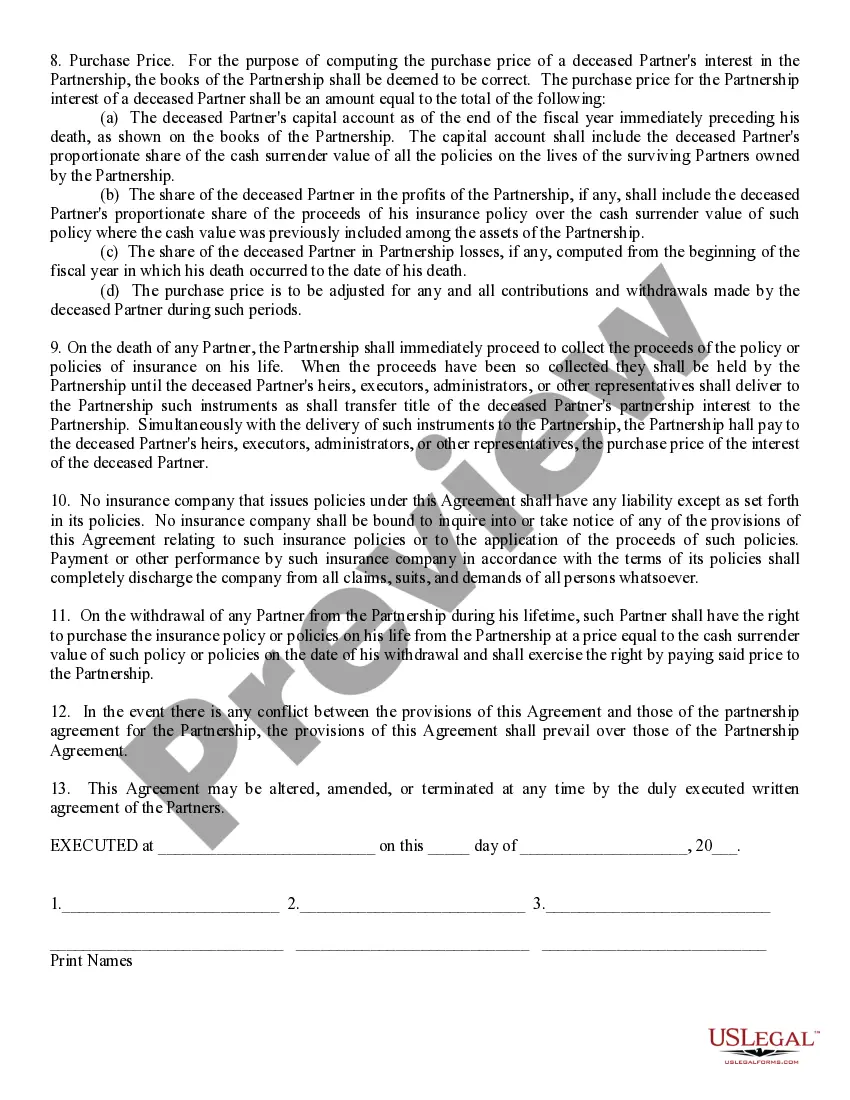

Maryland Sale of Deceased Partner's Interest refers to the legal process of disposing of a deceased partner's share in a business or partnership located in the state of Maryland. This process typically involves selling or transferring the interests, rights, and responsibilities of the deceased partner to another individual or entity. In Maryland, there are different types of Sale of Deceased Partner's Interest, which may include: 1. Private Sale: This involves the sale of the deceased partner's interest to an existing partner or a third-party buyer. Private sales often require negotiations on the value of the deceased partner's interest and may require approval from other partners or the partnership agreement. 2. Public Auction: In certain situations, a public auction can be held to sell the deceased partner's interest. This type of sale allows interested buyers to bid on the interest openly, ensuring transparency and potentially maximizing the value of the interest. 3. Redemption by Partnership: In some cases, the partnership may have the option to redeem the deceased partner's interest. This means that the remaining partners can choose to purchase the interest themselves, ensuring it remains within the partnership. 4. Purchase by Heir or Beneficiary: If the deceased partner had specified an heir or beneficiary in their will or trust, the heir or beneficiary may have the option to purchase the interest. This allows them to become a partner in the business or partnership or receive the value associated with that interest. The process of the Maryland Sale of Deceased Partner's Interest typically involves various legal steps, such as obtaining necessary court approvals, valuing the interest, and executing the sale agreement. It is important to consult with an attorney experienced in business law and estate planning to ensure compliance with state laws and to protect the interests of all parties involved. Keywords: Maryland Sale of Deceased Partner's Interest, business, partnership, deceased partner, legal process, transfer, private sale, public auction, redemption, heir, beneficiary, court approval, value, sale agreement, business law, estate planning.

Maryland Sale of Deceased Partner's Interest

Description

How to fill out Maryland Sale Of Deceased Partner's Interest?

If you wish to obtain, download, or print legal document templates, utilize US Legal Forms, the most extensive collection of legal forms available online.

Employ the site's straightforward and user-friendly search to locate the documents you require.

A variety of templates for business and personal purposes are organized by categories and states, or keywords.

Step 4. Once you have found the form you need, select the Buy now button. Choose the pricing plan you prefer and enter your information to register for the account.

Step 5. Complete the transaction. You can use your Visa or MasterCard or PayPal account to finalize the transaction.

- Utilize US Legal Forms to find the Maryland Sale of Deceased Partner's Interest with a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Acquire button to get the Maryland Sale of Deceased Partner's Interest.

- You can also access forms you have previously downloaded within the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions outlined below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Review feature to examine the form’s content. Be sure to read the summary.

- Step 3. If you are dissatisfied with the form, utilize the Search field at the top of the screen to find alternative versions of the legal form template.

Form popularity

FAQ

Remember, credit does not die and continues after the death of the debtor, meaning that creditors have a right to claim from the deceased's estate. Remember, the executor is obliged to pay all the estate's debts before distributing anything to their heirs or legatees of the deceased.

Creditors have six months from the date of death to submit a claim. Once the assets have been distributed, probate must remain open for at least six months to allow for a creditor to come forward.

Property passing to a child or other lineal descendant, spouse of a child or other lineal descendant, spouse, parent, grandparent, stepchild or stepparent, siblings or a corporation having only certain of these persons as stockholders is exempt from taxation. 10% on property passing to other individuals.

Inheritances are not considered income for federal tax purposes, whether you inherit cash, investments or property. However, any subsequent earnings on the inherited assets are taxable, unless it comes from a tax-free source.

How long do you have to make a claim? The Act has a strict time limit for making a claim of six months from the date of the Grant of Probate or Letters of Administration. In very exceptional circumstances this may be extended to allow a late claim, but as a rule you must stick to the six month deadline.

Collateral Inheritance Tax at the rate of 10% applies to distributions to persons or organizations not identified as exempt.

In Maryland, the statute of limitations on debt collection is three years. This means creditors have up to three years to file a lawsuit against you for the debt you supposedly owe.

Any Interest in an Annuity or other Public or Private Employee Pension or Benefit Plan. Any held Life Estates/Terms of Years. Payable-On-Death or Transfer-On-Death accounts. Real or Leasehold property owned by the decedent and located outside of Maryland.

Maryland is one of a few states with an inheritance tax. The tax focuses on the privilege of receiving property from a decedent. The Maryland inheritance tax rate is 10% of the value of the gift. It is currently only imposed on collateral heirs like a niece, nephew or friend.

In any event, where it is accepted that payment is due, the executor can seek to pay you (the creditor) from the deceased's estate. There is normally a six-month period from the deceased's death for creditors to advise the executor of any sums due to them from the estate.

Interesting Questions

More info

Search Tools > Search Tools > Browse By: Name Title ISBN Author Pages (in) Pages (out) ISBN Subject Catalog Keyword or Category Business Information Business Infrastructure Business Industry Business Service Interconnections Connections Transmission Design Services Technology Services Interconnections Transmission Technology Suppliers Communications Information Interconnections Transmission Supplier Marketing Sales Interconnect Communications Marketing Sales Communications Information Media Services Infrastructure Marketing Sales InterConnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Dependent Interconnectivity Competitors Information Business Infrastructure Business Industry Business Service