Maryland Cooperative Loan Recognition Agreement

Description

How to fill out Cooperative Loan Recognition Agreement?

Discovering the right lawful record template can be a struggle. Naturally, there are a variety of themes available online, but how can you get the lawful form you require? Use the US Legal Forms site. The support offers a large number of themes, such as the Maryland Cooperative Loan Recognition Agreement, which can be used for enterprise and personal demands. Each of the forms are inspected by experts and fulfill federal and state specifications.

Should you be previously registered, log in to the bank account and then click the Obtain switch to find the Maryland Cooperative Loan Recognition Agreement. Make use of your bank account to check with the lawful forms you possess acquired previously. Visit the My Forms tab of your respective bank account and obtain yet another backup of your record you require.

Should you be a fresh customer of US Legal Forms, listed here are basic instructions that you should follow:

- Initially, make certain you have selected the appropriate form for the city/area. You can look through the form making use of the Preview switch and look at the form explanation to make certain it will be the right one for you.

- In case the form does not fulfill your needs, utilize the Seach industry to obtain the proper form.

- When you are positive that the form is acceptable, go through the Acquire now switch to find the form.

- Pick the costs program you want and enter the essential information. Create your bank account and pay money for the transaction with your PayPal bank account or credit card.

- Choose the document formatting and down load the lawful record template to the device.

- Complete, modify and print out and signal the received Maryland Cooperative Loan Recognition Agreement.

US Legal Forms is definitely the largest catalogue of lawful forms where you can discover different record themes. Use the service to down load professionally-made files that follow express specifications.

Form popularity

FAQ

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace. It will make clear whether a particular union has sole negotiating rights for a bargaining group, or whether the employer recognises two or more unions jointly.

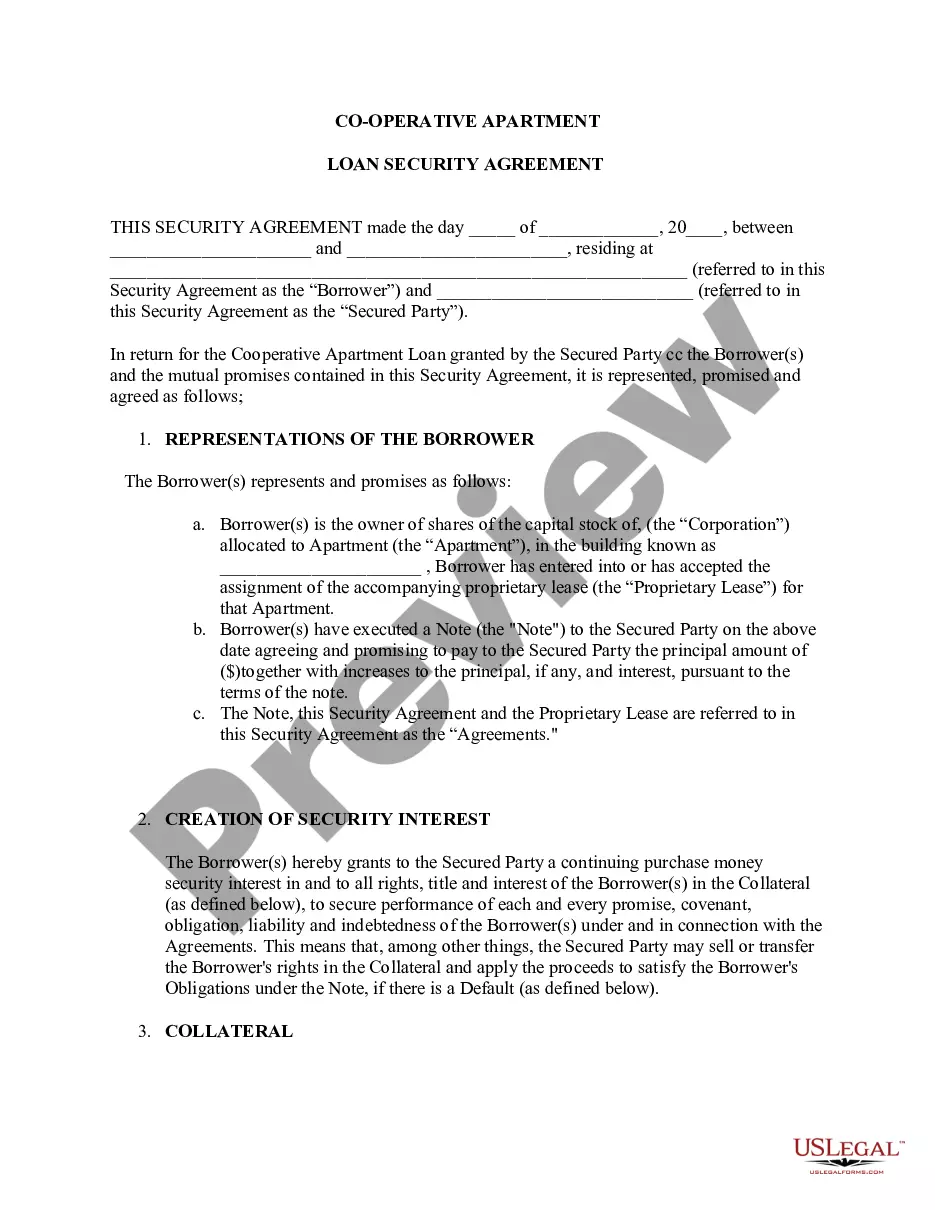

The owner of a co-op does not own his or her unit. The co-op is a corporation, complete with a corporate board of directors, and each resident is a ?shareholder.? Co-op buyers do not sign a deed. Instead, they purchases shares of the corporation, shares that include a lease granting use of a specific unit.

A cooperative corporation (or simply, a "cooperative") is a special form of corporation that places ownership and/or control of the corporation in the hands of the employees or patrons of the corporation.

The documents that show ownership in a cooperative are shares of stock in the cooperative corporation and a proprietary lease. An ownership interest that can be an estate interest or a right of use is. Time-share.

The stock, shares, membership certificates, or other contractual agreement evidencing ownership. The original Recognition Agreement, and, if applicable, the original assignment of the Recognition Agreement to the lender.

Co-op Ownership and Control The people who benefit from the products or services of a cooperative business own the cooperative business. In the case of a grocery co-op, the people who shop at the store are owner-members.

Recognition Agreement means, with respect to a Cooperative Mortgage Loan, an agreement executed by a Cooperative Corporation which, among other things, acknowledges the lien of the Mortgage on the Mortgaged Property in question.

More specifically, a recognition agreement is a contract between a subtenant and a prime landlord under which the prime landlord agrees to recognize the subtenant and the sublease if the tenant/sublandlord defaults under the prime lease and the prime landlord terminates the prime lease.

A recognition agreement is a legal document that allows parties to recognize each other's interests in an agreement.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace.