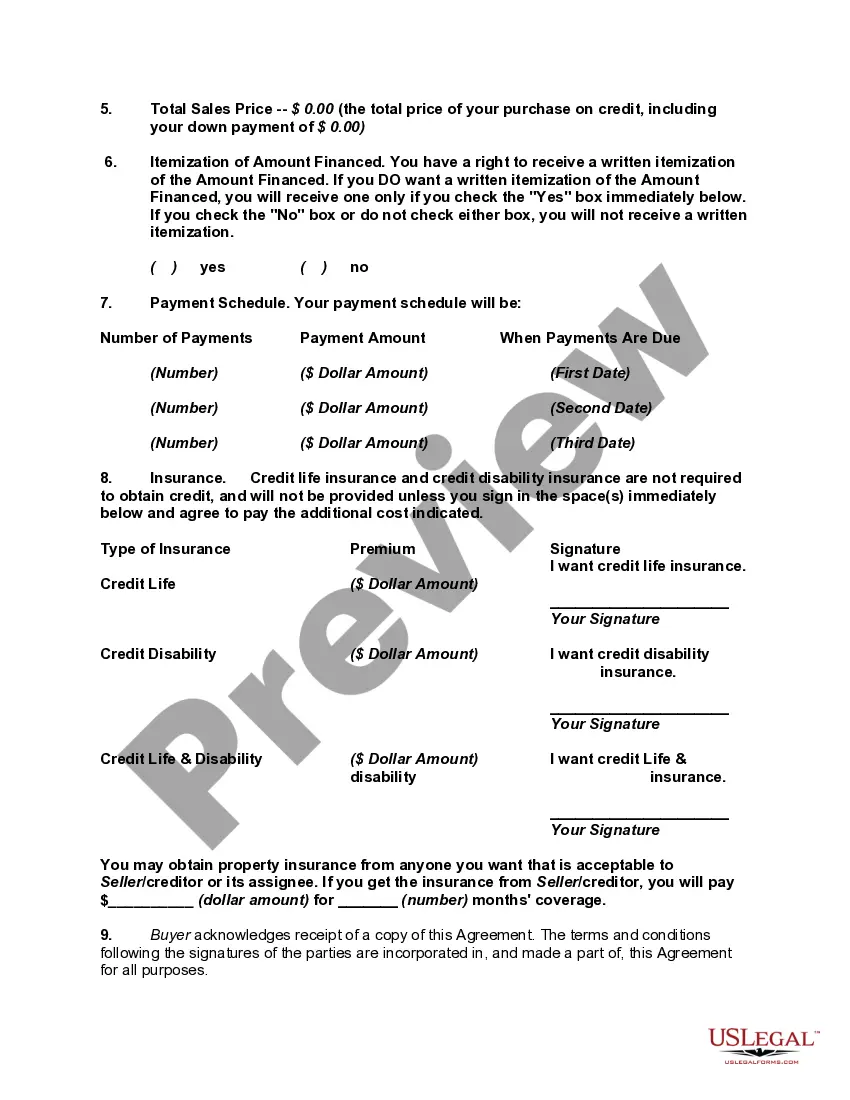

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

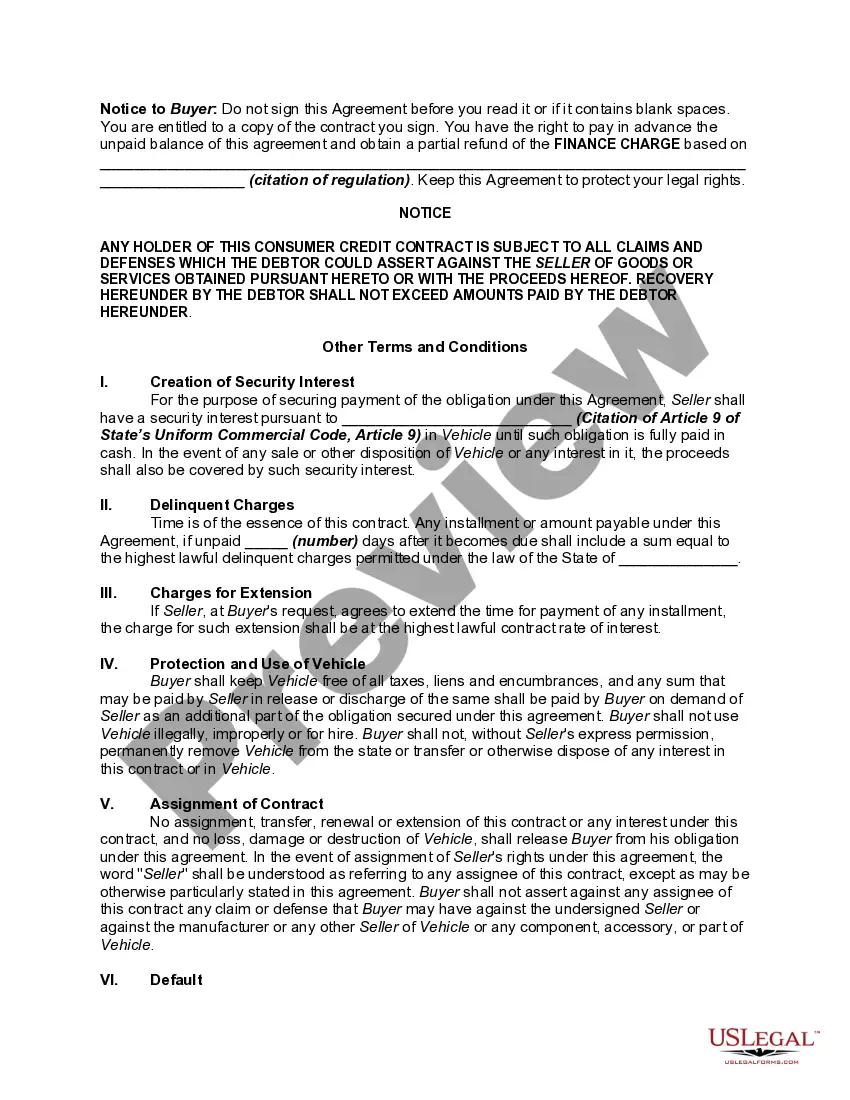

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

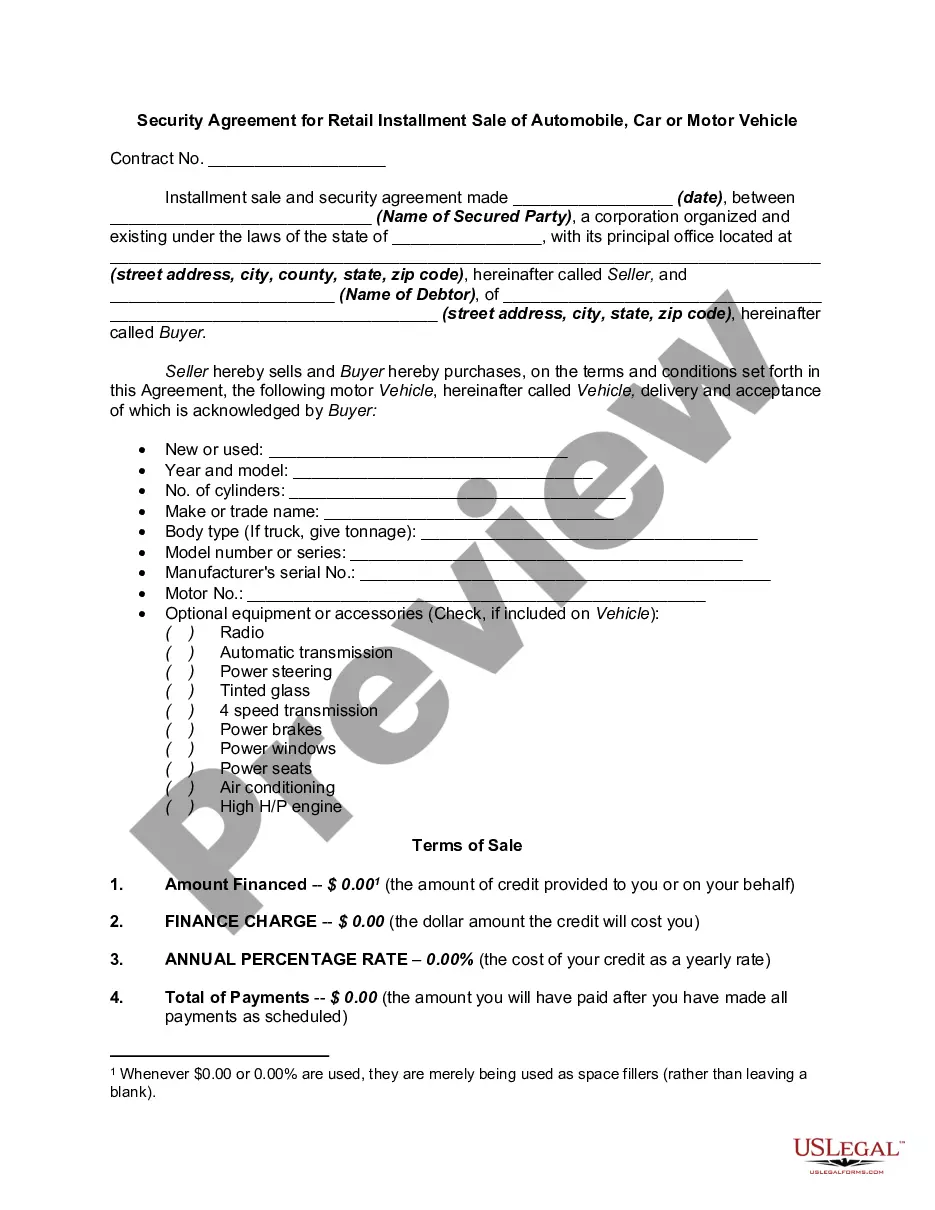

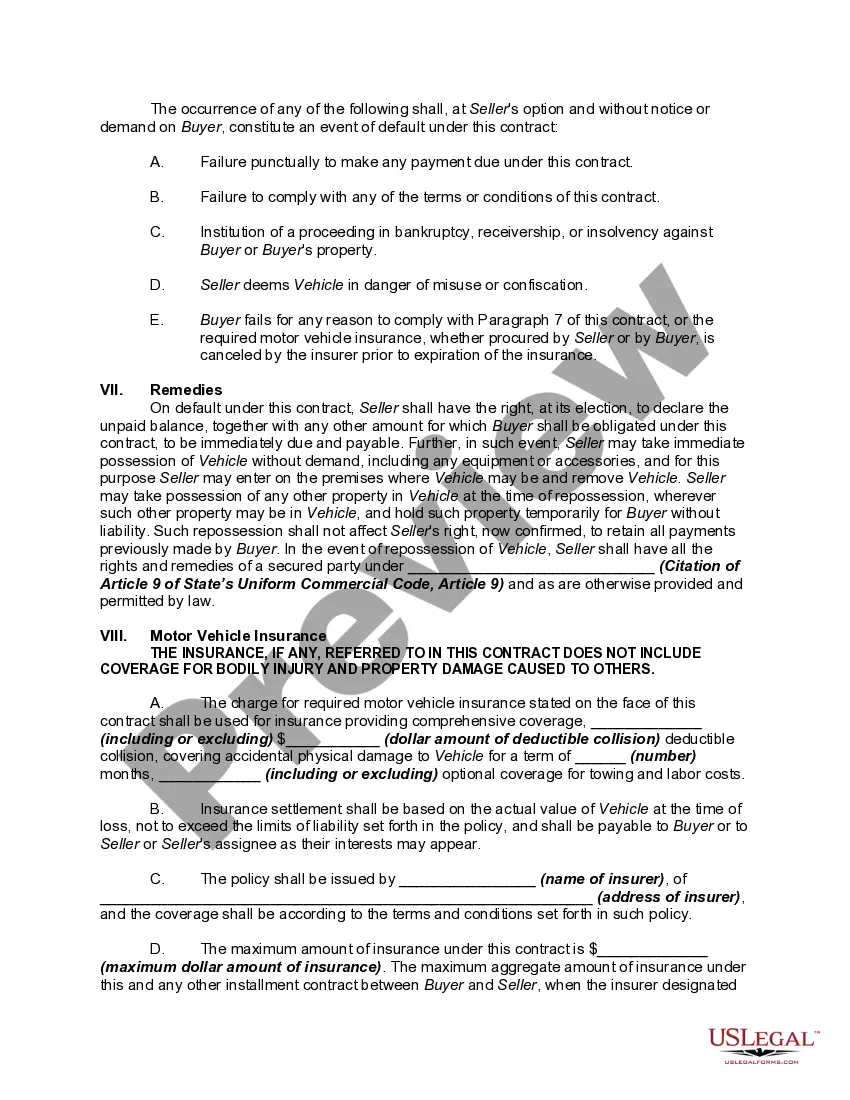

Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is a legal document used in the state of Maryland to secure a loan provided by a lender for the purchase of an automobile, car, or motor vehicle. It outlines the terms and conditions of the loan agreement, including the repayment schedule and the rights and responsibilities of both parties involved. The purpose of the Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is to protect the lender's interest in the vehicle as collateral until the loan amount is fully repaid. It ensures that the lender has the right to repossess the vehicle in the event of default by the borrower. The security agreement includes various key elements such as the details of the borrower and the lender, the vehicle's make, model, and identification number (VIN), the loan amount, annual percentage rate (APR), and the repayment schedule. It also includes provisions regarding insurance requirements, default clauses, and the consequences of default. Different types of Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle may exist based on specific circumstances or additional clauses added by the lender. Some variations may include: 1. Maryland Security Agreement with Cosigner: This type of security agreement involves a cosigner who guarantees the repayment of the loan in case the primary borrower defaults. It provides an extra layer of security for the lender. 2. Maryland Security Agreement with Balloon Payment: In this case, the borrower agrees to make smaller monthly payments initially, followed by a larger final payment known as a balloon payment. This type of agreement may be suitable for borrowers who expect increased income or plan to refinance the vehicle before the balloon payment becomes due. 3. Maryland Security Agreement with Purchase Option: This agreement may provide the borrower with a purchase option at the end of the loan term. The borrower can choose to buy the vehicle at a predetermined price or return it to the lender. It is important for both lenders and borrowers to understand the terms and conditions detailed in the Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle. Seeking legal advice or consulting a financial professional is recommended to ensure compliance with Maryland state laws and to protect the interests of both parties involved.Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is a legal document used in the state of Maryland to secure a loan provided by a lender for the purchase of an automobile, car, or motor vehicle. It outlines the terms and conditions of the loan agreement, including the repayment schedule and the rights and responsibilities of both parties involved. The purpose of the Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is to protect the lender's interest in the vehicle as collateral until the loan amount is fully repaid. It ensures that the lender has the right to repossess the vehicle in the event of default by the borrower. The security agreement includes various key elements such as the details of the borrower and the lender, the vehicle's make, model, and identification number (VIN), the loan amount, annual percentage rate (APR), and the repayment schedule. It also includes provisions regarding insurance requirements, default clauses, and the consequences of default. Different types of Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle may exist based on specific circumstances or additional clauses added by the lender. Some variations may include: 1. Maryland Security Agreement with Cosigner: This type of security agreement involves a cosigner who guarantees the repayment of the loan in case the primary borrower defaults. It provides an extra layer of security for the lender. 2. Maryland Security Agreement with Balloon Payment: In this case, the borrower agrees to make smaller monthly payments initially, followed by a larger final payment known as a balloon payment. This type of agreement may be suitable for borrowers who expect increased income or plan to refinance the vehicle before the balloon payment becomes due. 3. Maryland Security Agreement with Purchase Option: This agreement may provide the borrower with a purchase option at the end of the loan term. The borrower can choose to buy the vehicle at a predetermined price or return it to the lender. It is important for both lenders and borrowers to understand the terms and conditions detailed in the Maryland Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle. Seeking legal advice or consulting a financial professional is recommended to ensure compliance with Maryland state laws and to protect the interests of both parties involved.