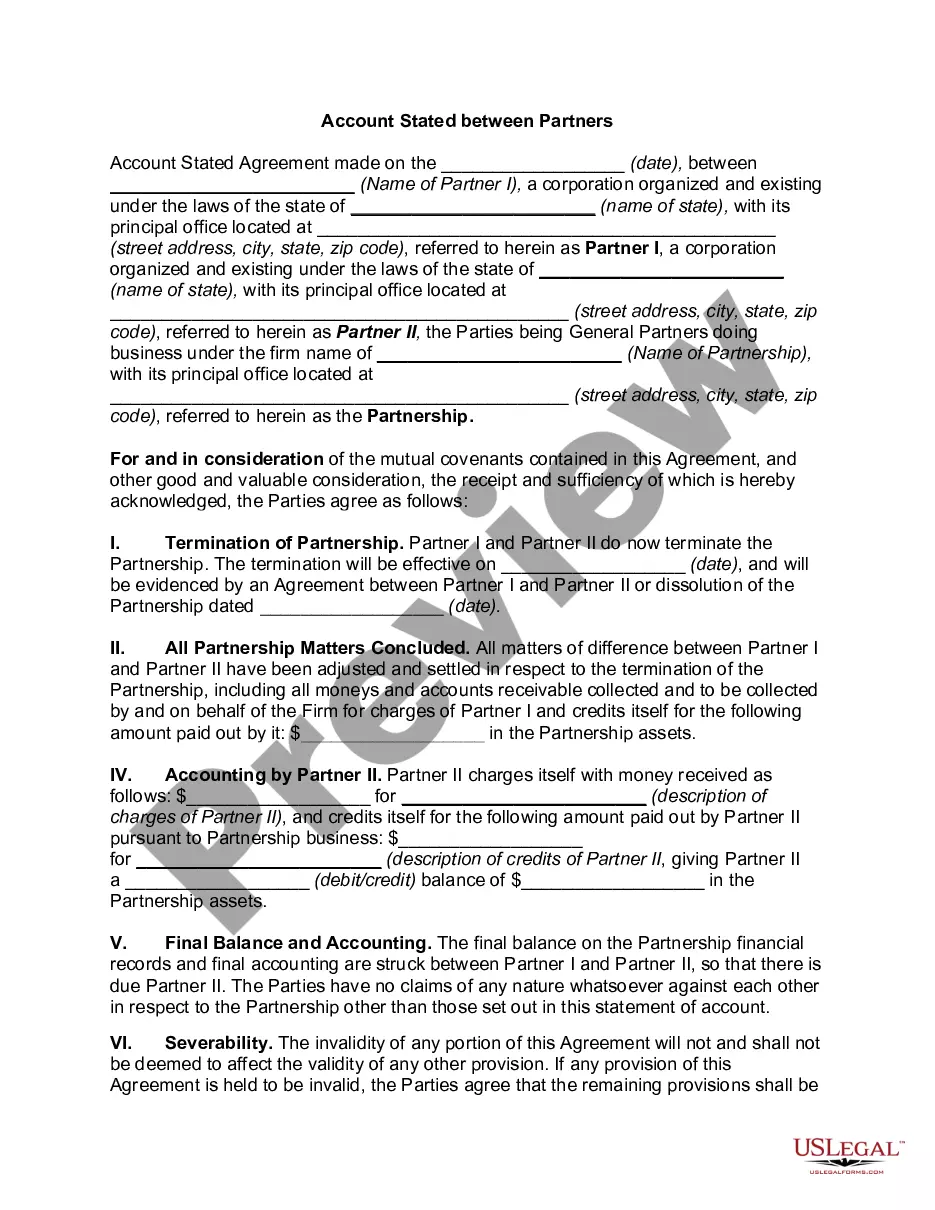

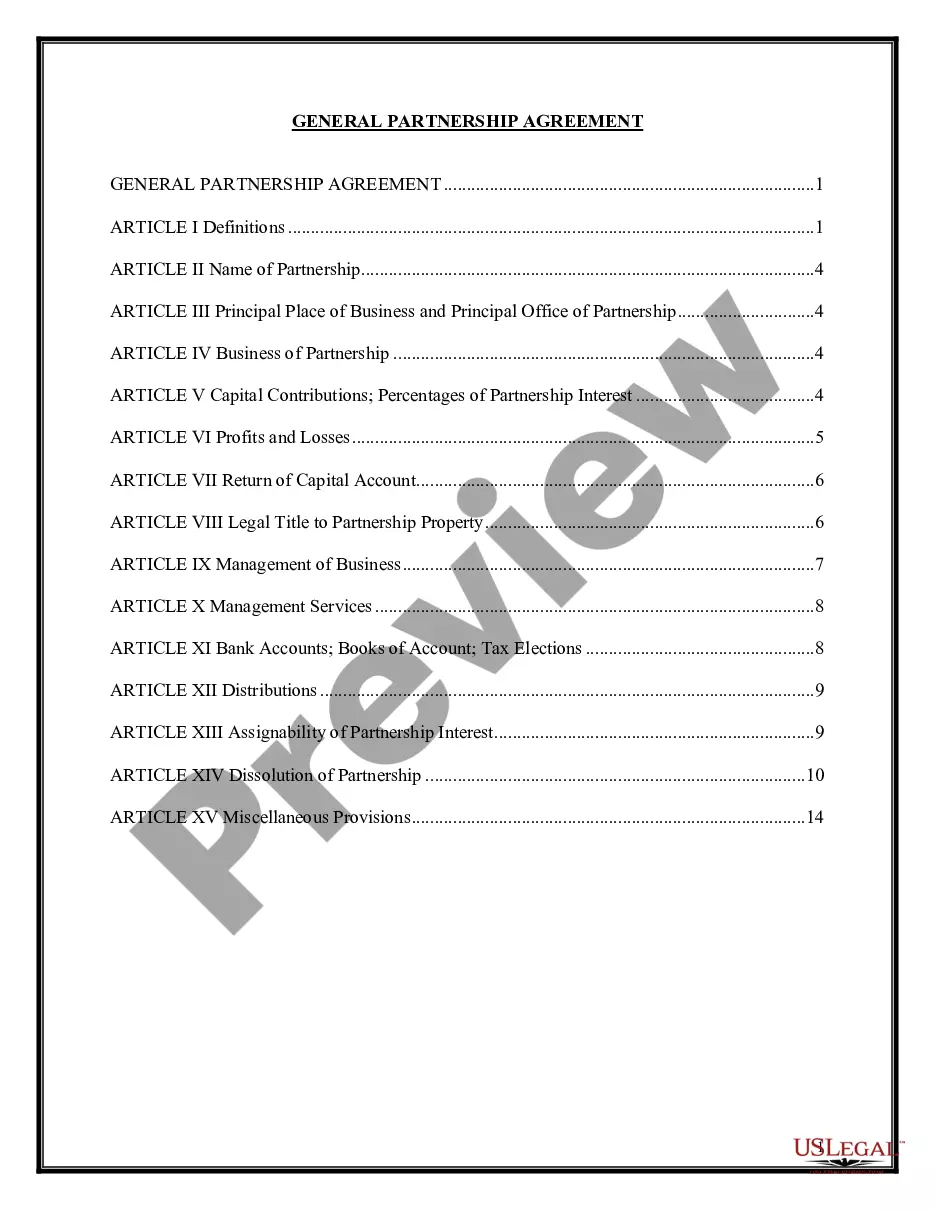

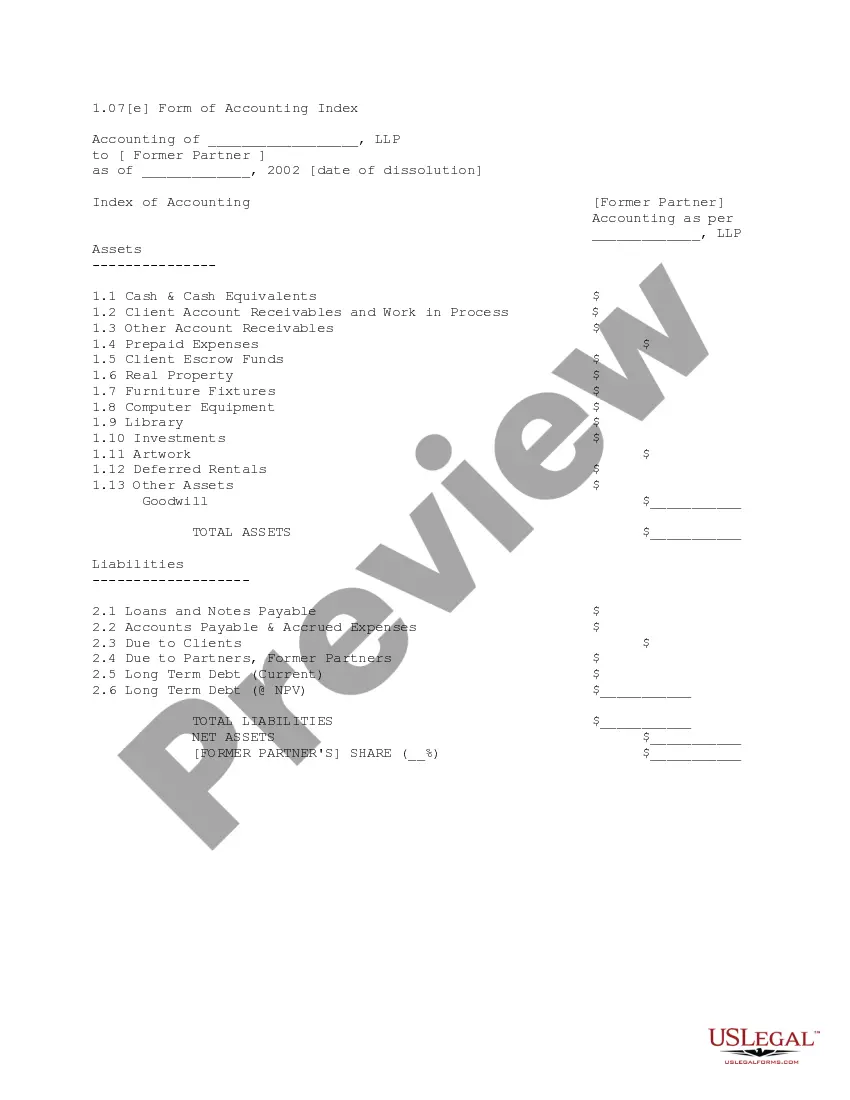

Maryland Account Stated Between Partners and Termination of Partnership

Description

How to fill out Account Stated Between Partners And Termination Of Partnership?

US Legal Forms - among the most significant libraries of authorized types in the States - delivers a variety of authorized papers web templates you may download or printing. Using the site, you can find thousands of types for company and specific reasons, categorized by classes, suggests, or key phrases.You can get the most up-to-date types of types such as the Maryland Account Stated Between Partners and Termination of Partnership in seconds.

If you have a membership, log in and download Maryland Account Stated Between Partners and Termination of Partnership through the US Legal Forms catalogue. The Acquire key will appear on every single form you perspective. You gain access to all previously downloaded types in the My Forms tab of your respective accounts.

If you want to use US Legal Forms the very first time, here are easy recommendations to get you started:

- Be sure to have picked out the proper form for the metropolis/county. Click the Review key to check the form`s content material. Browse the form explanation to actually have chosen the correct form.

- In case the form does not match your specifications, use the Lookup discipline near the top of the display screen to obtain the the one that does.

- When you are content with the form, verify your decision by clicking the Buy now key. Then, select the costs program you like and supply your qualifications to sign up for an accounts.

- Approach the transaction. Use your Visa or Mastercard or PayPal accounts to accomplish the transaction.

- Find the structure and download the form on your own device.

- Make modifications. Fill up, edit and printing and indication the downloaded Maryland Account Stated Between Partners and Termination of Partnership.

Every single format you included in your account does not have an expiry day which is your own permanently. So, if you would like download or printing one more version, just proceed to the My Forms section and then click in the form you want.

Gain access to the Maryland Account Stated Between Partners and Termination of Partnership with US Legal Forms, one of the most extensive catalogue of authorized papers web templates. Use thousands of expert and state-particular web templates that meet your company or specific requires and specifications.

Form popularity

FAQ

Comptroller of Maryland Payment Processing PO Box 8888 Annapolis, MD 21401-8888 To make an online payment, scan this QR code and follow instructions. A T T ACH CHECK OR MONEY ORDER HERE WITH ONE ST APLE. line of your Forms 502 and 505, Estimated Tax Payments and Extension Payments.

MD fiduciary returns will be available for e-file as of the 2022.03040 release. This is new for 2022, prior years are not e-fileable.

Comptroller of Maryland Payment Processing PO Box 8888 Annapolis, MD 21401-8888 To make an online payment, scan this QR code and follow instructions. A T T ACH CHECK OR MONEY ORDER HERE WITH ONE ST APLE. line of your Forms 502 and 505, Estimated Tax Payments and Extension Payments.

Description:You cannot eFile a MD Tax Amendment anywhere, except mail it in. This Form can be used to file a Tax Amendment, and Nonresident Income Tax Calculation. Description:Step 1: Download, Complete Form 502X (residents), or 505X and 505NR (nonresidents and part-year residents) for the appropriate Tax Year below.

You can call us at 800-492-5909 or 410-625-5555. online. This is the fastest and most secure method to update your Maryland state tax withholding. You can log into your account here: .

To terminate a Maryland Limited Liability Company (?LLC?) "Articles of Cancellation" must be submitted to: Department of Assessments and Taxation, Charter Legal Department, 301 W. Preston Street, Room 801, Baltimore, MD 21201.

To close your withholding account, please call 410-260-7980 or 1-800-638-2937, Monday ? Friday, am to pm. You can also close your withholding account by completing Form MW506FR, or by completing and resubmitting the Final Report Form in your withholding coupon booklet.

The Maryland Form 511 An Electing PTE Income Tax Return must be filed electronically if the pass-through entity has generated a business tax credit from Form 500CR or a Heritage Structure Rehabilitation Tax Credit from Form 502S to pass on to its members. taxhelp@marylandtaxes.gov.