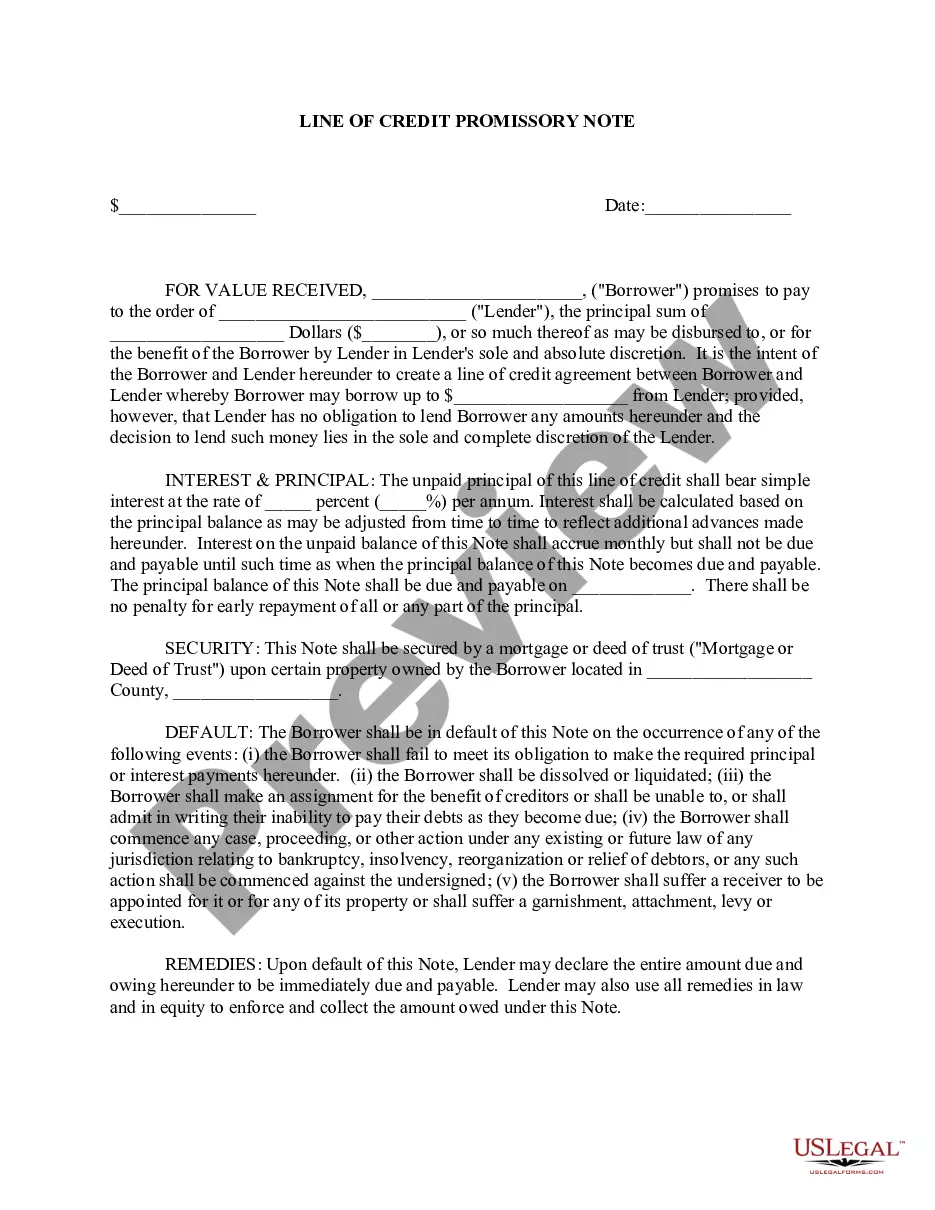

Maryland Line of Credit Promissory Note: A Comprehensive Overview Introduction: A Maryland Line of Credit Promissory Note refers to a legal document that outlines the terms and conditions for borrowing money through a line of credit in the state of Maryland. This note serves as a legally binding agreement between the borrower and the lender, ensuring that both parties are aware of their rights and obligations. By understanding the intricacies of this document, borrowers can make informed decisions while utilizing a line of credit in Maryland. Key Elements: 1. Borrower and Lender Information: — The Promissory Note includes the names, addresses, and contact details of both the borrower and the lender. It ensures clarity between the parties involved. 2. Loan Amount and Interest Rate: — This note specifies the maximum amount of money the borrower can access through the line of credit and sets the interest rate that will be charged on the borrowed amount. 3. Repayment Terms: — The Maryland Line of Credit Promissory Note indicates the repayment terms, including the repayment period, installment amounts, frequency of payments, and any additional fees or penalties associated with late payments. 4. Default and Remedies: — In the event of default, the note outlines the consequences, such as late fees and potential legal action, which the lender can take to recover the unpaid amount. Understanding the consequences of default is crucial for the borrower. 5. Security/Collateral: — If the line of credit is backed by collateral, such as property or assets, the Promissory Note specifies the type of security provided by the borrower to guarantee repayment. 6. Signatures and Witnesses: — To ensure the legal enforceability of the Maryland Line of Credit Promissory Note, it must be signed by both the borrower and lender. Witnesses may also be required, depending on Maryland state laws and lending institution policies. Types of Maryland Line of Credit Promissory Notes: 1. Personal Line of Credit: — This type of Promissory Note is utilized by individuals seeking a line of credit for personal financial needs, such as emergencies, education, or home improvements. 2. Business Line of Credit: — A business line of credit Promissory Note caters to entrepreneurs, small businesses, and corporations requiring funds to finance operations, manage cash flow, or cover unexpected expenses. 3. Home Equity Line of Credit (HELOT): — Specifically designed for homeowners, a HELOT Promissory Note allows individuals to borrow against the equity in their residential property for various purposes, such as renovations or debt consolidation. Conclusion: By acquainting yourself with the Maryland Line of Credit Promissory Note, you can make informed decisions about borrowing funds through a line of credit. Understanding the essential components, repayment terms, and consequences of default will enable borrowers to navigate these financial agreements with confidence. Whether it's a personal line of credit, business line of credit, or a HELOT, being well-informed ensures a smooth borrowing experience.

Maryland Line of Credit Promissory Note

Description

How to fill out Maryland Line Of Credit Promissory Note?

Discovering the right authorized papers web template could be a struggle. Naturally, there are plenty of templates available on the Internet, but how do you find the authorized develop you need? Utilize the US Legal Forms web site. The service delivers 1000s of templates, such as the Maryland Line of Credit Promissory Note, that can be used for company and private requirements. Each of the kinds are checked by professionals and meet federal and state needs.

When you are previously authorized, log in to the profile and then click the Obtain key to find the Maryland Line of Credit Promissory Note. Use your profile to look throughout the authorized kinds you might have bought earlier. Visit the My Forms tab of your respective profile and have one more version of your papers you need.

When you are a new user of US Legal Forms, listed here are easy instructions that you should comply with:

- Initially, ensure you have selected the proper develop for your area/region. You may look over the shape while using Review key and browse the shape explanation to make sure it is the best for you.

- When the develop does not meet your expectations, take advantage of the Seach area to obtain the appropriate develop.

- Once you are sure that the shape would work, go through the Get now key to find the develop.

- Opt for the prices prepare you would like and enter in the necessary information. Make your profile and pay for the order utilizing your PayPal profile or charge card.

- Opt for the data file formatting and obtain the authorized papers web template to the device.

- Full, edit and print and indicator the attained Maryland Line of Credit Promissory Note.

US Legal Forms may be the biggest catalogue of authorized kinds in which you can find various papers templates. Utilize the service to obtain expertly-created files that comply with status needs.