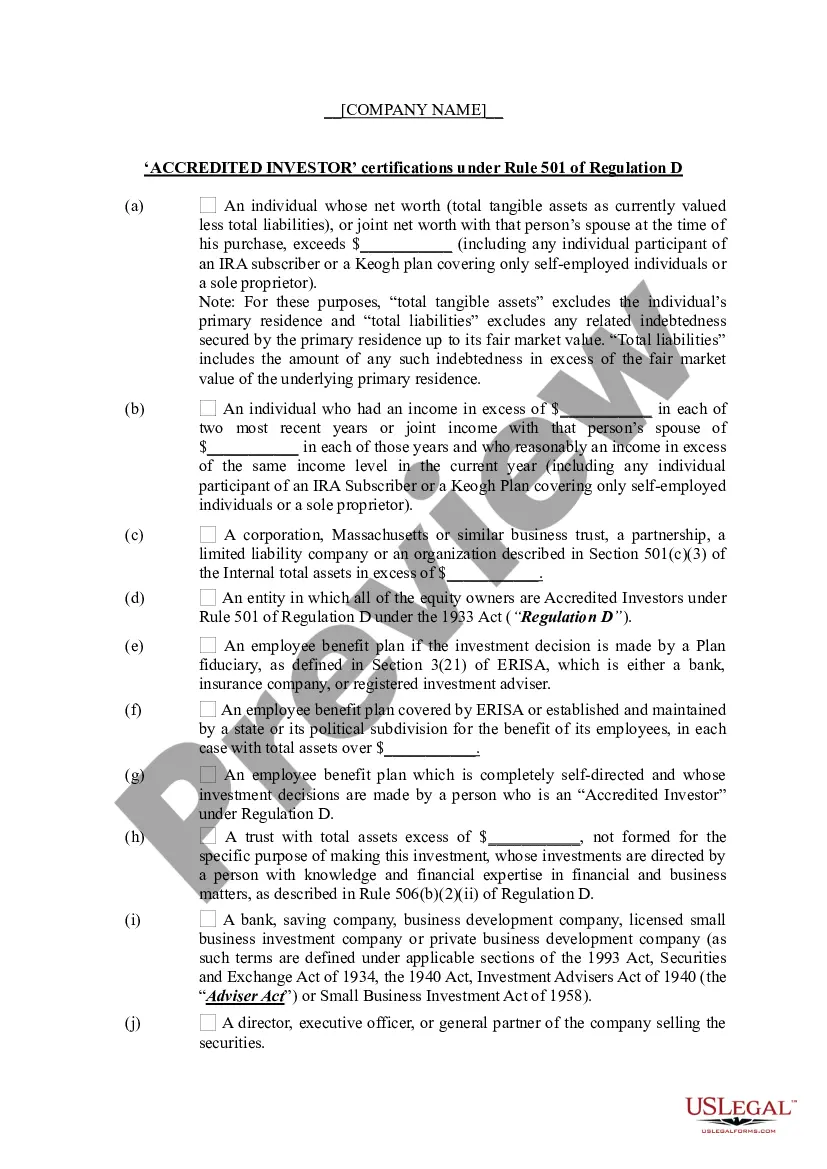

Maryland Information Checklist — Accredited Investor Certifications Under Rule 501 In Maryland, the state requires individuals or entities claiming to be accredited investors to fulfill certain criteria as specified under Rule 501 of the Securities and Exchange Commission (SEC). These requirements are designed to ensure that investors possess the necessary knowledge and financial capacity to participate in certain investment opportunities. Below is a detailed description of the Maryland Information Checklist for Accredited Investor Certifications under Rule 501, including various types of certifications that can be obtained. 1. Individual Certification: Individuals seeking to become accredited investors in Maryland must meet specific criteria outlined by the SEC. These criteria include having a net worth exceeding $1 million (excluding the value of a primary residence) or having an annual income of at least $200,000 (or $300,000 together with a spouse) for the past two years with a reasonable expectation of the same income level in the current year. Individuals may also qualify if they hold the Series 7, 65, or 82 licenses. 2. Corporate Entity Certification: Certain corporate entities can also qualify as accredited investors in Maryland. These entities must have a total assets value exceeding $5 million and be either a corporation, partnership, limited liability company, business trust, or other similar organization. Additionally, the entity's investment decisions must be made by a sophisticated person or a team of sophisticated persons with sufficient knowledge to evaluate the investment opportunity. 3. Trusts, Charitable Organizations, and Employee Benefit Plans Certification: Trusts, charitable organizations, and employee benefit plans may also qualify as accredited investors in Maryland under certain conditions. For example, a trust must have total assets exceeding $5 million and be not formed for the purpose of acquiring the security being offered. Charitable organizations must have total assets exceeding $5 million and either be exempt from taxation under Section 501(c)(3) of the Internal Revenue Code or be a state-registered investment company. Employee benefit plans, such as retirement plans, must have total assets exceeding $5 million or be self-directed with investment decisions made by an accredited investor. 4. Regulation D Certifications: Maryland recognizes the qualifications under SEC Regulation D, which provides certain exemptions from the securities' registration requirements. By meeting the accredited investor criteria defined in Rule 501, individuals or entities can benefit from these exemptions when participating in private placements, venture capital investments, or other non-public offerings. It is important for investors and entities in Maryland to carefully evaluate and fulfill the specific requirements relevant to their situation when seeking accredited investor certification under Rule 501. By doing so, they can gain access to a wider range of investment opportunities while maintaining compliance with Maryland securities regulations.

Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 of Regulation D

Description

How to fill out Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 Of Regulation D?

If you wish to comprehensive, down load, or produce legitimate record web templates, use US Legal Forms, the greatest collection of legitimate types, that can be found online. Use the site`s simple and easy hassle-free lookup to obtain the files you need. Numerous web templates for enterprise and specific functions are sorted by categories and says, or keywords. Use US Legal Forms to obtain the Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 of in just a handful of clicks.

When you are already a US Legal Forms client, log in in your accounts and then click the Down load button to find the Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 of. You may also gain access to types you in the past delivered electronically from the My Forms tab of the accounts.

If you use US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have chosen the shape for the correct city/nation.

- Step 2. Use the Preview solution to examine the form`s information. Never neglect to learn the description.

- Step 3. When you are unsatisfied together with the develop, make use of the Lookup area towards the top of the display to find other types of your legitimate develop design.

- Step 4. After you have identified the shape you need, click the Buy now button. Choose the pricing prepare you favor and add your credentials to sign up to have an accounts.

- Step 5. Method the financial transaction. You may use your credit card or PayPal accounts to accomplish the financial transaction.

- Step 6. Find the formatting of your legitimate develop and down load it in your product.

- Step 7. Comprehensive, change and produce or signal the Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 of.

Each legitimate record design you get is yours forever. You might have acces to each develop you delivered electronically in your acccount. Go through the My Forms section and decide on a develop to produce or down load once more.

Compete and down load, and produce the Maryland Information Checklist - Accredited Investor Certifications Under Rule 501 of with US Legal Forms. There are many expert and state-certain types you can use for your personal enterprise or specific requirements.