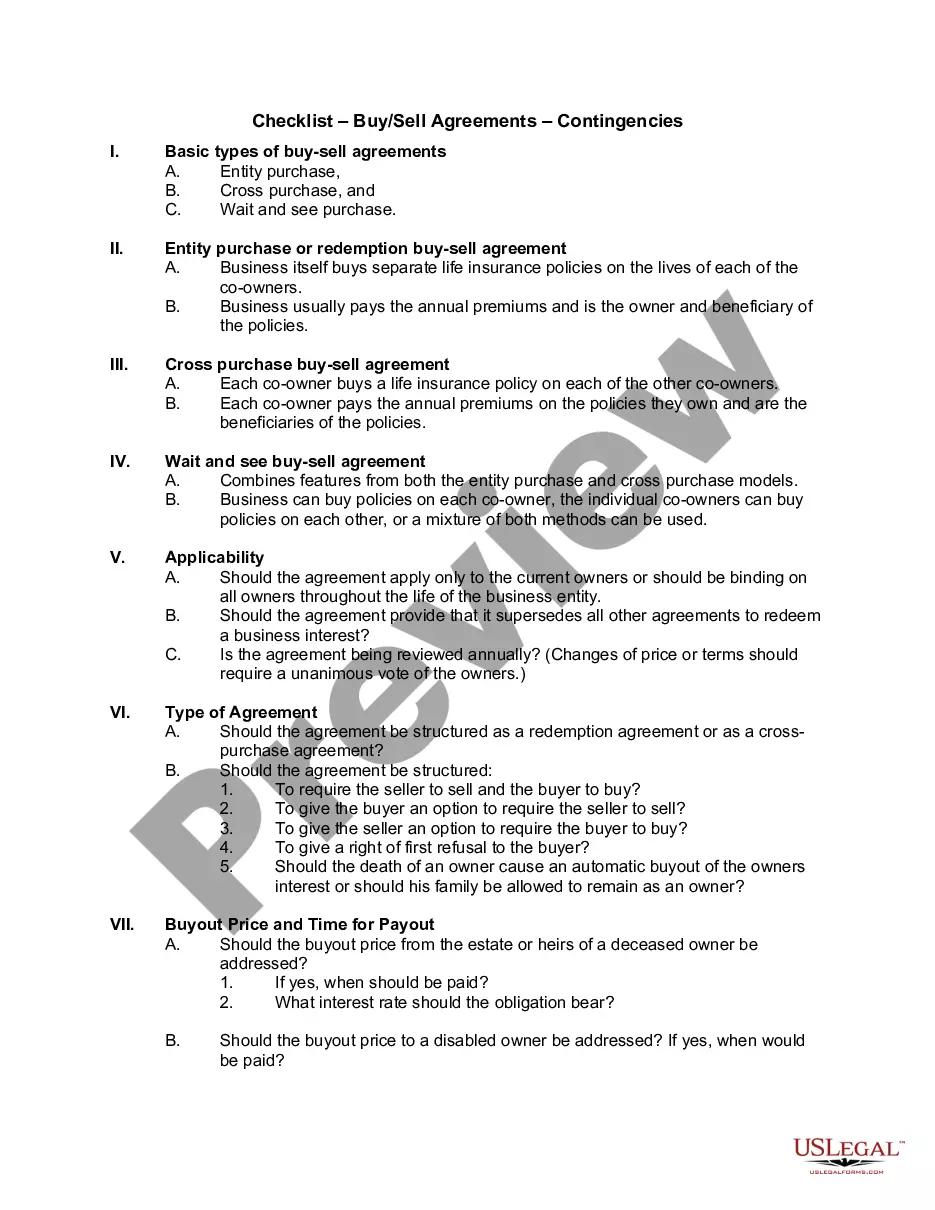

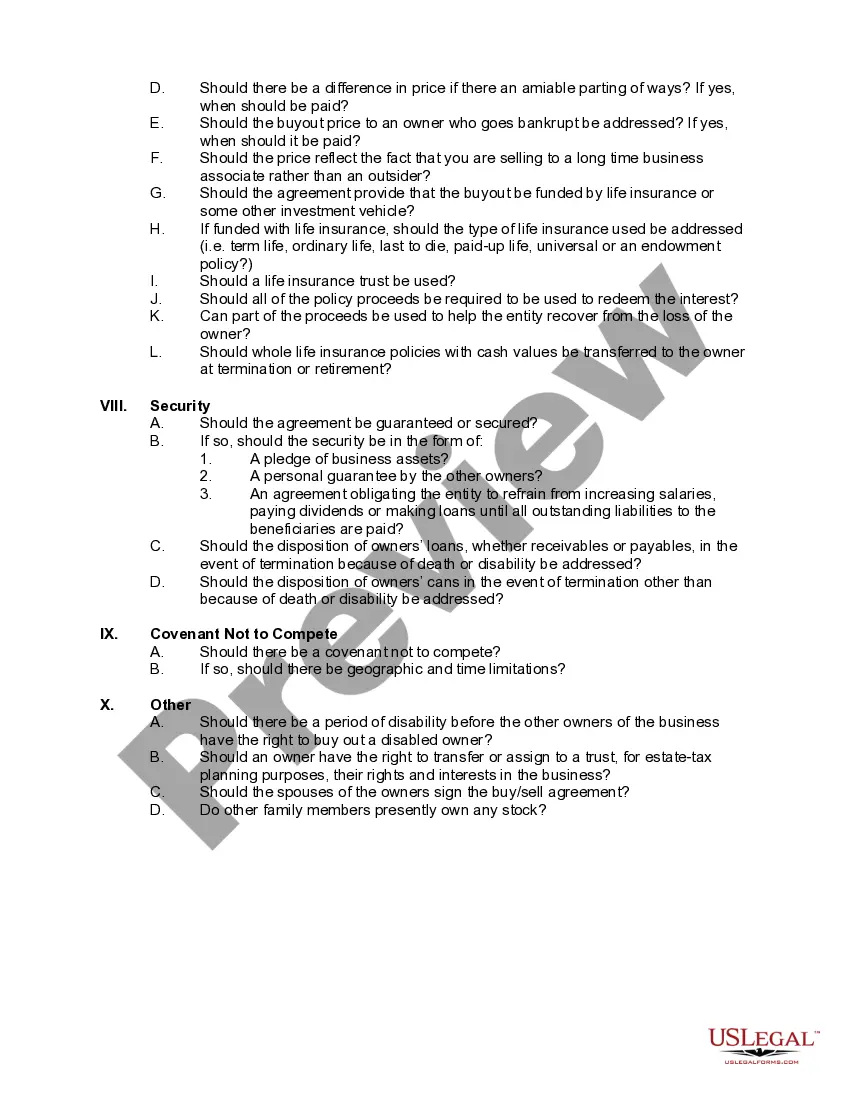

A buy-sell agreement is an agreement between the owners of the business for purchase of each others interest in the business. Such an agreement will spell out the terms governing sale of company stock to an outsider and thus protect control of the company. It can be triggered in the event of the owner's death, disability, retirement, withdrawal from the business or other events. Life insurance owned by the corporation is often used to provide the funds to purchase the shares of a closely held company if one of the owners dies.

The time to prevent disputes is before they occur. Experience proves that owners anxieties created in dealing with one another are inversely proportional to the effort they spend addressing business problems in the event that they should happen. Dealing with these contingencies before they manifest themselves is the secret to a harmonious business relationship with other owners, Use the checklist below to determine areas where you may need assistance.

Maryland Checklist — Buy/Sell Agreement— - Contingencies: In Maryland, when entering into a buy/sell agreement, various contingencies need to be considered to protect the parties involved. These contingencies act as safeguards, outlining conditions that must be met before completing the purchase or sale of a property or business. Here is a detailed description of what these contingencies entail, along with some important keywords: 1. Financing Contingency: One of the essential contingencies in a buy/sell agreement is the financing contingency. This clause allows the buyer to secure financing for the purchase. It specifies a timeline within which the buyer should obtain a mortgage commitment, and if they fail to do so, they can back out of the agreement without any penalties. 2. Inspection Contingency: This contingency allows the buyer to conduct a thorough inspection of the property or business. It ensures that the buyer is aware of any defects, damages, or issues that may affect the property's value or desirability. If the inspection reveals significant problems, the buyer can negotiate repairs, credits, or terminate the agreement altogether. 3. Appraisal Contingency: An appraisal contingency is crucial when the buyer needs a mortgage to fund the purchase. It requires the property to be appraised at or above the agreed-upon sale price. If the appraisal falls short, the buyer can renegotiate the price, request the seller to lower it, or terminate the agreement. 4. Title Contingency: In Maryland, a title contingency is typically included in buy/sell agreements. It ensures that the seller has clear and marketable title to the property, free from any liens or encumbrances. If any issues arise during the title search, the buyer has the option to address them, obtain title insurance, or cancel the agreement. 5. Home Sale Contingency: This contingency is applied when the buyer needs to sell their current home before completing the purchase. It provides a specific timeframe for the buyer to sell their property. If the buyer fails to sell their home within the specified period, they can terminate the agreement without consequences. Other types of contingencies that might be relevant in Maryland buy/sell agreements may include: — Financing Contingency Waiver: This contingency applies when the buyer can purchase the property without relying on financing. It removes the requirement for a mortgage commitment and expedites the purchase process. — Settlement Contingency: This contingency sets a specific date by when the settlement must take place. If either party fails to meet the deadline, the other party may have the right to pursue legal action or terminate the agreement. — Zoning or Land Use Contingency: This contingency ensures that the property can be used for the intended purpose. If any zoning or land use issues arise during due diligence, the buyer may have the right to negotiate or possibly withdraw from the agreement. Understanding and carefully considering these contingencies in a Maryland buy/sell agreement is vital for protecting the rights and interests of both buyers and sellers. It is crucial to consult with an experienced real estate attorney to ensure that all necessary contingencies are included and that the agreement meets the specific requirements and regulations of the Maryland jurisdiction.Maryland Checklist — Buy/Sell Agreement— - Contingencies: In Maryland, when entering into a buy/sell agreement, various contingencies need to be considered to protect the parties involved. These contingencies act as safeguards, outlining conditions that must be met before completing the purchase or sale of a property or business. Here is a detailed description of what these contingencies entail, along with some important keywords: 1. Financing Contingency: One of the essential contingencies in a buy/sell agreement is the financing contingency. This clause allows the buyer to secure financing for the purchase. It specifies a timeline within which the buyer should obtain a mortgage commitment, and if they fail to do so, they can back out of the agreement without any penalties. 2. Inspection Contingency: This contingency allows the buyer to conduct a thorough inspection of the property or business. It ensures that the buyer is aware of any defects, damages, or issues that may affect the property's value or desirability. If the inspection reveals significant problems, the buyer can negotiate repairs, credits, or terminate the agreement altogether. 3. Appraisal Contingency: An appraisal contingency is crucial when the buyer needs a mortgage to fund the purchase. It requires the property to be appraised at or above the agreed-upon sale price. If the appraisal falls short, the buyer can renegotiate the price, request the seller to lower it, or terminate the agreement. 4. Title Contingency: In Maryland, a title contingency is typically included in buy/sell agreements. It ensures that the seller has clear and marketable title to the property, free from any liens or encumbrances. If any issues arise during the title search, the buyer has the option to address them, obtain title insurance, or cancel the agreement. 5. Home Sale Contingency: This contingency is applied when the buyer needs to sell their current home before completing the purchase. It provides a specific timeframe for the buyer to sell their property. If the buyer fails to sell their home within the specified period, they can terminate the agreement without consequences. Other types of contingencies that might be relevant in Maryland buy/sell agreements may include: — Financing Contingency Waiver: This contingency applies when the buyer can purchase the property without relying on financing. It removes the requirement for a mortgage commitment and expedites the purchase process. — Settlement Contingency: This contingency sets a specific date by when the settlement must take place. If either party fails to meet the deadline, the other party may have the right to pursue legal action or terminate the agreement. — Zoning or Land Use Contingency: This contingency ensures that the property can be used for the intended purpose. If any zoning or land use issues arise during due diligence, the buyer may have the right to negotiate or possibly withdraw from the agreement. Understanding and carefully considering these contingencies in a Maryland buy/sell agreement is vital for protecting the rights and interests of both buyers and sellers. It is crucial to consult with an experienced real estate attorney to ensure that all necessary contingencies are included and that the agreement meets the specific requirements and regulations of the Maryland jurisdiction.