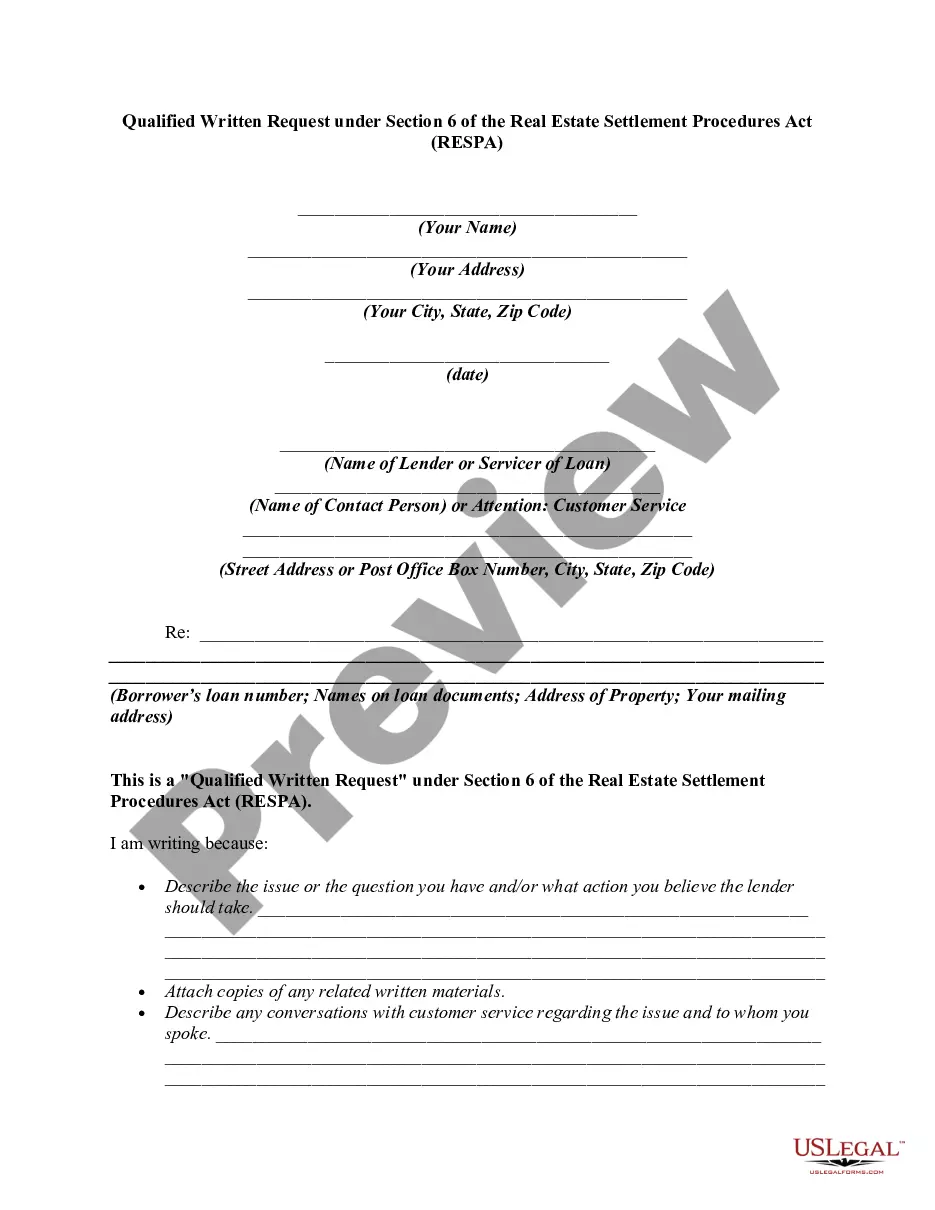

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

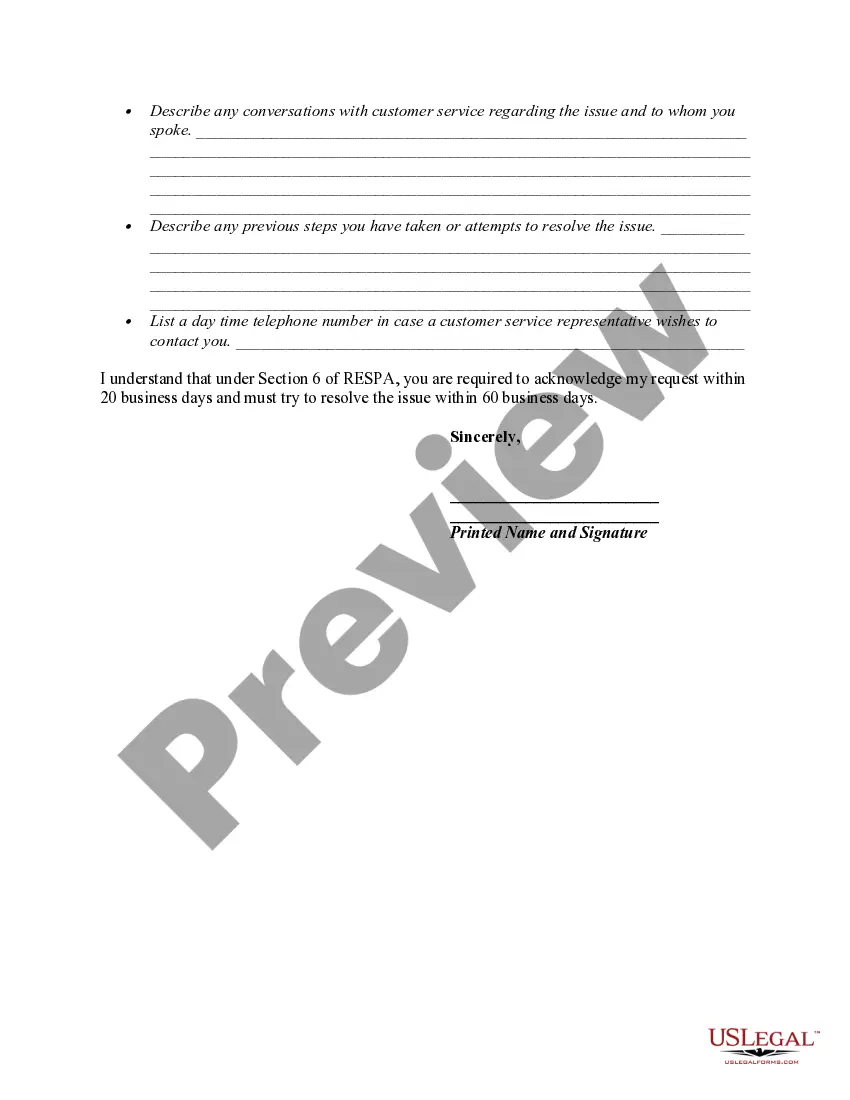

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

Maryland Qualified Written Request under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a formal process through which homeowners or borrowers in Maryland can request specific information from their mortgage service related to their loan or account. This request is governed by the provisions outlined in Section 6 of RESP. A Maryland Qualified Written Request (BWR) is a powerful tool that allows borrowers to obtain important information regarding their mortgages, such as loan documents, account statements, and payment history. It also provides a means for borrowers to challenge any errors, discrepancies, or unfair practices by the mortgage service. Some key elements of a Maryland Qualified Written Request under Section 6 of RESP may include: 1. Borrower Information: The request should include the borrower's full name, address, and contact details to ensure the mortgage service can identify the account accurately. 2. Loan Information: Details about the mortgage loan, such as the loan number, origination date, and loan balance, should be provided to assist the mortgage service in locating the relevant account. 3. Specific Information Requested: The borrower should be clear and detailed in outlining the specific information or documents they are requesting from the mortgage service. This can include loan agreements, escrow statements, or any other relevant documentation related to the loan. 4. Basis for the Request: The borrower should explain the reason behind the request, whether it is investigating an error, disputing charges, or seeking resolution for any concerns or discrepancies. 5. Documentation of Effort Made: The borrower should document any previous attempts made to resolve the issue with the mortgage service, such as previous phone calls, emails, or letters. This documentation demonstrates that there has been an effort to resolve the matter before escalating to a Qualified Written Request. 6. Timelines: The request should specify a reasonable timeframe for the mortgage service to respond to the request and provide the requested information. A typical timeframe is 20 business days. 7. Request for Response in Writing: The borrower should specifically request a written response from the mortgage service, ensuring that all communication is properly documented. It is important to note that there are no different types of Maryland Qualified Written Requests under Section 6 of RESP. However, the content and specific details within the request may vary based on the borrower's unique situation and the information they are seeking. Submitting a Maryland Qualified Written Request under Section 6 of RESP is an essential step for borrowers who are facing mortgage-related issues or have concerns regarding their loan. It empowers borrowers to access the necessary information and safeguards their rights under RESP.

Maryland Qualified Written Request under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a formal process through which homeowners or borrowers in Maryland can request specific information from their mortgage service related to their loan or account. This request is governed by the provisions outlined in Section 6 of RESP. A Maryland Qualified Written Request (BWR) is a powerful tool that allows borrowers to obtain important information regarding their mortgages, such as loan documents, account statements, and payment history. It also provides a means for borrowers to challenge any errors, discrepancies, or unfair practices by the mortgage service. Some key elements of a Maryland Qualified Written Request under Section 6 of RESP may include: 1. Borrower Information: The request should include the borrower's full name, address, and contact details to ensure the mortgage service can identify the account accurately. 2. Loan Information: Details about the mortgage loan, such as the loan number, origination date, and loan balance, should be provided to assist the mortgage service in locating the relevant account. 3. Specific Information Requested: The borrower should be clear and detailed in outlining the specific information or documents they are requesting from the mortgage service. This can include loan agreements, escrow statements, or any other relevant documentation related to the loan. 4. Basis for the Request: The borrower should explain the reason behind the request, whether it is investigating an error, disputing charges, or seeking resolution for any concerns or discrepancies. 5. Documentation of Effort Made: The borrower should document any previous attempts made to resolve the issue with the mortgage service, such as previous phone calls, emails, or letters. This documentation demonstrates that there has been an effort to resolve the matter before escalating to a Qualified Written Request. 6. Timelines: The request should specify a reasonable timeframe for the mortgage service to respond to the request and provide the requested information. A typical timeframe is 20 business days. 7. Request for Response in Writing: The borrower should specifically request a written response from the mortgage service, ensuring that all communication is properly documented. It is important to note that there are no different types of Maryland Qualified Written Requests under Section 6 of RESP. However, the content and specific details within the request may vary based on the borrower's unique situation and the information they are seeking. Submitting a Maryland Qualified Written Request under Section 6 of RESP is an essential step for borrowers who are facing mortgage-related issues or have concerns regarding their loan. It empowers borrowers to access the necessary information and safeguards their rights under RESP.