The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

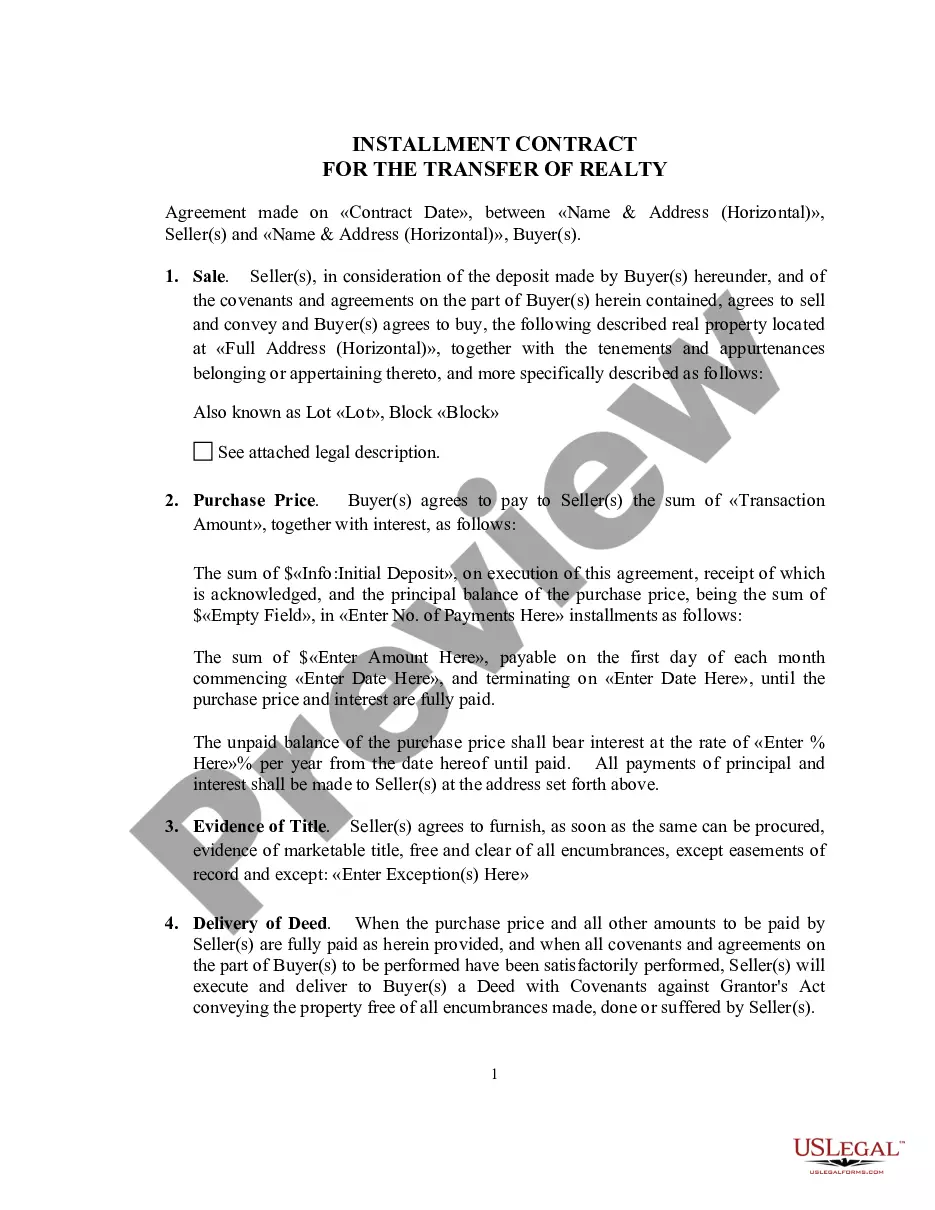

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

Are you in a position where you need documents for potential organizational or personal use almost every day.

There are many legal document templates available online, but finding ones you can trust is not easy.

US Legal Forms provides thousands of document templates, such as the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, which are designed to meet state and federal requirements.

Select a suitable file format and download your version.

Retrieve all the document templates you have purchased in the My documents section. You can get an additional copy of the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures whenever necessary. Simply access the desired document to download or print the template.

- If you are already familiar with the US Legal Forms site and have an account, simply Log In.

- Then, you can download the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Find the document you need and ensure it is for the correct city/region.

- Use the Preview option to view the document.

- Check the information to confirm that you have selected the correct document.

- If the document is not what you are looking for, use the Search field to find the document that meets your needs and requirements.

- Once you find the right document, click Get now.

- Choose the pricing plan you want, fill in the required information to create your account, and pay for the transaction with your PayPal or credit card.

Form popularity

FAQ

The Truth in Lending Act requires retail businesses to communicate essential credit terms to consumers clearly and transparently. Retailers must provide disclosures that align with the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, helping consumers understand their repayment responsibilities. By adhering to these requirements, businesses foster trust and promote responsible borrowing.

The Truth in Lending Disclosure requires lenders to disclose several critical items. These include the annual percentage rate (APR), finance charges, payment schedule, and total amount financed. By complying with the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, lenders ensure that consumers receive the necessary information to make informed financial decisions.

Regulation Z mandates that lenders provide clear and comprehensive disclosures to borrowers. This includes details about the terms and costs associated with credit agreements. Specifically, for Maryland, these disclosures detail the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, ensuring borrowers understand their financial obligations and rights.

According to Regulation Z, all material closed-end credit disclosures must be presented clearly and conspicuously, using easily readable formats. Disclosures should not use fine print or misleading language, making information accessible for consumers. Adhering to the Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures ensures that you receive straightforward and honest details about your credit terms.

Regulation Z is a federal regulation that implements the Truth in Lending Act, primarily focusing on closed-end credit transactions. It requires creditors to disclose key terms and costs so consumers can make educated decisions about borrowing. The Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures incorporates Regulation Z to protect consumers and promote fair and transparent lending practices.

A truth in lending disclosure statement must include vital information such as the annual percentage rate (APR), the total finance charges, and the total amount financed. It should clearly outline the payment terms and the consequences of failing to meet payment obligations. The Maryland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures ensures transparency in these vital aspects.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

Terms in this set (10) The Truth-in-Lending Act promotes the informed use of credit and protects borrowers from unethical lenders by requiring the clear and conspicuous disclosure of the terms and conditions of consumer loans offered.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.