Maryland A Summary of Your Rights Under the Fair Credit Reporting Act

Description

How to fill out A Summary Of Your Rights Under The Fair Credit Reporting Act?

Have you been inside a position where you need paperwork for either business or personal purposes virtually every day? There are plenty of legitimate document themes accessible on the Internet, but locating kinds you can rely isn`t easy. US Legal Forms gives a huge number of type themes, like the Maryland A Summary of Your Rights Under the Fair Credit Reporting Act, which can be published to satisfy state and federal demands.

Should you be previously familiar with US Legal Forms website and possess a merchant account, simply log in. Next, you may download the Maryland A Summary of Your Rights Under the Fair Credit Reporting Act design.

Should you not offer an bank account and need to start using US Legal Forms, adopt these measures:

- Find the type you need and ensure it is to the correct city/area.

- Utilize the Review key to check the form.

- See the description to ensure that you have chosen the right type.

- In case the type isn`t what you are looking for, utilize the Research discipline to discover the type that fits your needs and demands.

- When you get the correct type, click on Get now.

- Opt for the costs strategy you want, submit the necessary information to create your money, and pay money for an order using your PayPal or Visa or Mastercard.

- Decide on a handy document structure and download your backup.

Discover all the document themes you may have purchased in the My Forms menus. You can aquire a additional backup of Maryland A Summary of Your Rights Under the Fair Credit Reporting Act whenever, if possible. Just click on the essential type to download or print the document design.

Use US Legal Forms, probably the most comprehensive variety of legitimate varieties, in order to save time as well as steer clear of faults. The services gives expertly made legitimate document themes that can be used for an array of purposes. Generate a merchant account on US Legal Forms and start creating your life easier.

Form popularity

FAQ

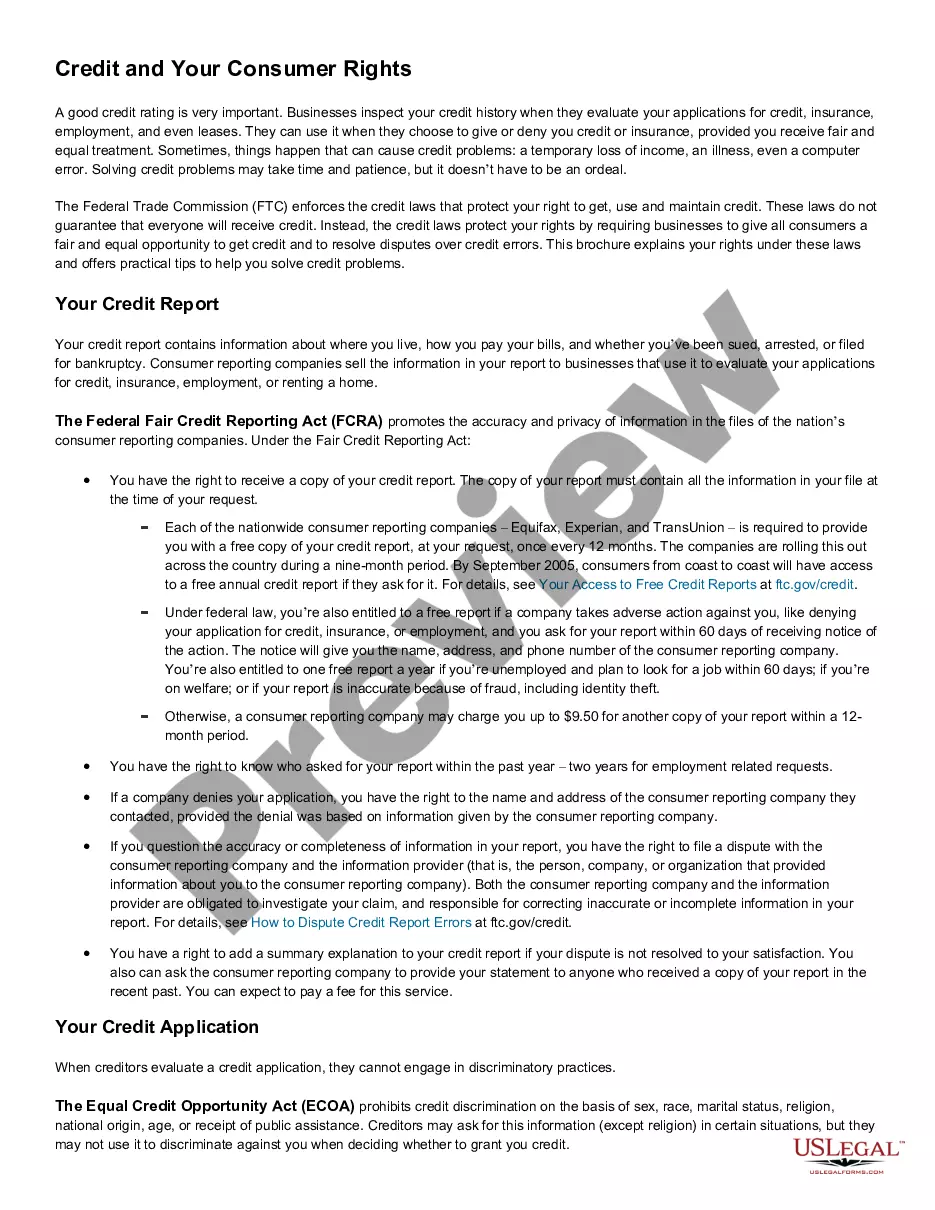

? It bears on a consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living. understanding-the-fcra.pdf - Jones Day Jones Day ? files ? fileattachment Jones Day ? files ? fileattachment PDF

Four Basic Steps to FCRA Compliance Step 1: Disclosure & Written Consent. Before requesting a consumer or investigative report, an employer must: ... Step 2: Certification To The Consumer Reporting Agency. ... Step 3: Provide Applicant With Pre-Adverse Action Documents. ... Step 4: Notify Applicant Of Adverse Action.

The Fair Credit Reporting Act (FCRA) is a federal law that regulates the collection of consumers' credit information and access to their credit reports. It was passed in 1970 to address the fairness, accuracy, and privacy of the personal information contained in the files of the credit reporting agencies. How the Fair Credit Reporting Act (FCRA) Protects Consumer ... Investopedia ? ... ? Building Credit Investopedia ? ... ? Building Credit

? You have the right to know what is in your file. information about you in the files of a consumer reporting agency (your ?file disclosure?). You will be required to provide proper identification, which may include your Social Security number. In many cases, the disclosure will be free.

Candidate Rights Under FCRA The candidate may dispute the information provided by the consumer reporting agency. This action allows for the correction of misreported, outdated, or otherwise incorrect data.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

The Fair Credit Reporting Act (FCRA) , 15 U.S.C. § 1681 et seq., governs access to consumer credit report records and promotes accuracy, fairness, and the privacy of personal information assembled by Credit Reporting Agencies (CRAs).

? You have the right to know what is in your file. In addition, all consumers are entitled to one free disclosure every 12 months upon request from each nationwide credit bureau and from nationwide specialty consumer reporting agencies. See .consumerfinance.gov/learnmore for additional information.

Under the Fair Credit Reporting Act, you have a right to: You must have proper identification. You have a right to a free copy of your credit report within 15 days of your request. Protected Access ? The act limits access to your file to those with a valid need. Fair Credit Reporting Act - Debt.org Debt.org ? credit ? your-consumer-rights Debt.org ? credit ? your-consumer-rights

The Fair Credit Reporting Act (FCRA) , 15 U.S.C. § 1681 et seq., governs access to consumer credit report records and promotes accuracy, fairness, and the privacy of personal information assembled by Credit Reporting Agencies (CRAs). Fair Credit Reporting Act - Bureau of Justice Assistance Bureau of Justice Assistance (.gov) ? program ? authorities ? statutes Bureau of Justice Assistance (.gov) ? program ? authorities ? statutes