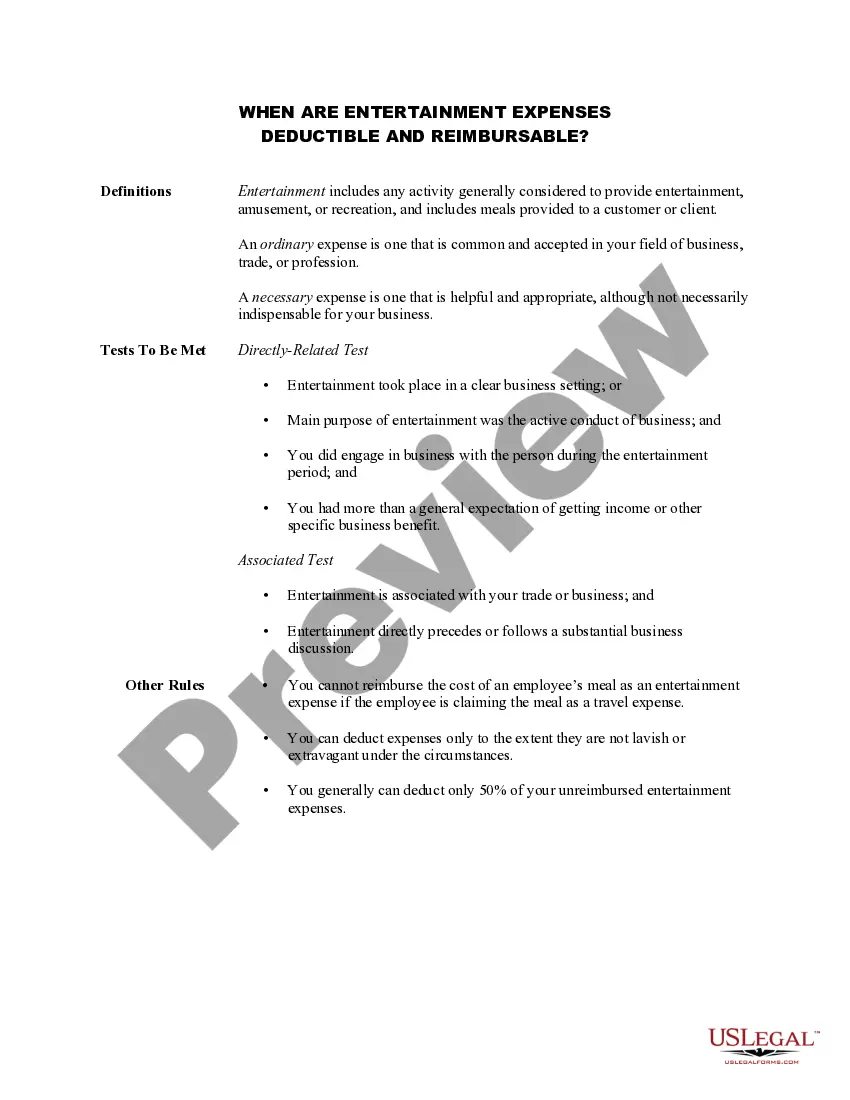

Maryland Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: A Comprehensive Guide Introduction: In this Maryland Information Sheet, we will delve into the various aspects of reducibility and reimbursement of entertainment expenses. This guide will explore the specific rules and regulations enforced by the state of Maryland, providing taxpayers with a clear understanding of when entertainment expenses may be deductible and reimbursable. We will highlight key keywords and cover any additional types or subtopics related to this subject. Keywords: Maryland, Information Sheet, Entertainment Expenses, Deductible, Reimbursable. Section 1: Understanding Entertainment Expenses: 1.1 Definition: This section will define entertainment expenses, covering their scope and various forms like meals, entertainment events, business-related networking activities, etc. 1.2 Eligibility for Deduction: Key requirements and criteria that must be met for entertainment expenses to be considered deductible will be discussed. 1.3 Records and Documentation: A thorough explanation of the documentation necessary to claim entertainment expenses as deductions, including receipts, invoices, and other supporting evidence. Section 2: Reducibility of Entertainment Expenses in Maryland: 2.1 Maryland Tax Laws: An overview of the specific tax laws and regulations relevant to entertainment expense deductions in Maryland. 2.2 Business Purpose: Discussing the essential requirement of establishing a clear business purpose to justify the reducibility of entertainment expenses. 2.3 Ordinary and Necessary Test: Elaborating on the "ordinary and necessary" test, explaining how entertainment expenses must meet these criteria to be considered deductible. Section 3: Reimbursement of Entertainment Expenses: 3.1 Employer Reimbursement Policies: An exploration of company policies regarding the reimbursement of entertainment expenses. 3.2 Reporting Requirements: Clarifying the reporting obligations for employees seeking reimbursement for entertainment expenses. 3.3 Tax Implications: Discussing the potential tax consequences for both employees and employers when reimbursing entertainment expenses. Section 4: Different Types of Entertainment Expenses: 4.1 Meals: Detailing the specific rules and limitations surrounding the reducibility and reimbursability of meals consumed for business purposes. 4.2 Sporting Events: Exploring the reducibility and reimbursability of expenses related to attending sporting events for business purposes. 4.3 Client Entertainment: Highlighting the requirements and conditions for deducting and reimbursing expenses incurred while entertaining clients. 4.4 Travel and Accommodation: Addressing the nuances related to the reducibility and reimbursability of entertainment expenses associated with business travel and accommodation. Conclusion: This Maryland Information Sheet provides a comprehensive understanding of when entertainment expenses may be considered deductible and reimbursable. By exploring the specific rules and regulations enforced by Maryland's tax laws, taxpayers can confidently navigate the complexities of claiming deductions and seeking reimbursement for their entertainment-related expenditures. Remember to consult with a qualified tax professional for personalized advice regarding your specific situation. Types of Maryland Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: 1. Basic Maryland Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: This covers the fundamental principles and guidelines surrounding entertainment expense deductions and reimbursements in Maryland. 2. Advanced Maryland Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: This provides a more in-depth analysis of complex scenarios and exceptional cases related to entertainment expense reducibility and reimbursement in Maryland. Note: The actual types of Maryland Information Sheets may vary based on targeted audiences, levels of detail, and specific subjects.

Maryland Information Sheet - When are Entertainment Expenses Deductible and Reimbursable

Description

How to fill out Maryland Information Sheet - When Are Entertainment Expenses Deductible And Reimbursable?

Choosing the best lawful document template might be a struggle. Obviously, there are a variety of templates accessible on the Internet, but how would you get the lawful develop you need? Use the US Legal Forms internet site. The services delivers thousands of templates, including the Maryland Information Sheet - When are Entertainment Expenses Deductible and Reimbursable, which can be used for company and personal requires. All the varieties are inspected by experts and satisfy federal and state requirements.

If you are already authorized, log in to your profile and then click the Acquire key to find the Maryland Information Sheet - When are Entertainment Expenses Deductible and Reimbursable. Use your profile to look through the lawful varieties you may have bought in the past. Proceed to the My Forms tab of your profile and have one more duplicate from the document you need.

If you are a whole new consumer of US Legal Forms, here are straightforward directions that you should stick to:

- Initial, be sure you have chosen the appropriate develop for your personal metropolis/county. It is possible to look through the form making use of the Review key and study the form description to ensure this is basically the best for you.

- If the develop will not satisfy your preferences, utilize the Seach discipline to discover the right develop.

- Once you are positive that the form is acceptable, click on the Acquire now key to find the develop.

- Select the prices strategy you need and type in the necessary information and facts. Create your profile and pay for the transaction with your PayPal profile or charge card.

- Pick the submit structure and acquire the lawful document template to your device.

- Total, revise and print out and sign the attained Maryland Information Sheet - When are Entertainment Expenses Deductible and Reimbursable.

US Legal Forms is definitely the biggest library of lawful varieties that you can see various document templates. Use the service to acquire appropriately-created paperwork that stick to state requirements.