Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

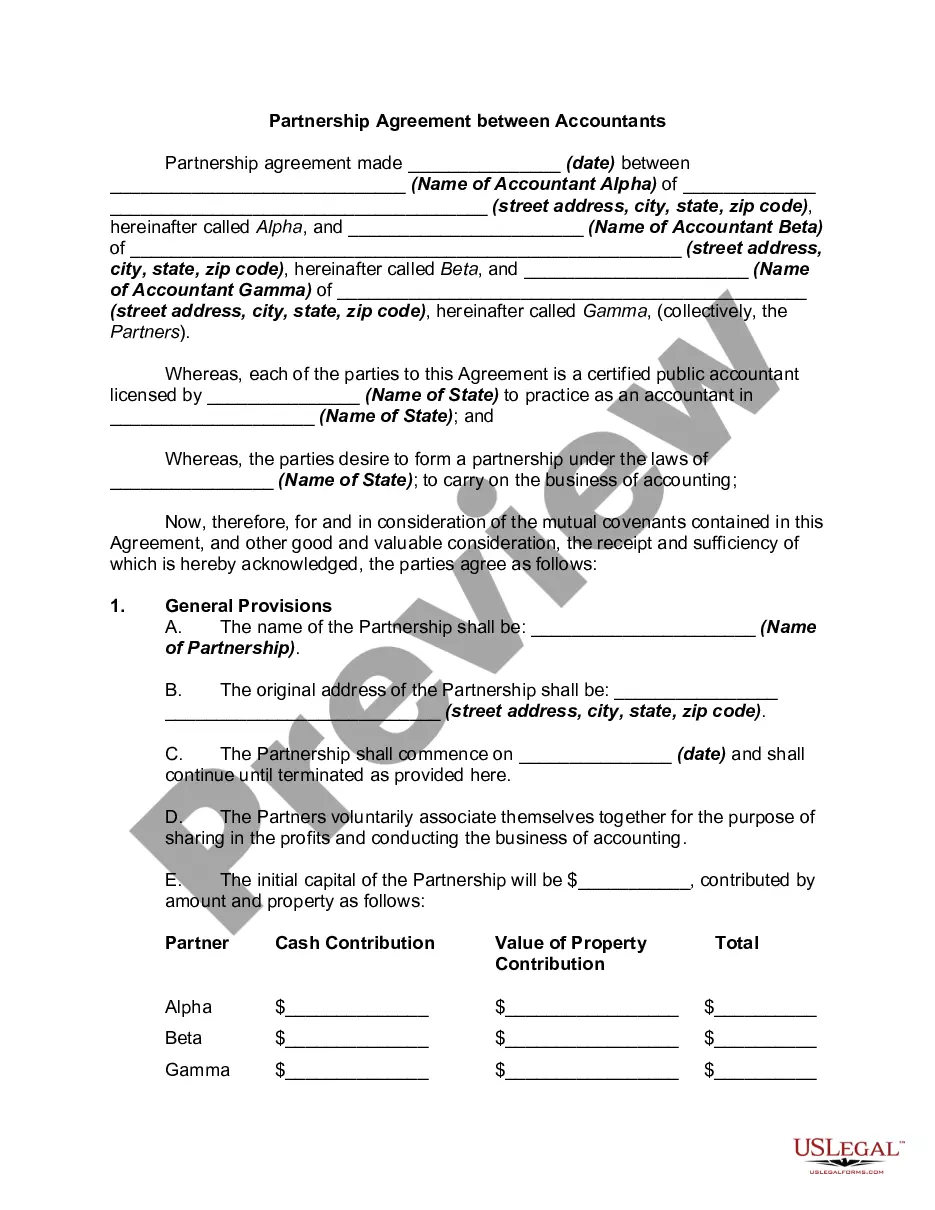

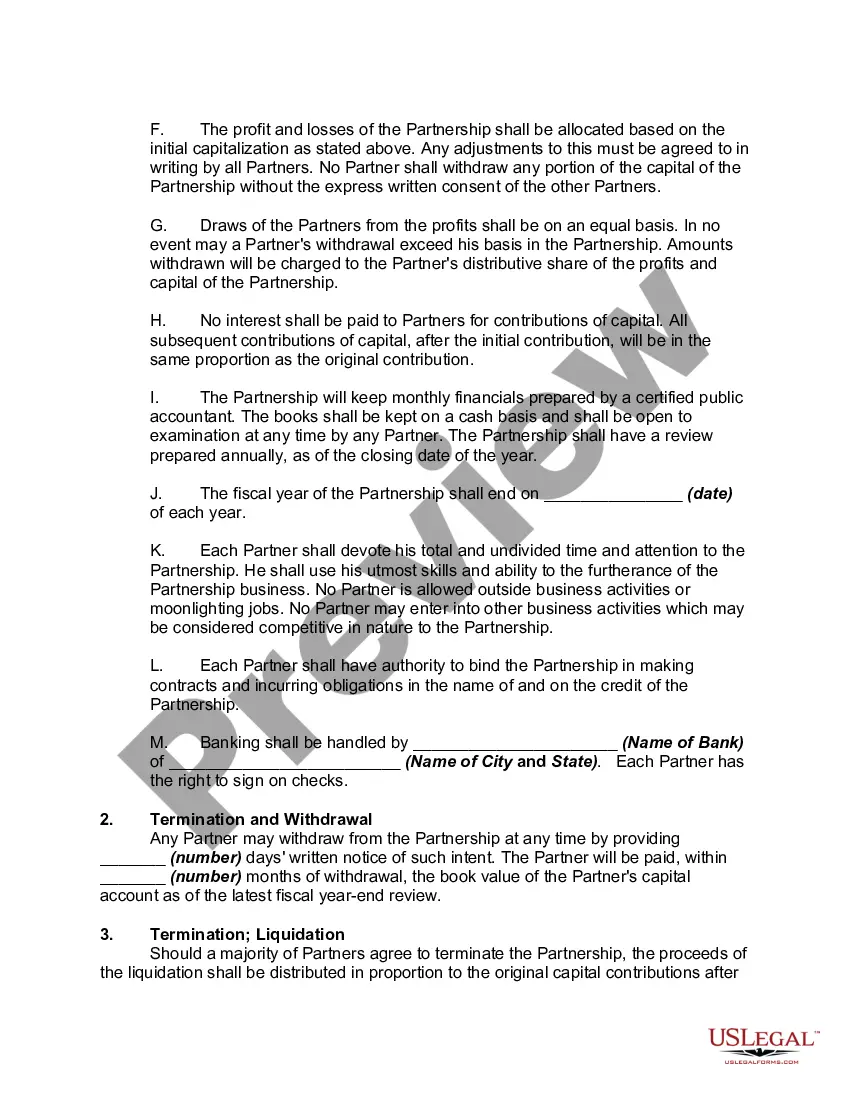

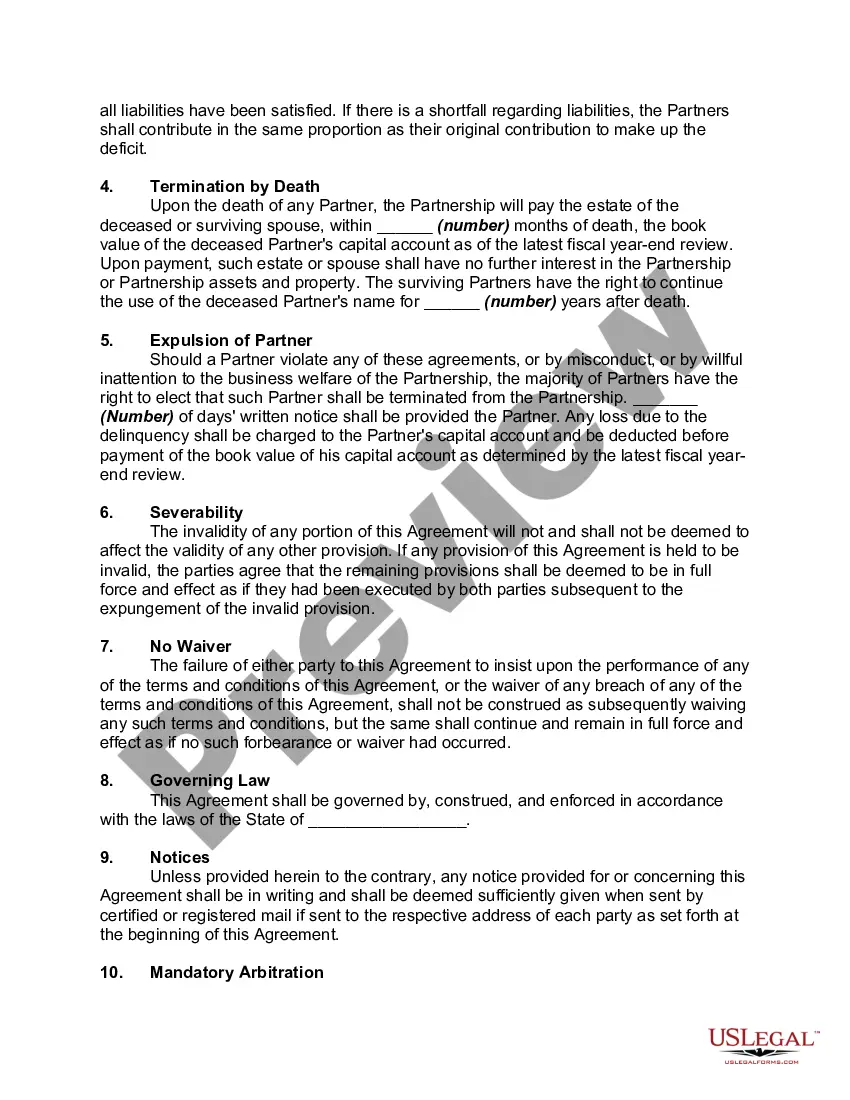

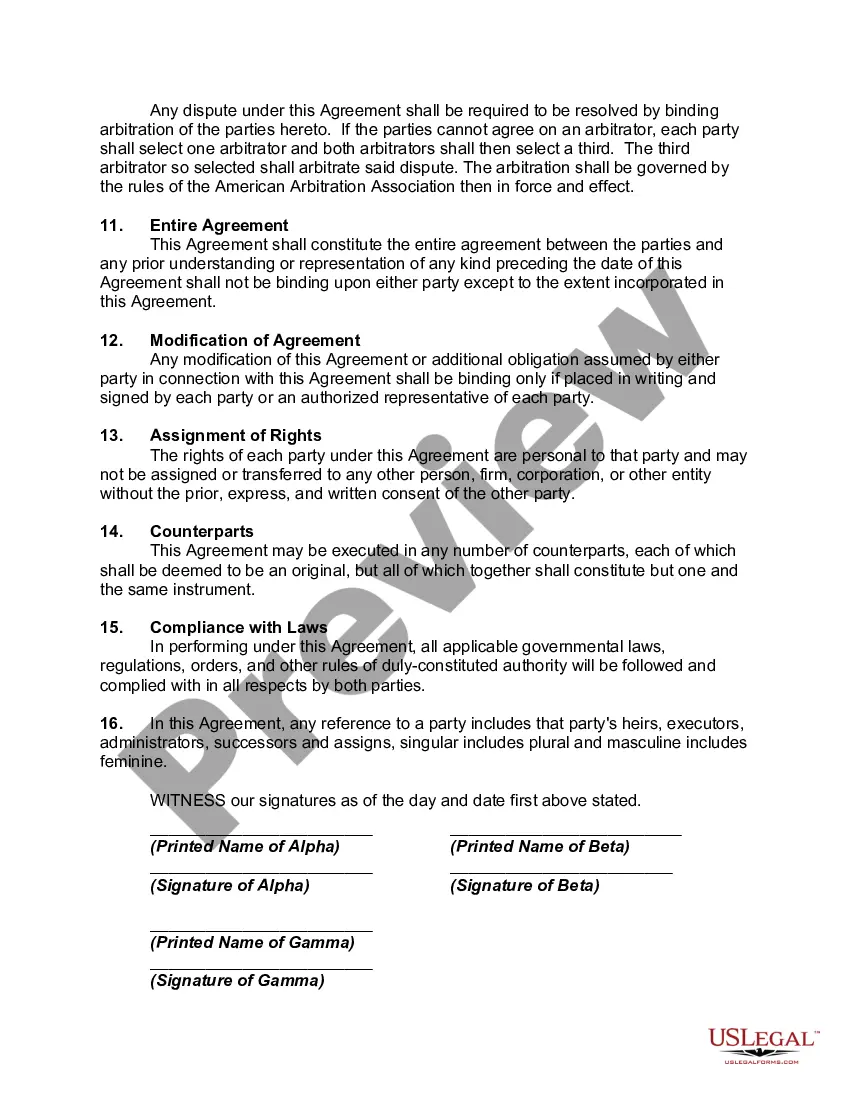

A Maryland Partnership Agreement Between Accountants is a legal document that outlines the terms and conditions governing the partnership between two or more accounting professionals in the state of Maryland. This agreement serves as a guidebook for the partners regarding their roles, responsibilities, profit-sharing structure, decision-making process, and other crucial aspects of the partnership. Key provisions typically included in a Maryland Partnership Agreement Between Accountants may consist of: 1. Partnership Name: The agreement should mention the official name of the partnership, which is typically a combination of the partners' last names. 2. Purpose: This section defines the nature and purpose of the partnership, such as providing accounting services or consulting to clients. 3. Capital Contributions: Partners often contribute initial capital to the partnership. The agreement should specify the amount and nature of the contributions made by each partner, which can be in cash, property, or services. 4. Profits and Losses: The sharing of profits and losses among partners is a critical aspect of any partnership agreement. This section outlines how the profits and losses will be allocated among the partners, typically based on their capital contributions or an agreed percentage. 5. Decision-Making: The agreement should delineate how key decisions within the partnership will be made. This may involve voting rights, super majority requirements, or a designated managing partner responsible for making executive decisions. 6. Management and Authority: The roles and responsibilities of each partner in managing the partnership should be clearly defined. Some partnerships may have one managing partner with significant decision-making power, while others may distribute management responsibilities equally. 7. Dissolution: This section outlines the process of dissolving the partnership, including the steps required to wind up the partnership's affairs, distribute assets, and settle any outstanding liabilities. Types of Maryland Partnership Agreements Between Accountants: 1. General Partnership: A general partnership is the simplest form of partnership, where each partner shares equal responsibility and unlimited liability for the partnership's obligations. 2. Limited Partnership: In a limited partnership, there are general partners who manage the business and have unlimited liability, while limited partners contribute capital but have limited liability for the partnership's debts. 3. Limited Liability Partnership (LLP): An LLP combines aspects of a general partnership and a corporation. It offers limited liability to all partners while allowing them to actively participate in the management and operation of the business. In conclusion, a Maryland Partnership Agreement Between Accountants is a legally binding document that establishes the terms and conditions of a partnership between accounting professionals in Maryland. It covers various aspects such as capital contributions, profit sharing, decision-making, management, and dissolution. Different types of partnership agreements include general partnerships, limited partnerships, and limited liability partnerships (LLP).A Maryland Partnership Agreement Between Accountants is a legal document that outlines the terms and conditions governing the partnership between two or more accounting professionals in the state of Maryland. This agreement serves as a guidebook for the partners regarding their roles, responsibilities, profit-sharing structure, decision-making process, and other crucial aspects of the partnership. Key provisions typically included in a Maryland Partnership Agreement Between Accountants may consist of: 1. Partnership Name: The agreement should mention the official name of the partnership, which is typically a combination of the partners' last names. 2. Purpose: This section defines the nature and purpose of the partnership, such as providing accounting services or consulting to clients. 3. Capital Contributions: Partners often contribute initial capital to the partnership. The agreement should specify the amount and nature of the contributions made by each partner, which can be in cash, property, or services. 4. Profits and Losses: The sharing of profits and losses among partners is a critical aspect of any partnership agreement. This section outlines how the profits and losses will be allocated among the partners, typically based on their capital contributions or an agreed percentage. 5. Decision-Making: The agreement should delineate how key decisions within the partnership will be made. This may involve voting rights, super majority requirements, or a designated managing partner responsible for making executive decisions. 6. Management and Authority: The roles and responsibilities of each partner in managing the partnership should be clearly defined. Some partnerships may have one managing partner with significant decision-making power, while others may distribute management responsibilities equally. 7. Dissolution: This section outlines the process of dissolving the partnership, including the steps required to wind up the partnership's affairs, distribute assets, and settle any outstanding liabilities. Types of Maryland Partnership Agreements Between Accountants: 1. General Partnership: A general partnership is the simplest form of partnership, where each partner shares equal responsibility and unlimited liability for the partnership's obligations. 2. Limited Partnership: In a limited partnership, there are general partners who manage the business and have unlimited liability, while limited partners contribute capital but have limited liability for the partnership's debts. 3. Limited Liability Partnership (LLP): An LLP combines aspects of a general partnership and a corporation. It offers limited liability to all partners while allowing them to actively participate in the management and operation of the business. In conclusion, a Maryland Partnership Agreement Between Accountants is a legally binding document that establishes the terms and conditions of a partnership between accounting professionals in Maryland. It covers various aspects such as capital contributions, profit sharing, decision-making, management, and dissolution. Different types of partnership agreements include general partnerships, limited partnerships, and limited liability partnerships (LLP).