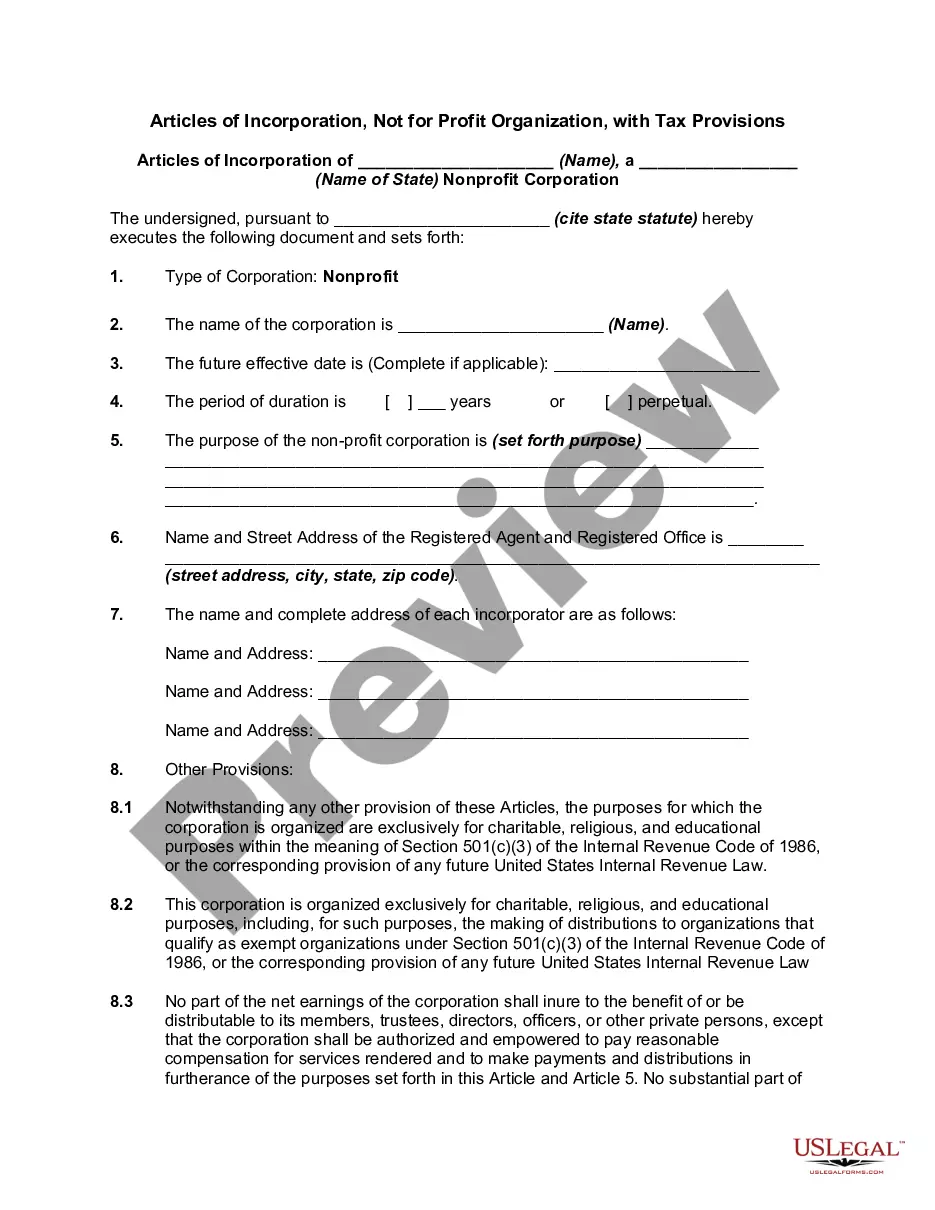

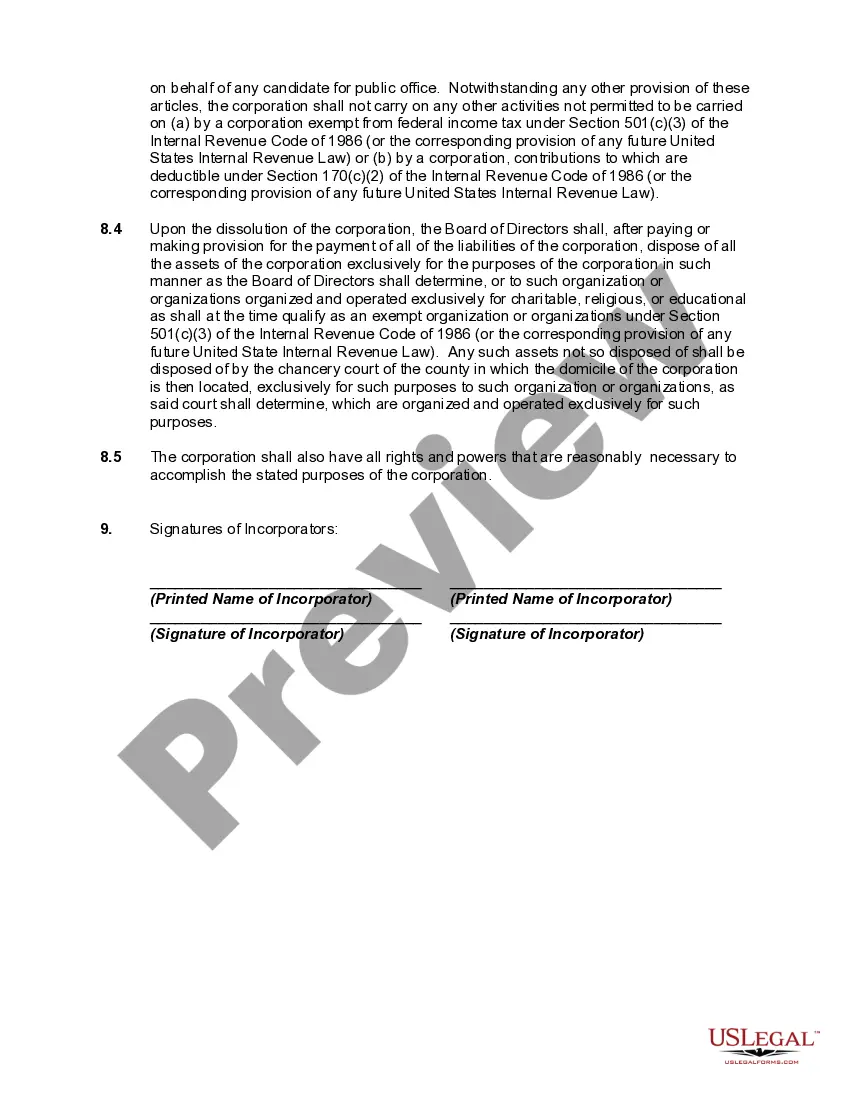

Maryland Articles of Incorporation — Not for Profit Organization with Tax Provisions: A Comprehensive Overview Keywords: Maryland, Articles of Incorporation, Not for Profit Organization, Tax Provisions. Introduction: The Maryland Articles of Incorporation for a Not for Profit Organization with Tax Provisions are legal documents that establish the formation of a non-profit entity within the state. These articles serve as the foundation for operating and managing the organization, highlighting its purpose, structure, and compliance with tax regulations. In Maryland, there are different types of Articles of Incorporation for Not for Profit Organizations with varying tax provisions, including: 1. General Not for Profit Corporations: General Not for Profit Corporations are the most common type of non-profit organizations in Maryland. These organizations are established for charitable, educational, religious, scientific, or literary purposes, focusing on providing services to the community. The articles outline the purpose of the organization, its governance structure, and its compliance with Maryland tax provisions. 2. Religious Corporations: Religious Corporations are specific entities formed for religious purposes such as churches, temples, mosques, or other religious institutions. These articles emphasize the purpose of the organization, including its religious doctrine, rituals, and practices. They also outline the governance structure, membership requirements, and tax provisions relevant to religious organizations in Maryland. 3. Public Benefit Corporations: Public Benefit Corporations are non-profit organizations established with the objective of serving and benefiting the public, or a specific segment of society. These articles detail the specific public benefit or service the organization aims to provide, outlining its governance structure, membership requirements, and compliance with tax provisions applicable to public benefit organizations in Maryland. 4. Mutual Benefit Corporations: Mutual Benefit Corporations are non-profit organizations formed for the mutual benefit of their members, who may be individuals or other organizations. These articles specify the mutual benefit the organization is established to provide, outlining its governance structure, membership requirements, and the taxation provisions applicable to mutual benefit organizations in Maryland. Tax Provisions: In Maryland, non-profit organizations enjoy certain tax exemptions and benefits. The Articles of Incorporation for Not for Profit Organizations with Tax Provisions duly highlight the organization's compliance with these tax regulations. — Federal Tax-Exempt Status: The articles establish the organization's eligibility for federal tax-exempt status under section 501(c) of the Internal Revenue Code×. This ensures the organization's income is not subject to federal income tax. — State Tax Exemptions: The articles outline the requirements and qualifications for Maryland state tax exemptions, such as sales, property, or income tax exemptions. These exemptions aim to encourage and support the non-profit organization's charitable, educational, religious, scientific, or literary purposes. Conclusion: The Maryland Articles of Incorporation for Not for Profit Organizations with Tax Provisions are essential legal documents that establish the formation of non-profit entities within the state. These documents differ based on the organization's purpose, such as general not-for-profit, religious, public benefit, or mutual benefit corporations. By properly addressing tax provisions and qualifications for tax exemptions, the articles ensure compliance with both federal and state tax regulations. The establishment of these articles sets the legal framework for the organization's operations, governance structure, and its commitment to serving the public interest or members' mutual benefit. *Note: Compliance with federal tax regulations requires separate application and approval from the Internal Revenue Service (IRS).

Maryland Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Maryland Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

US Legal Forms - one of many biggest libraries of legitimate types in the United States - gives a wide array of legitimate papers templates it is possible to download or printing. While using web site, you will get a huge number of types for enterprise and individual uses, categorized by classes, claims, or search phrases.You can get the latest variations of types such as the Maryland Articles of Incorporation, Not for Profit Organization, with Tax Provisions within minutes.

If you already possess a membership, log in and download Maryland Articles of Incorporation, Not for Profit Organization, with Tax Provisions from the US Legal Forms local library. The Obtain switch will appear on every single form you view. You gain access to all previously saved types within the My Forms tab of your own bank account.

If you want to use US Legal Forms the first time, listed below are simple directions to help you get started:

- Ensure you have chosen the best form for your personal area/area. Select the Preview switch to analyze the form`s information. See the form outline to actually have selected the right form.

- In case the form does not match your requirements, make use of the Research area at the top of the screen to get the the one that does.

- When you are satisfied with the form, confirm your decision by simply clicking the Purchase now switch. Then, choose the costs prepare you like and provide your accreditations to sign up on an bank account.

- Method the deal. Use your charge card or PayPal bank account to perform the deal.

- Choose the formatting and download the form on the gadget.

- Make adjustments. Fill out, modify and printing and sign the saved Maryland Articles of Incorporation, Not for Profit Organization, with Tax Provisions.

Every single web template you included in your money lacks an expiration date and is the one you have forever. So, if you want to download or printing an additional duplicate, just check out the My Forms segment and then click around the form you want.

Get access to the Maryland Articles of Incorporation, Not for Profit Organization, with Tax Provisions with US Legal Forms, by far the most extensive local library of legitimate papers templates. Use a huge number of professional and state-certain templates that meet your business or individual needs and requirements.