under the FCRA, which regulates credit reporting practices, have been violated. This may include issues related to the disclosure of credit information, disputes, or the handling of credit reports without proper procedures. When filing a Maryland Complaint by Consumer against Wrongful User of Credit Information, individuals should consult legal professionals for guidance on the specific procedures and requirements involved. It is essential to gather relevant evidence, such as credit reports, account statements, correspondence, and any supporting documentation to substantiate the claim. The complaint should clearly explain the nature of the alleged wrongful use of credit information and the damages suffered as a result. By providing comprehensive information and using appropriate keywords, consumers can effectively address their concerns and seek the resolution they deserve.Maryland Complaint by Consumer against Wrongful User of Credit Information can refer to various legal actions taken by individuals who believe that their credit information has been used improperly or without authorization. These complaints aim to protect consumers' rights and ensure fair practices in credit reporting. The following are potential types of complaints that fall under this category: 1. Identity Theft: This type of complaint arises when an individual discovers that their credit information has been used fraudulently by someone else without their knowledge or consent. It can involve unauthorized credit card transactions, loan applications, or other fraudulent activities using the victim's personal information. 2. Unauthorized Credit Inquiry: Consumers can file complaints when they suspect that a credit inquiry has been made on their credit report without a permissible purpose. This may include instances where a lender or any other party accesses a consumer's credit report without proper authorization or a legitimate reason. 3. Inaccurate Reporting: This type of complaint involves disputing inaccurate or false information on a credit report. Consumers may find incorrect account balances, late payments, or inaccurate personal details that negatively impact their creditworthiness. They can file complaints against the credit reporting agencies or the entities providing the incorrect information. 4. Failure to Update Information: Consumers can file complaints against credit reporting agencies or information furnishes if they fail to update their credit information, even after legitimate requests for corrections or updates have been made. This applies to situations where outdated or inaccurate information continues to affect a consumer's creditworthiness. 5. Violation of Fair Credit Reporting Act (FCRA): Consumers can file complaints when they believe that their rights under the FCRA, which regulates credit reporting practices, have been violated. This may include issues related to the disclosure of credit information, disputes, or the handling of credit reports without proper procedures. When filing a Maryland Complaint by Consumer against Wrongful User of Credit Information, individuals should consult legal professionals for guidance on the specific procedures and requirements involved. It is essential to gather relevant evidence, such as credit reports, account statements, correspondence, and any supporting documentation to substantiate the claim. The complaint should clearly explain the nature of the alleged wrongful use of credit information and the damages suffered as a result. By providing comprehensive information and using appropriate keywords, consumers can effectively address their concerns and seek the resolution they deserve.