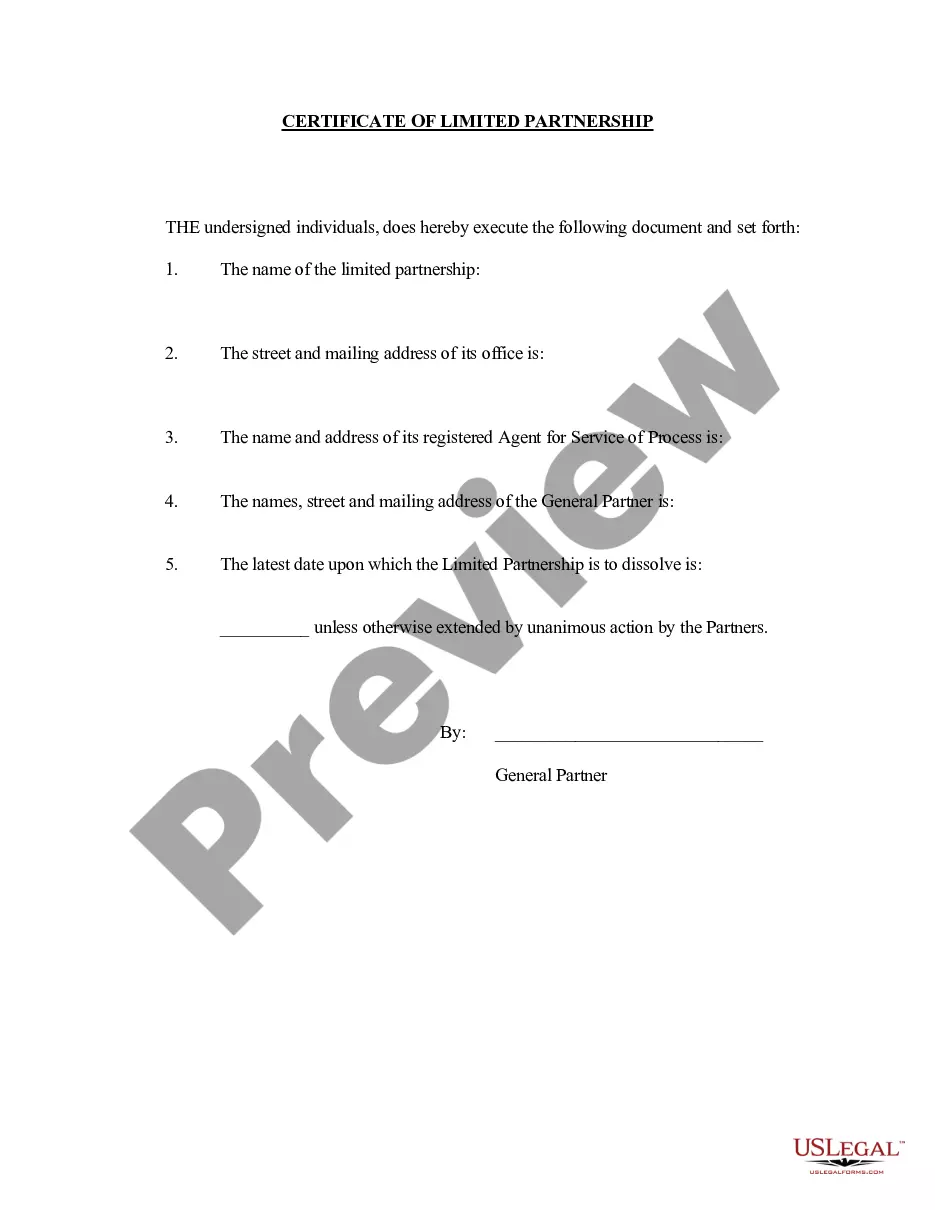

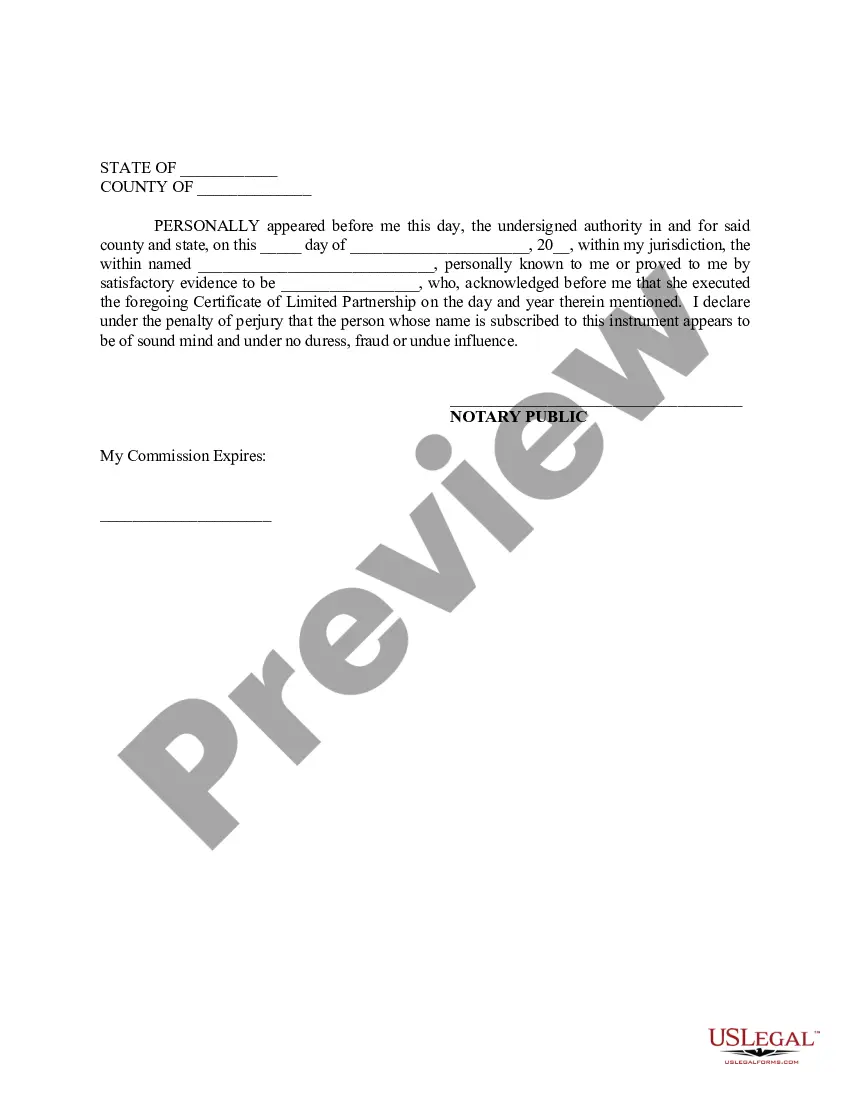

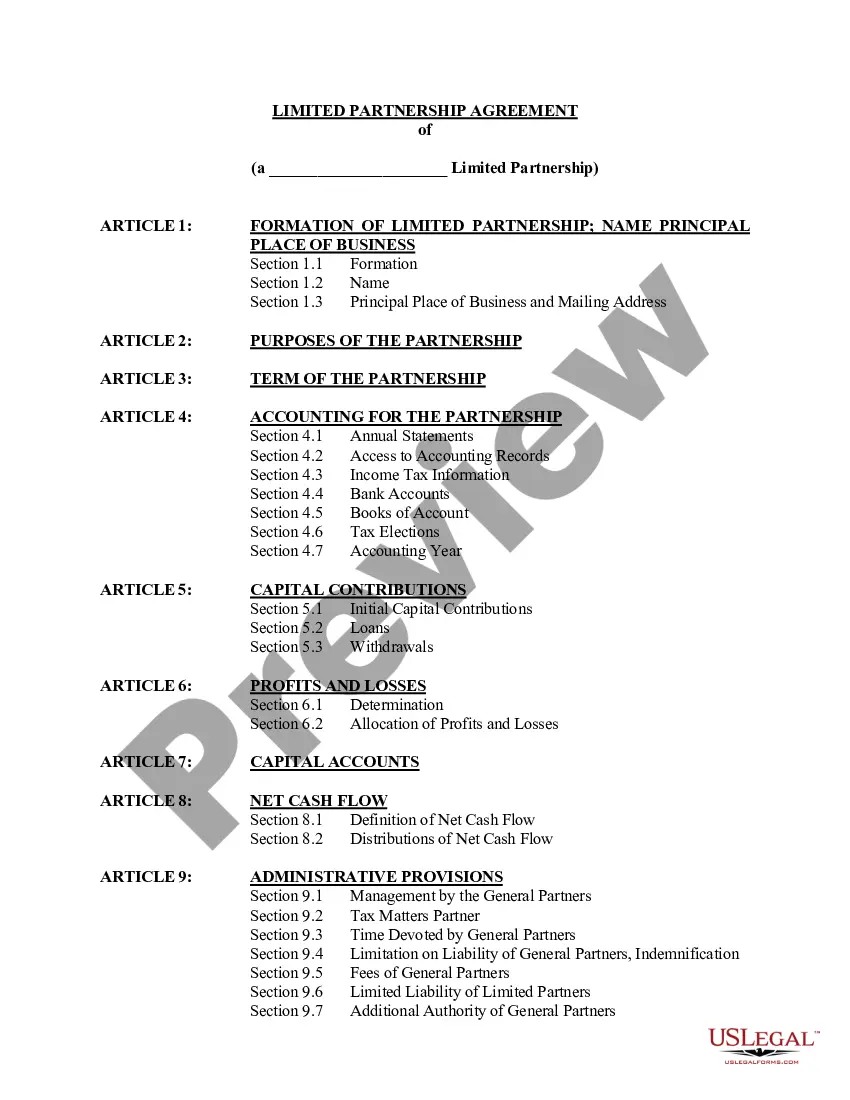

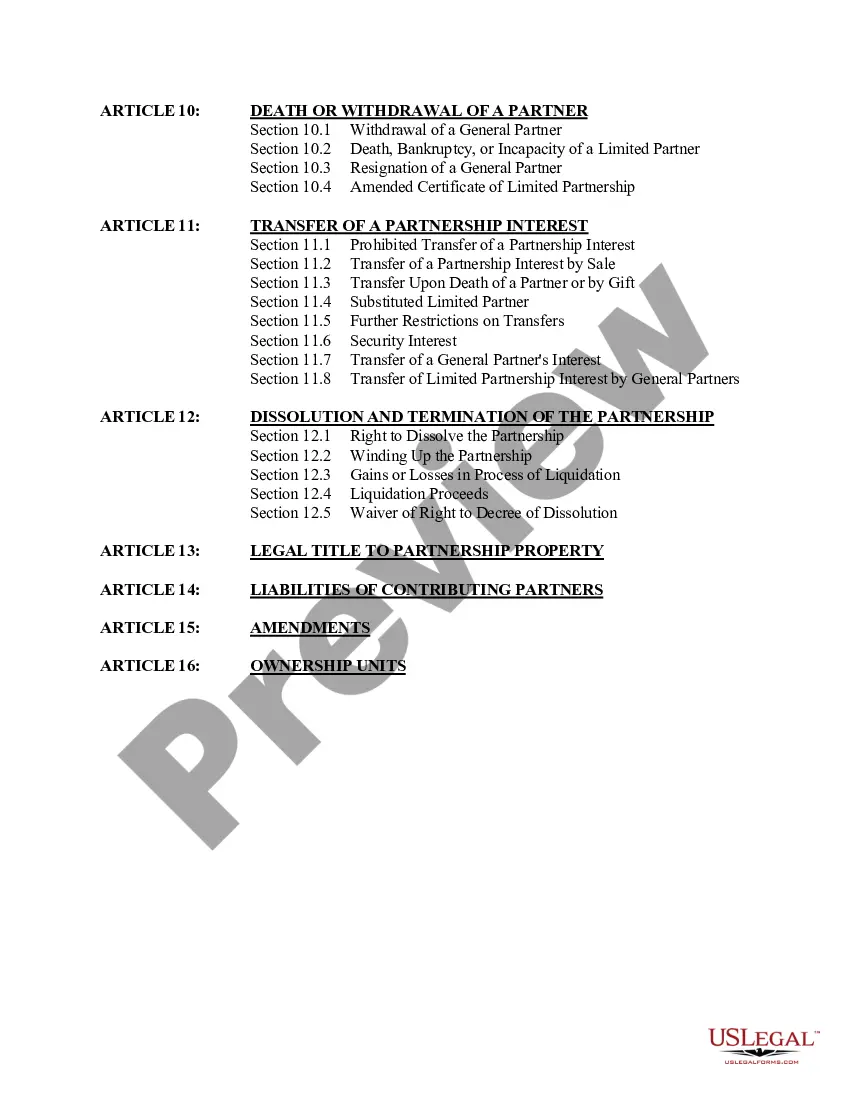

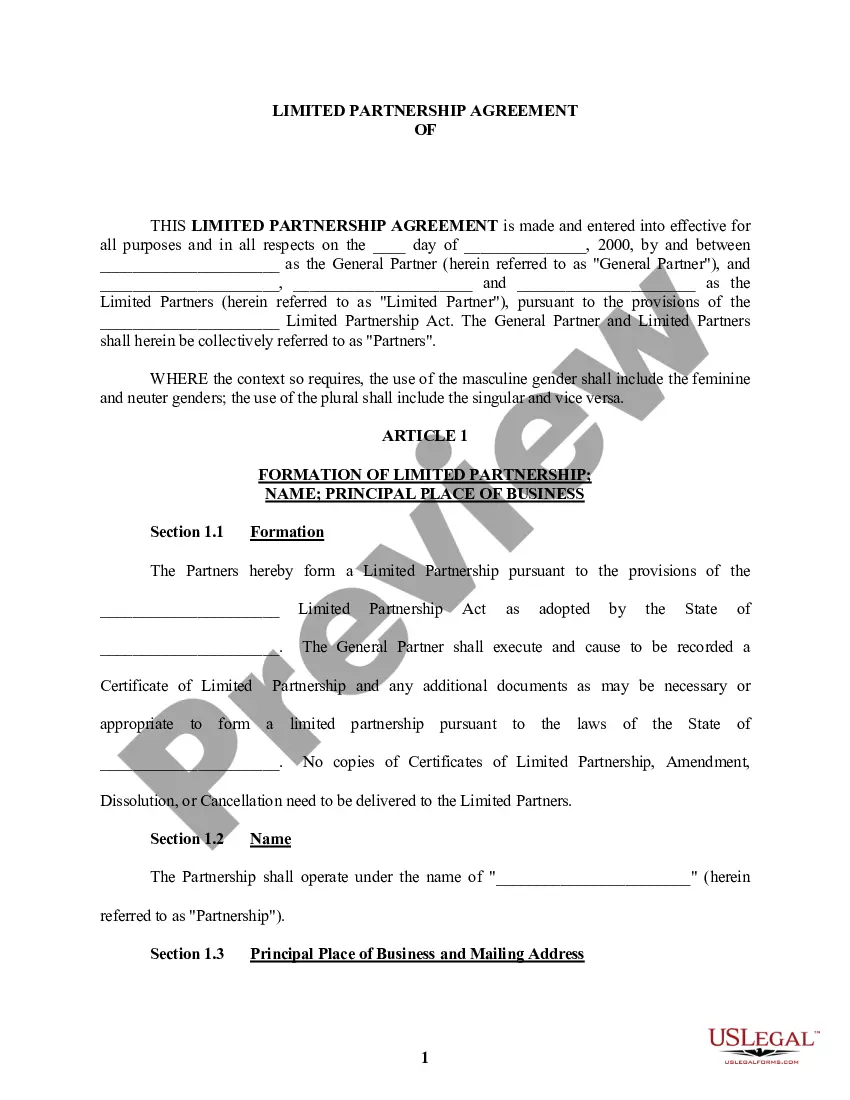

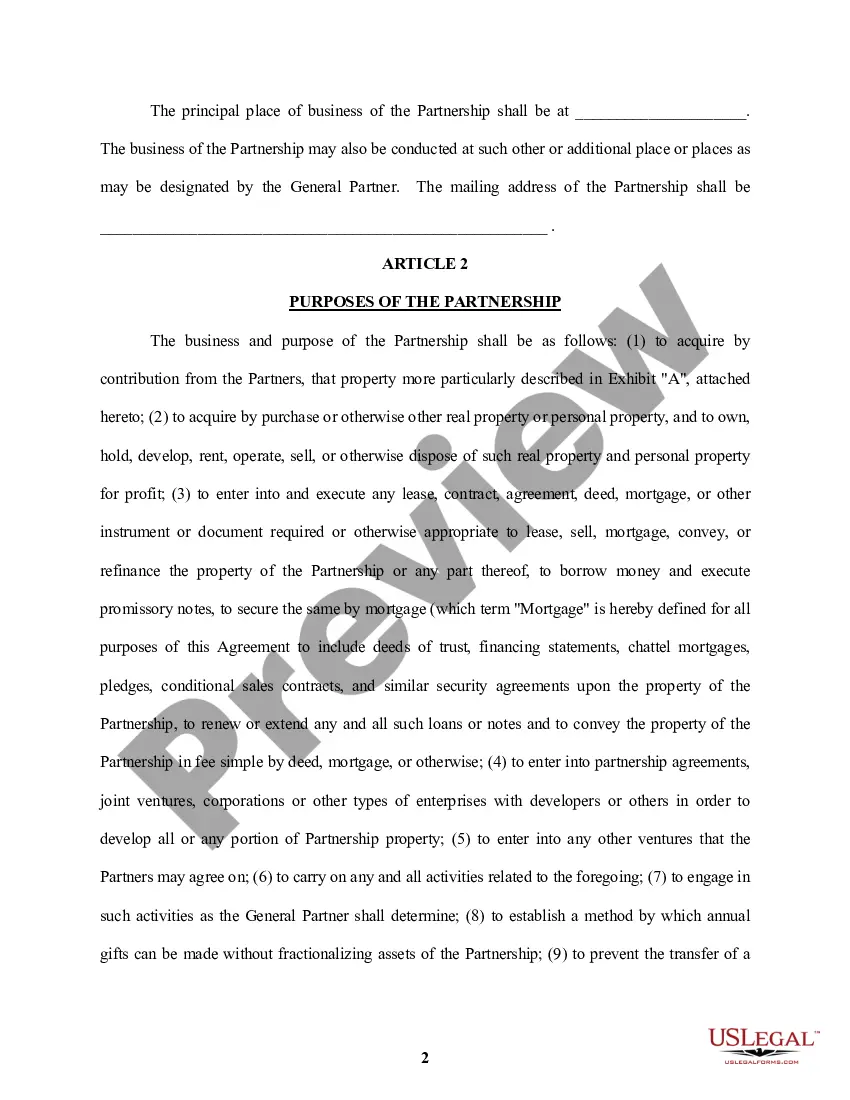

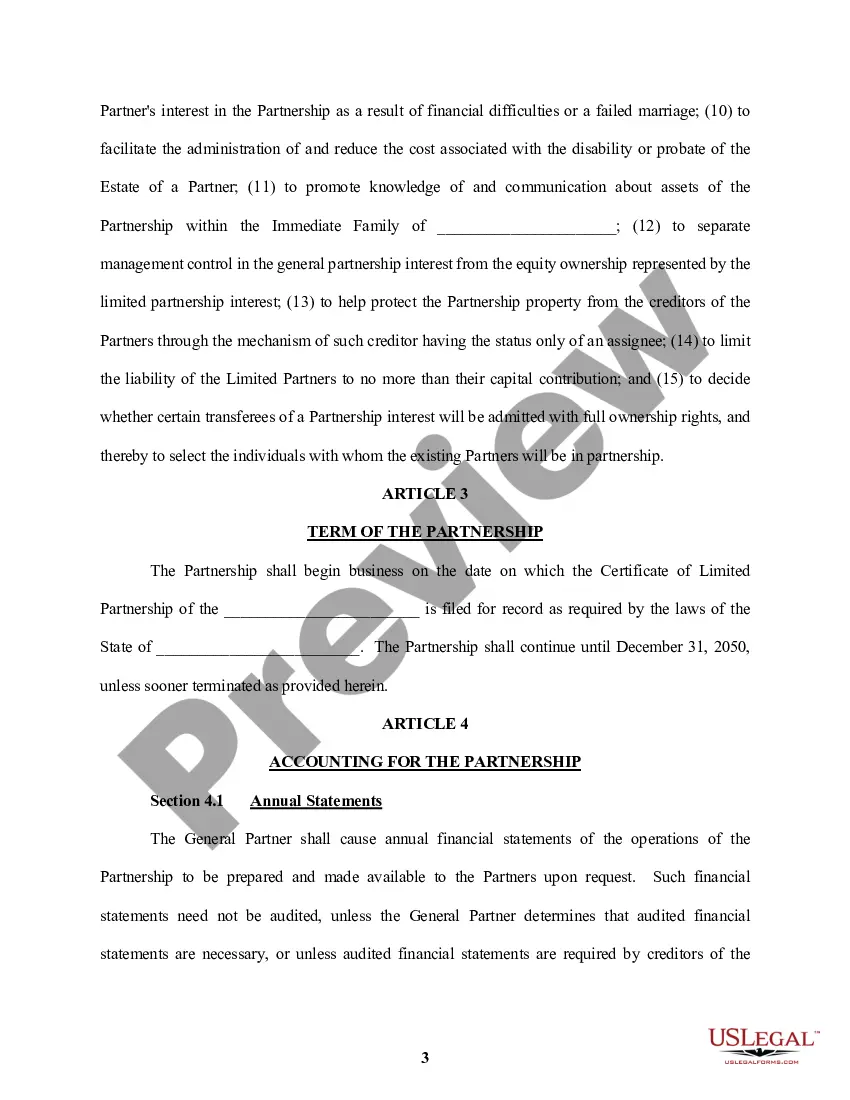

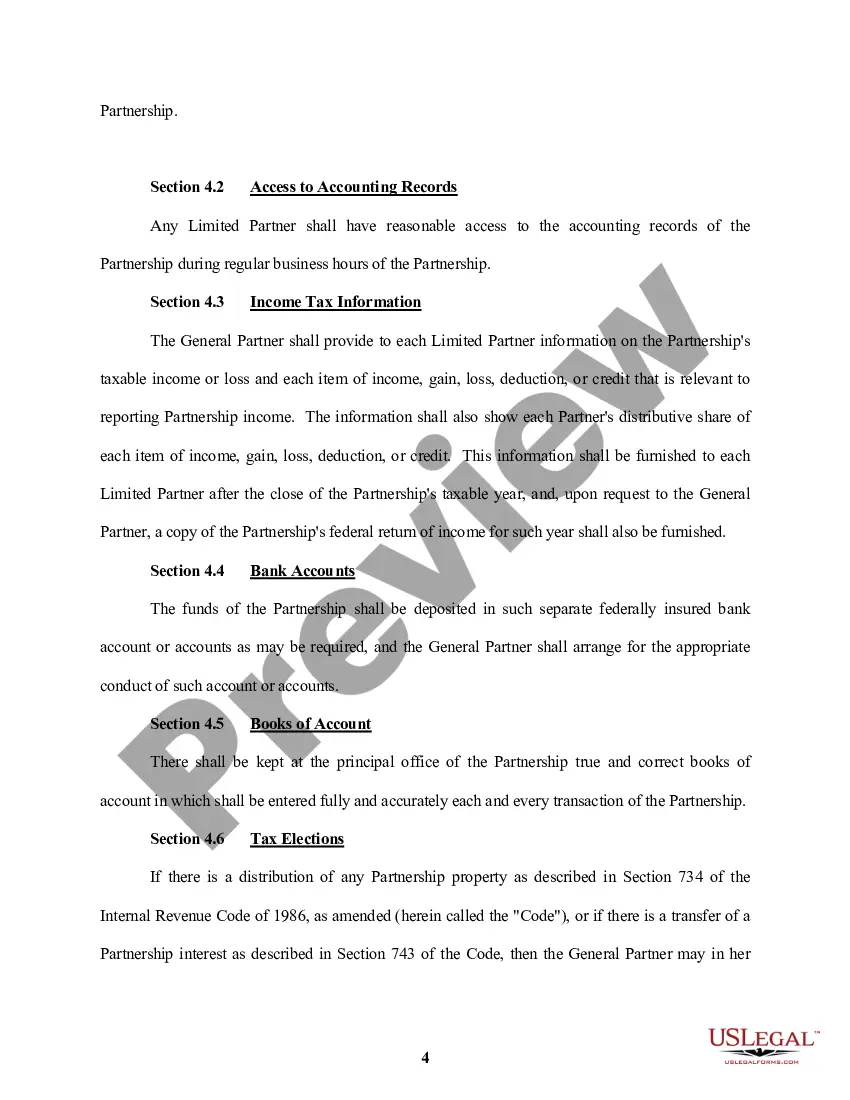

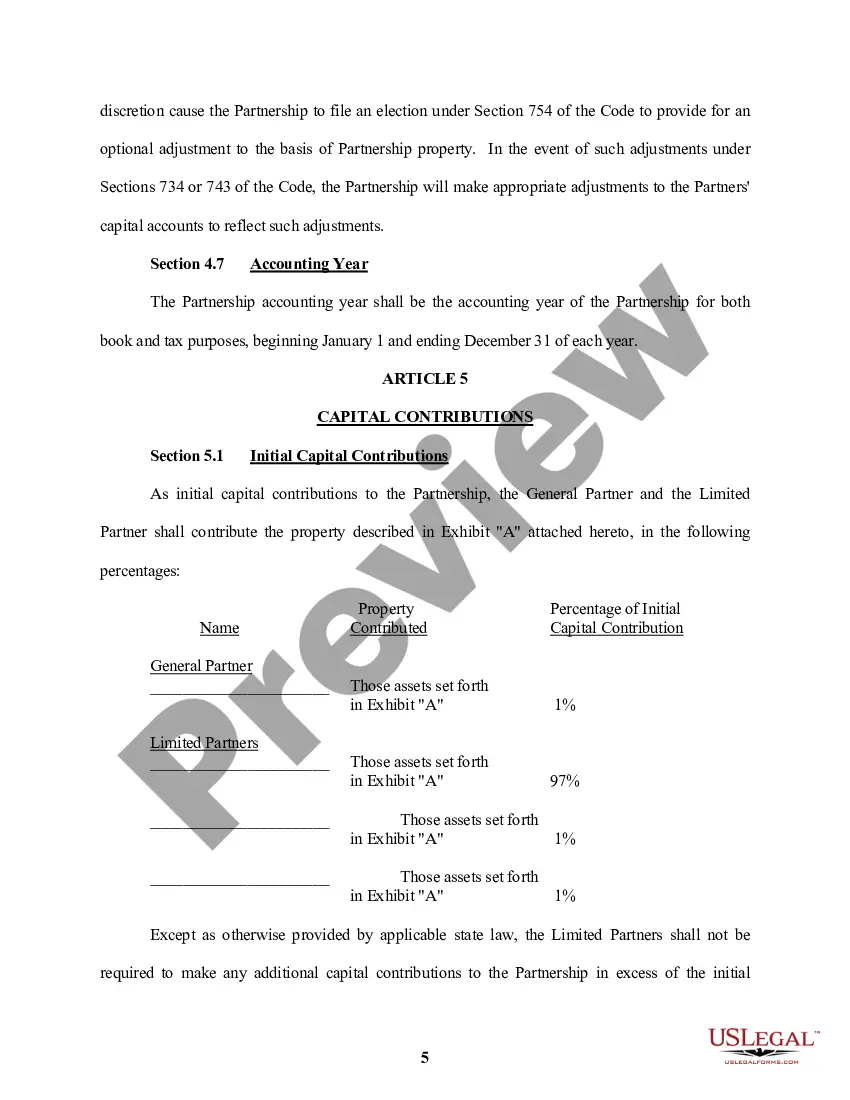

Maryland Family Limited Partnership Agreement and Certificate are legal documents used to establish a family limited partnership (FLP) in the state of Maryland. An FLP is a type of partnership that allows for the transfer of wealth and assets within a family while providing certain tax advantages and asset protection. The Maryland Family Limited Partnership Agreement sets out the terms and conditions under which the FLP will operate. It contains provisions regarding the management and control of the partnership, the rights and obligations of the partners, the distribution of profits and losses, and the transfer of partnership interests. The agreement also outlines the rules for adding or removing partners, as well as the procedures for dissolving the FLP. The Maryland Family Limited Partnership Certificate is a document filed with the Maryland Secretary of State's office to officially register the FLP. This certificate typically includes the name of the FLP, the names and addresses of the general and limited partners, the principal place of business, and other relevant details required by the state. In Maryland, there are no specific types of FLP agreements or certificates based on the family relationship. However, there may be different variations of the FLP agreement based on the specific needs and objectives of each family. Some common types of FLP agreements include non-taxable Alps, which focus on asset protection and family governance, and tax-advantaged Alps, designed to minimize estate taxes and facilitate estate planning. Keywords: Maryland Family Limited Partnership Agreement, Maryland Family Limited Partnership Certificate, family limited partnership, FLP, transfer of wealth, tax advantages, asset protection, management and control, partnership interests, adding or removing partners, dissolving the FLP, Maryland Secretary of State, family relationship, non-taxable FLP, tax-advantaged FLP, estate taxes, estate planning.

Maryland Family Limited Partnership Agreement and Certificate

Description

How to fill out Maryland Family Limited Partnership Agreement And Certificate?

Finding the right legitimate papers web template could be a have a problem. Needless to say, there are a lot of templates accessible on the Internet, but how will you obtain the legitimate form you want? Use the US Legal Forms website. The support provides a large number of templates, like the Maryland Family Limited Partnership Agreement and Certificate, which can be used for enterprise and private demands. All the varieties are checked by specialists and meet state and federal needs.

When you are already registered, log in for your profile and then click the Download button to get the Maryland Family Limited Partnership Agreement and Certificate. Use your profile to look through the legitimate varieties you have ordered in the past. Proceed to the My Forms tab of your own profile and get one more duplicate of the papers you want.

When you are a brand new consumer of US Legal Forms, listed below are basic instructions that you should stick to:

- Very first, make sure you have chosen the right form to your city/area. You can look over the form making use of the Preview button and look at the form description to guarantee this is the right one for you.

- In case the form fails to meet your requirements, make use of the Seach industry to find the right form.

- When you are positive that the form would work, select the Buy now button to get the form.

- Select the rates prepare you would like and enter in the essential information. Make your profile and pay money for the order with your PayPal profile or bank card.

- Select the submit formatting and download the legitimate papers web template for your device.

- Full, change and print out and signal the attained Maryland Family Limited Partnership Agreement and Certificate.

US Legal Forms is definitely the most significant library of legitimate varieties in which you can see a variety of papers templates. Use the service to download skillfully-manufactured documents that stick to state needs.