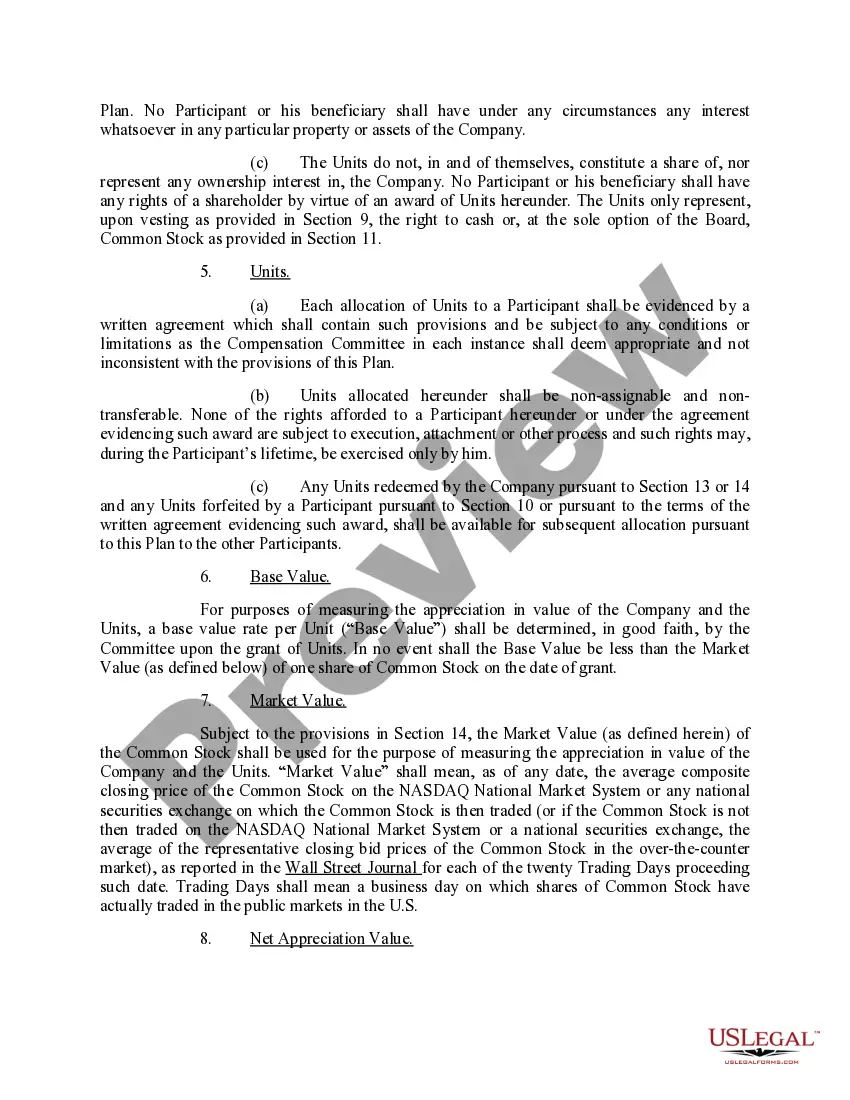

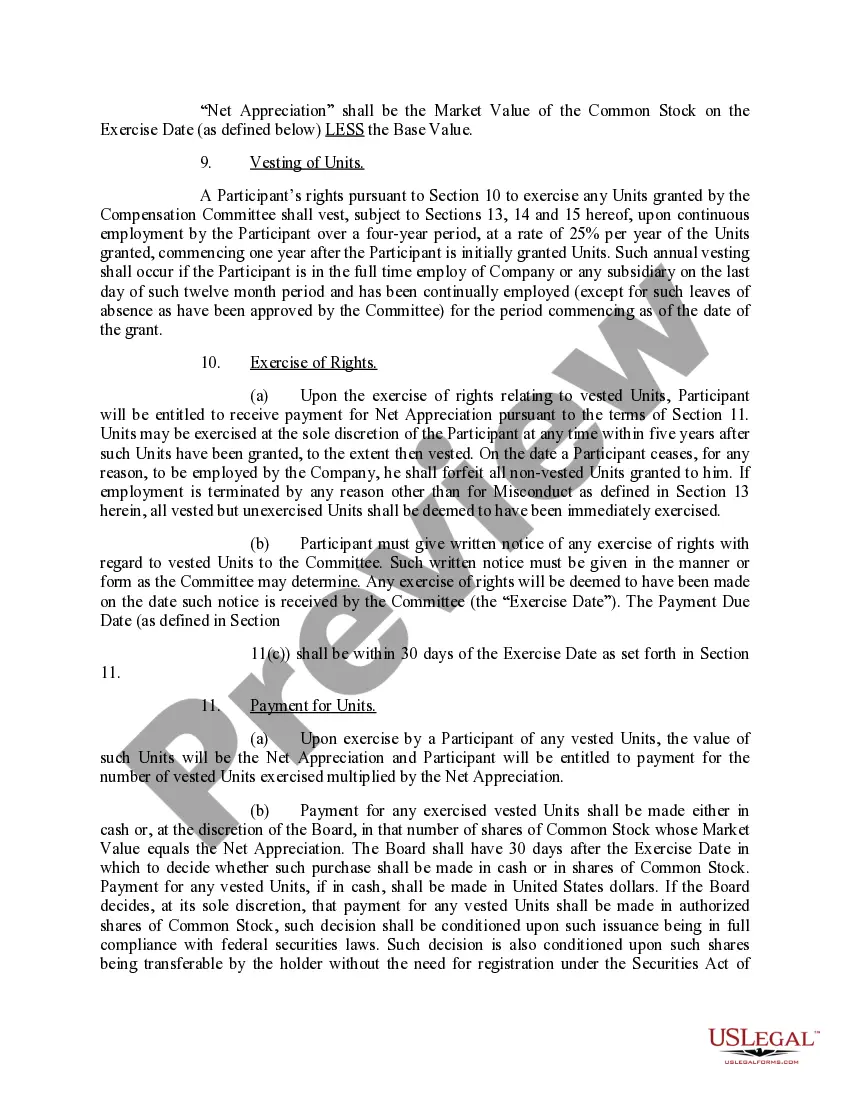

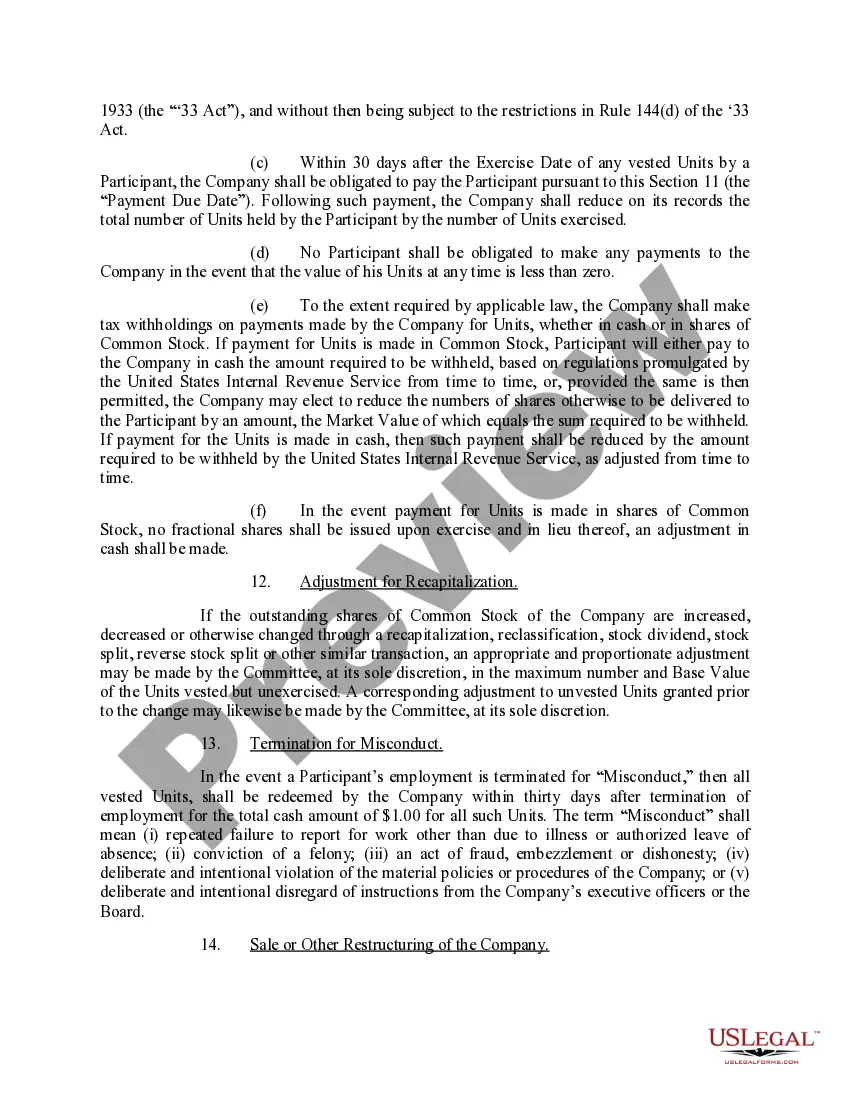

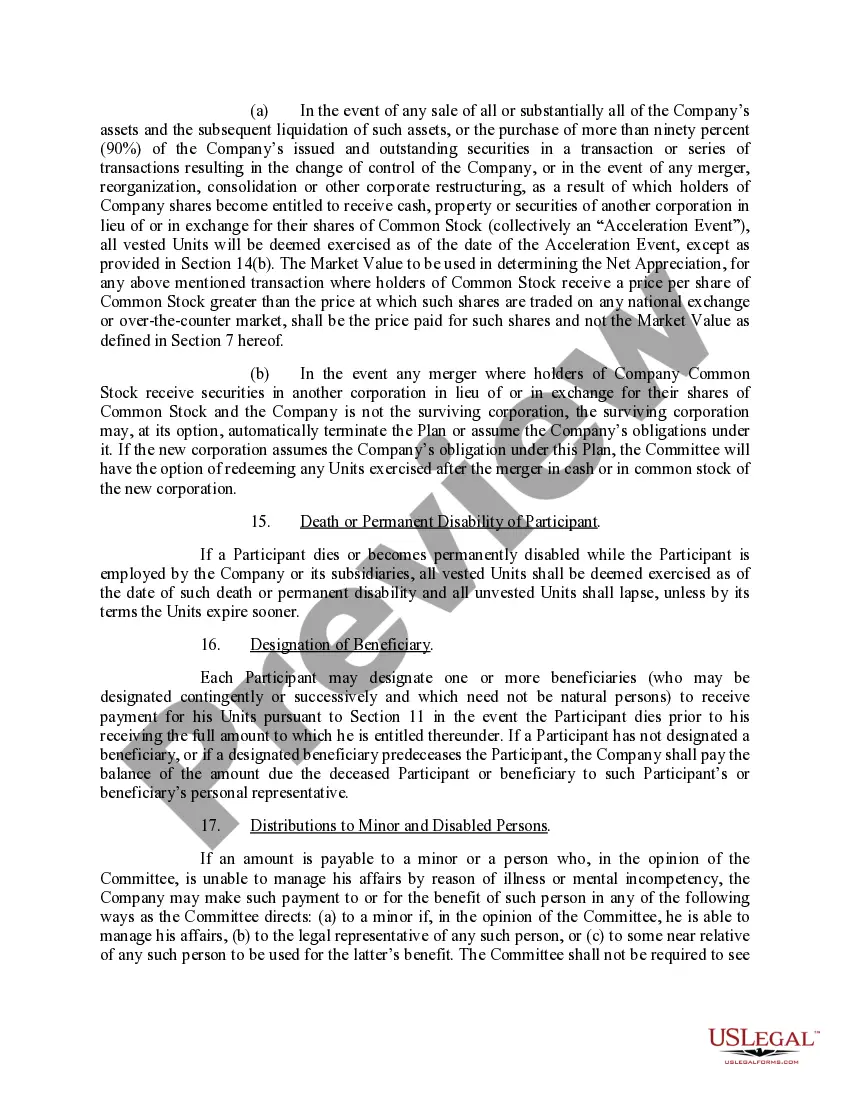

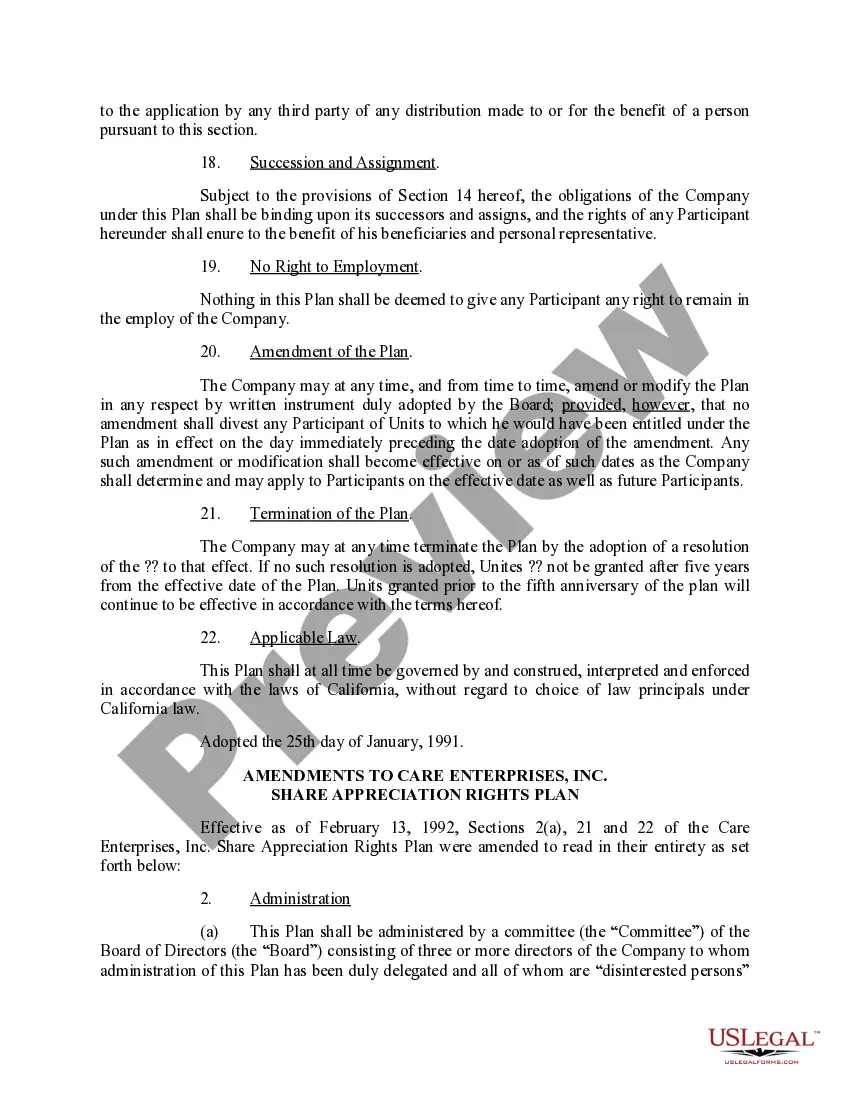

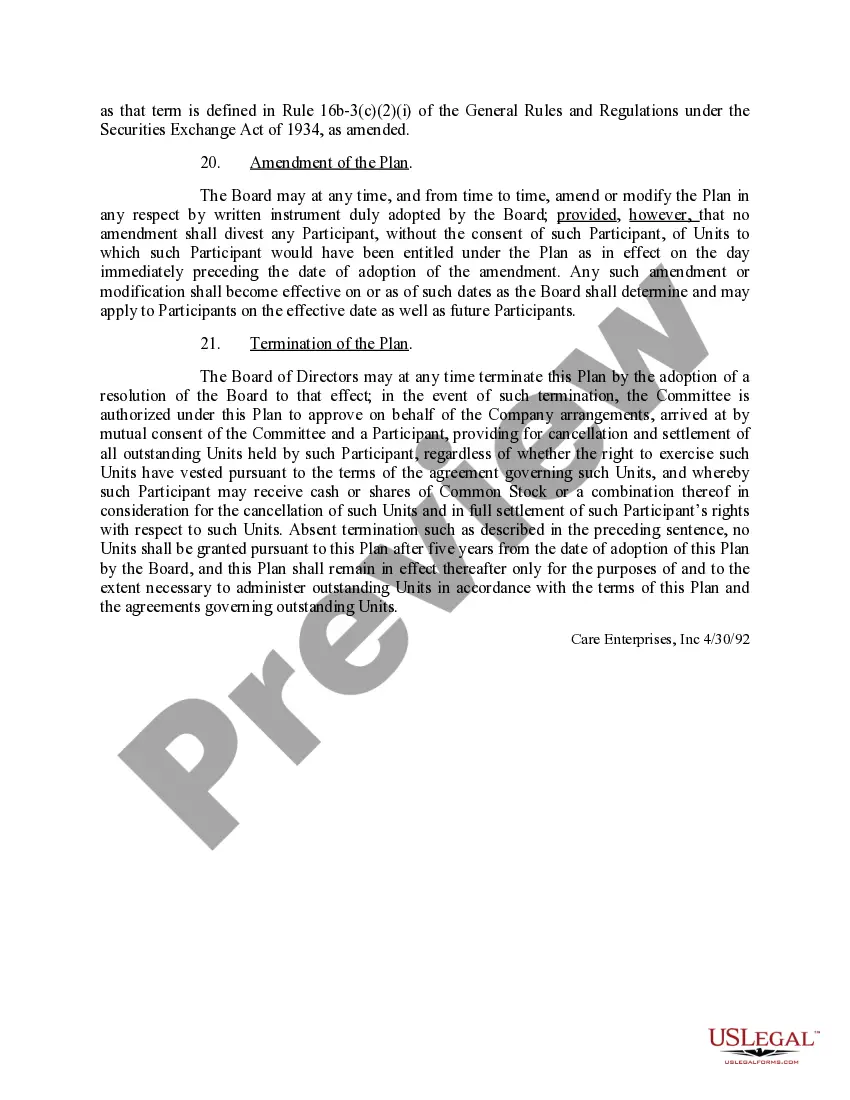

Maryland Share Appreciation Rights Plan with Amendment The Maryland Share Appreciation Rights (SAR) Plan with Amendment is a compensation incentive program offered by companies to their employees that is specific to the state of Maryland. This plan grants eligible employees the right to receive appreciation in the value of a specified number of company shares, similar to stock options but without the requirement to purchase the shares. Under the Maryland SAR Plan, employees are granted SARS, which represent the right to receive the difference between the fair market value of the company's shares on the date of exercise and the grant price of the SAR. This appreciation is usually paid out in cash or company shares, offering employees an opportunity to benefit from the company's growth without directly purchasing shares. The amendment to the Maryland SAR Plan involves making changes or modifications to the existing plan. These amendments can vary based on the company's requirements, industry regulations, or other factors. Common amendments may include altering the eligibility criteria for employees, adjusting the grant price, changing the vesting period, or modifying the payout method. Different types of Maryland Share Appreciation Rights Plans with amendments may exist, depending on the specific needs and preferences of each company. These can include: 1. General Maryland SAR Plan: This plan is designed to compensate a broad group of employees, typically offered to all eligible employees regardless of their position. 2. Executive Maryland SAR Plan: This plan is usually tailored for top-level executives and key management personnel within the organization, offering them a more significant number of SARS and additional benefits to attract and retain high-level talent. 3. Restricted Maryland SAR Plan: In this type of plan, the SARS are subject to certain restrictions or limitations, such as a predetermined vesting period or performance-based conditions that must be met before the SARS can be exercised. 4. Performance-Based Maryland SAR Plan: This plan links the SARS' exercise and payouts to the company's performance metrics, such as revenue growth, earnings per share, or other predetermined financial goals. 5. Rolling Maryland SAR Plan: This plan allows the company to issue new SARS periodically, providing ongoing opportunities for employees to participate and benefit from the company's performance. It is important to note that the specific terms and conditions of the Maryland Share Appreciation Rights Plan, including any amendments, may vary from company to company. Employees should carefully review their company's plan documents and consult with the appropriate legal and financial professionals for personalized advice and guidance.

Maryland Share Appreciation Rights Plan with amendment

Description

How to fill out Maryland Share Appreciation Rights Plan With Amendment?

If you wish to complete, down load, or print out legitimate papers themes, use US Legal Forms, the greatest selection of legitimate types, that can be found on the Internet. Take advantage of the site`s easy and practical search to obtain the papers you will need. Different themes for business and individual functions are categorized by groups and suggests, or keywords and phrases. Use US Legal Forms to obtain the Maryland Share Appreciation Rights Plan with amendment with a number of mouse clicks.

When you are currently a US Legal Forms buyer, log in for your bank account and click the Obtain key to get the Maryland Share Appreciation Rights Plan with amendment. Also you can gain access to types you formerly downloaded in the My Forms tab of your respective bank account.

If you work with US Legal Forms the very first time, refer to the instructions below:

- Step 1. Be sure you have selected the form to the correct area/country.

- Step 2. Make use of the Review method to look over the form`s content. Do not overlook to read the description.

- Step 3. When you are not satisfied together with the kind, take advantage of the Lookup field near the top of the display screen to discover other models of the legitimate kind design.

- Step 4. Upon having located the form you will need, click the Buy now key. Pick the pricing strategy you choose and add your qualifications to sign up on an bank account.

- Step 5. Method the purchase. You can use your Мisa or Ьastercard or PayPal bank account to perform the purchase.

- Step 6. Choose the structure of the legitimate kind and down load it in your system.

- Step 7. Complete, modify and print out or sign the Maryland Share Appreciation Rights Plan with amendment.

Every single legitimate papers design you acquire is your own forever. You might have acces to every single kind you downloaded inside your acccount. Select the My Forms segment and decide on a kind to print out or down load once again.

Contend and down load, and print out the Maryland Share Appreciation Rights Plan with amendment with US Legal Forms. There are many professional and status-certain types you may use to your business or individual requirements.