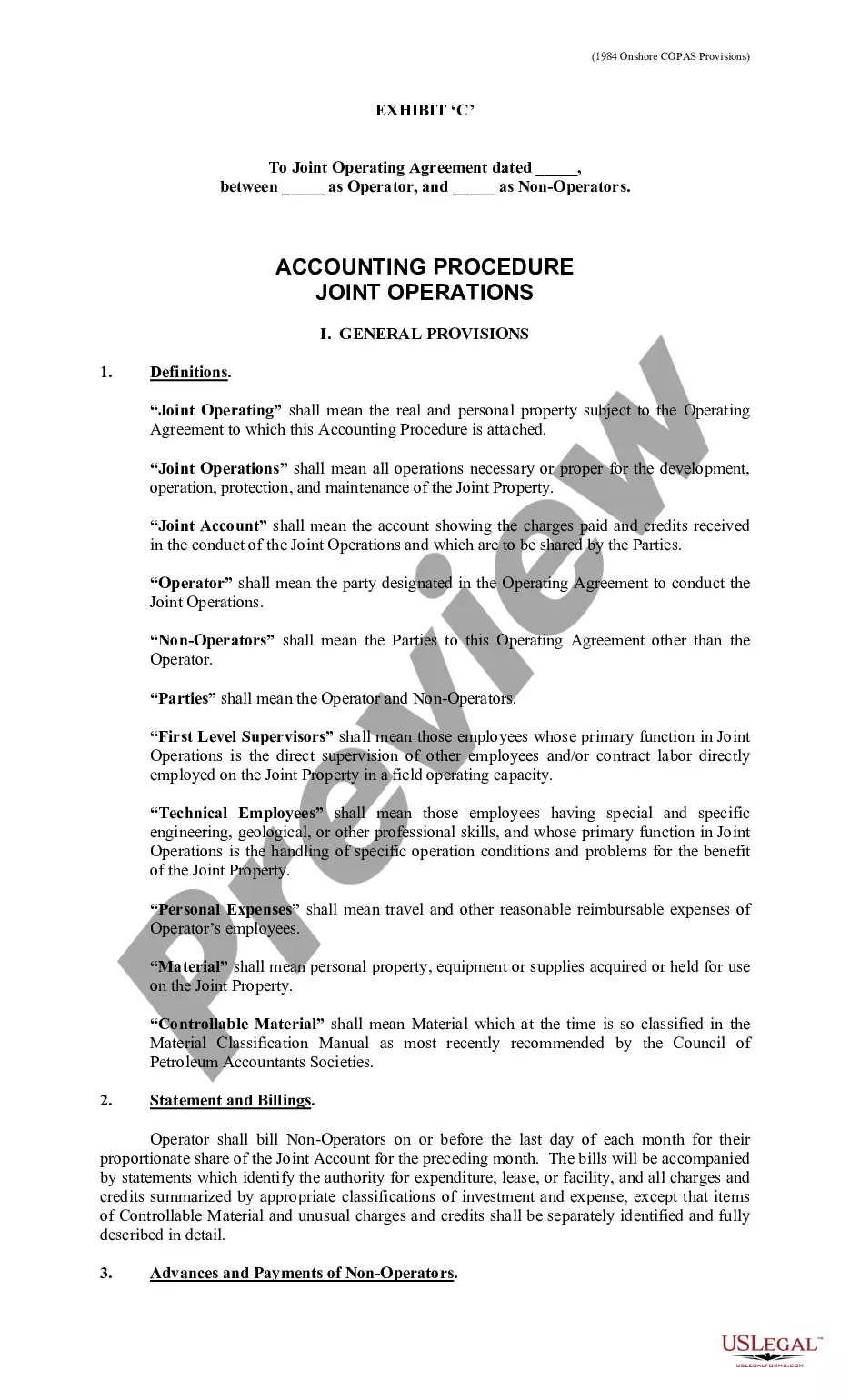

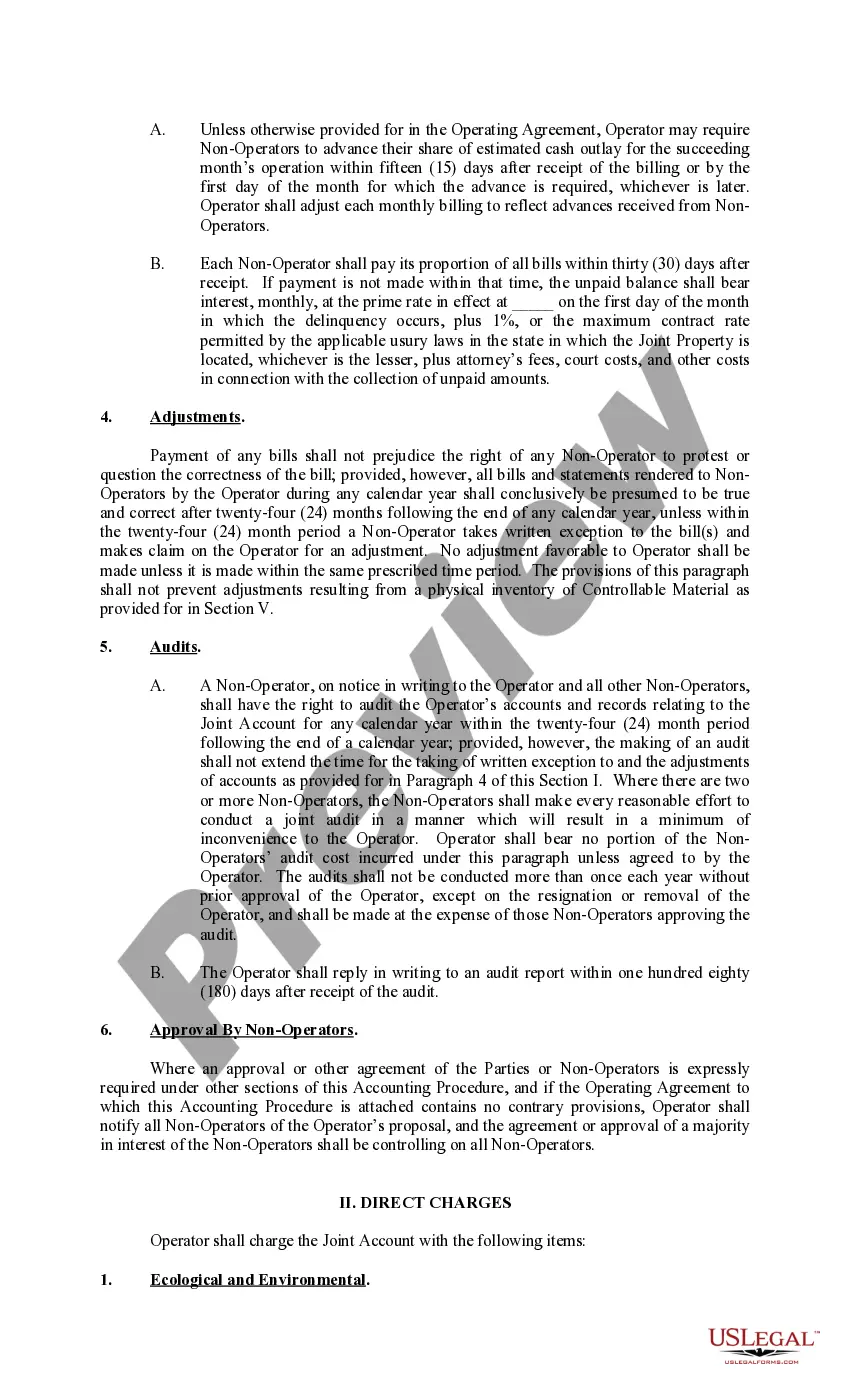

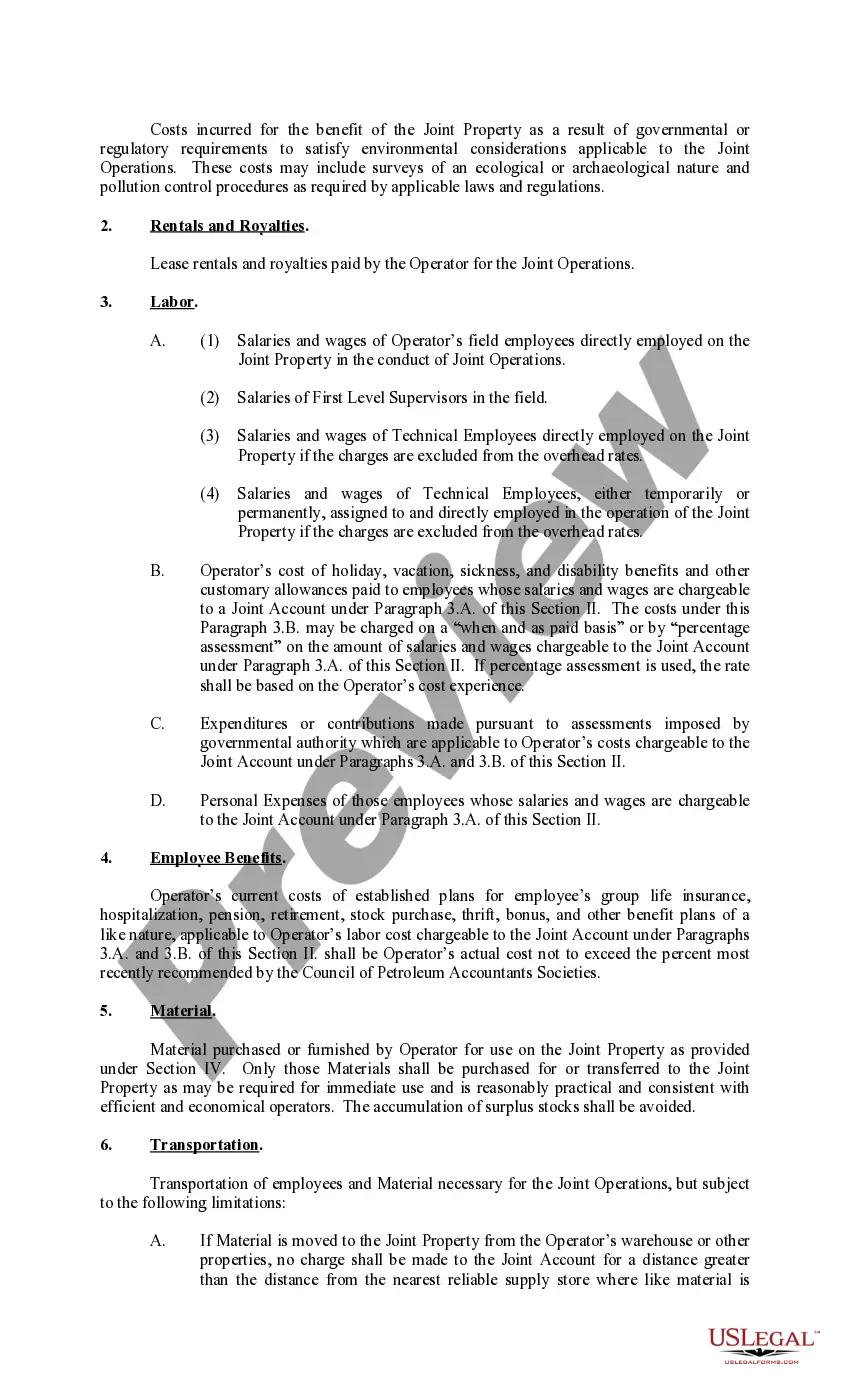

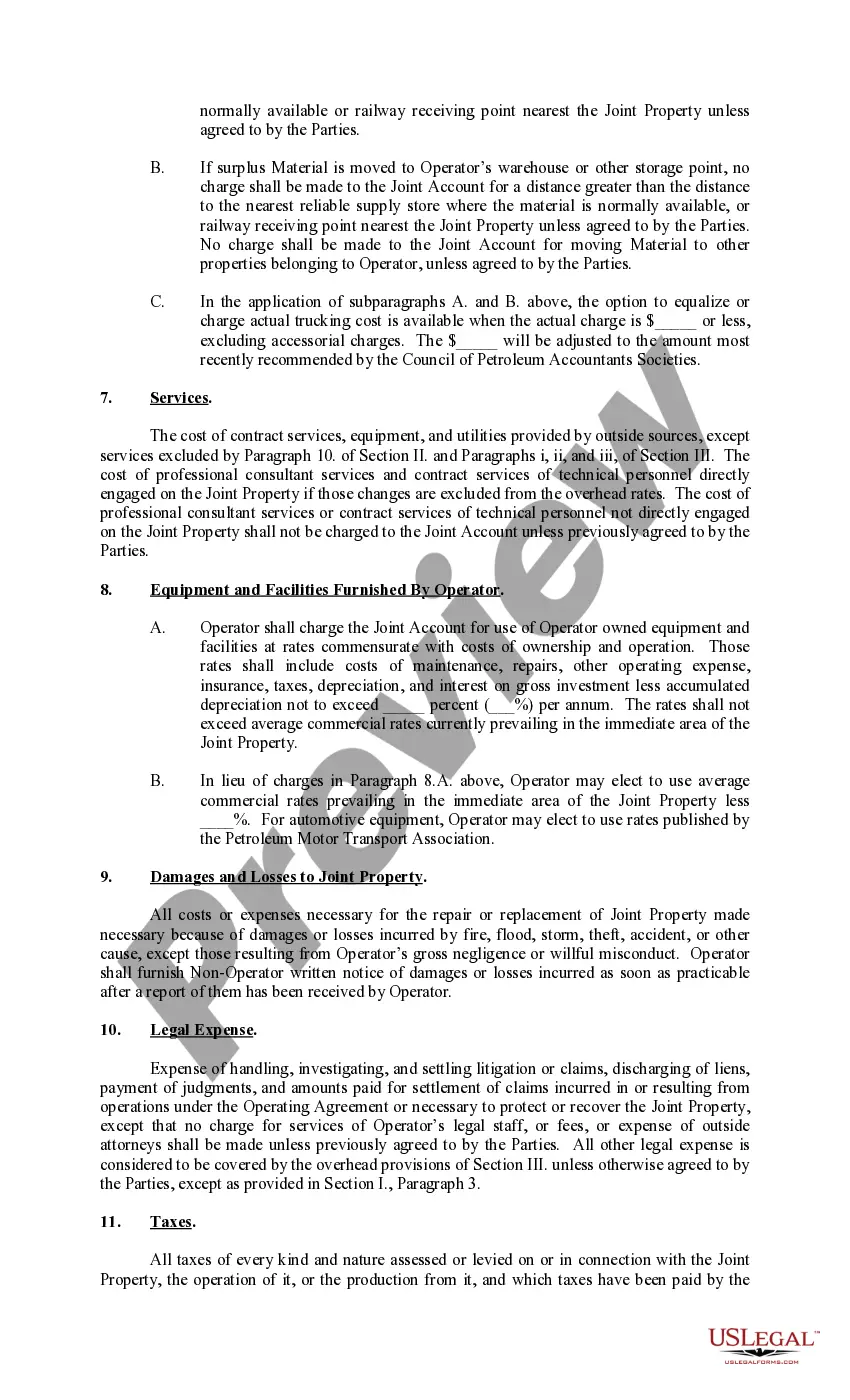

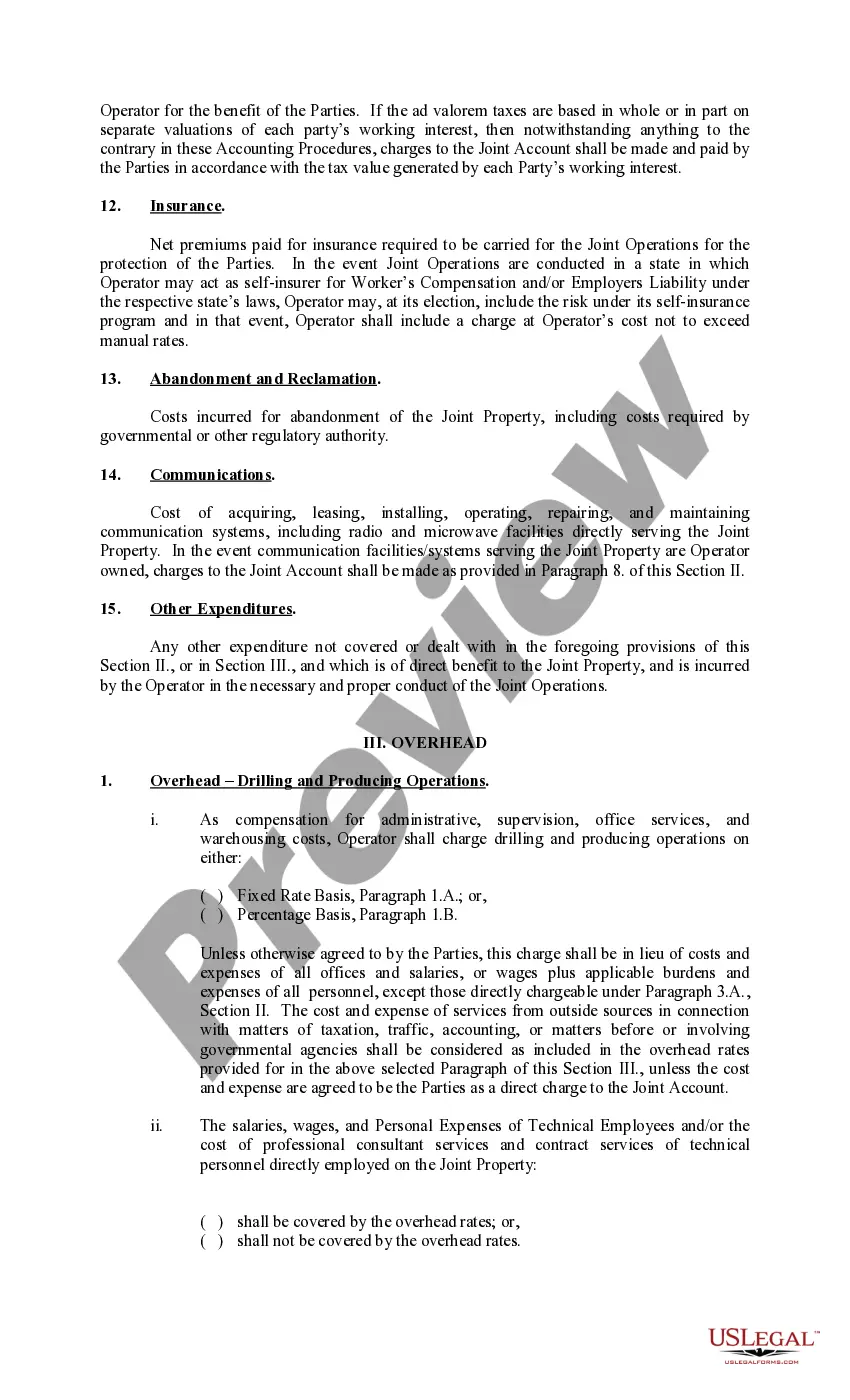

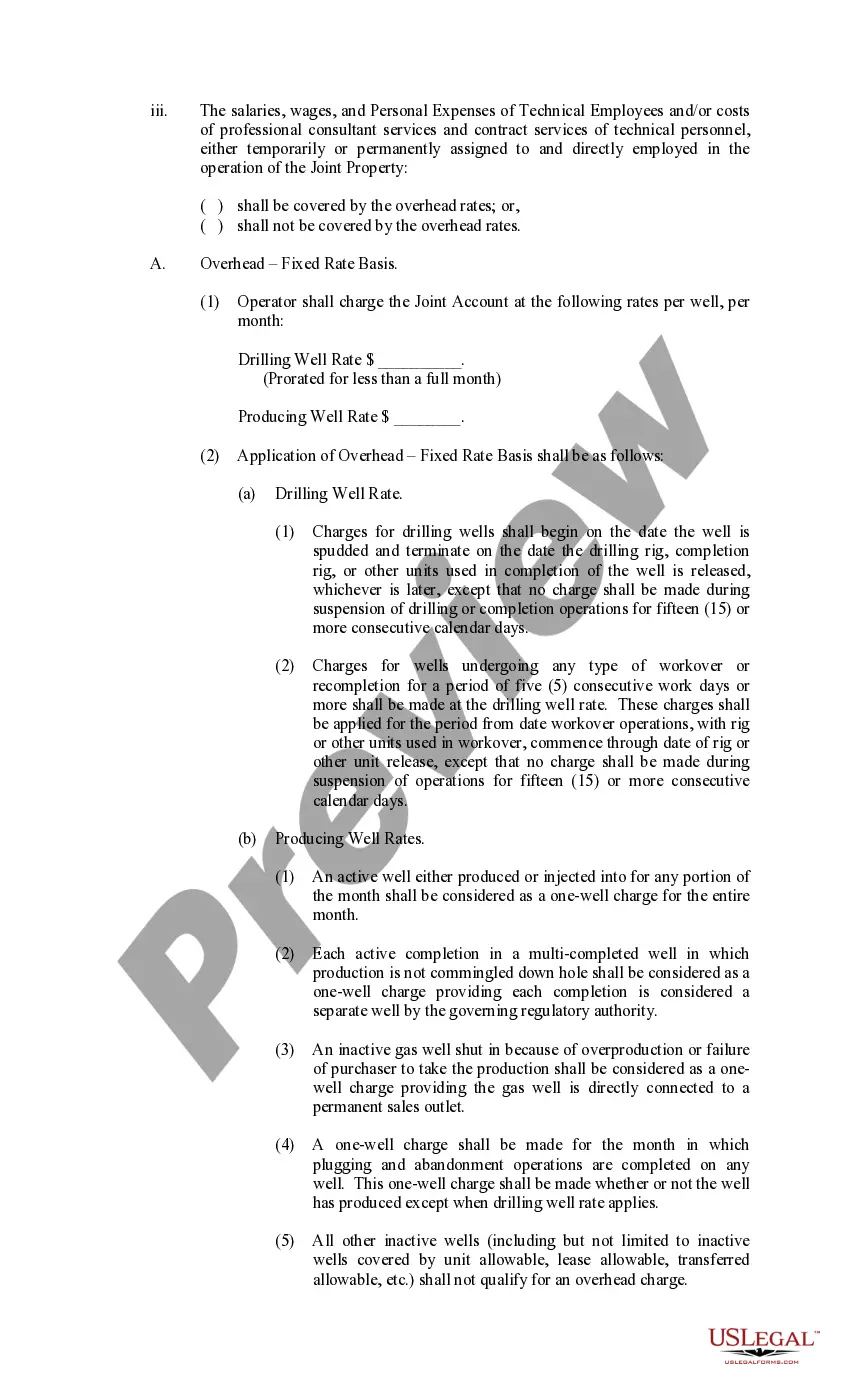

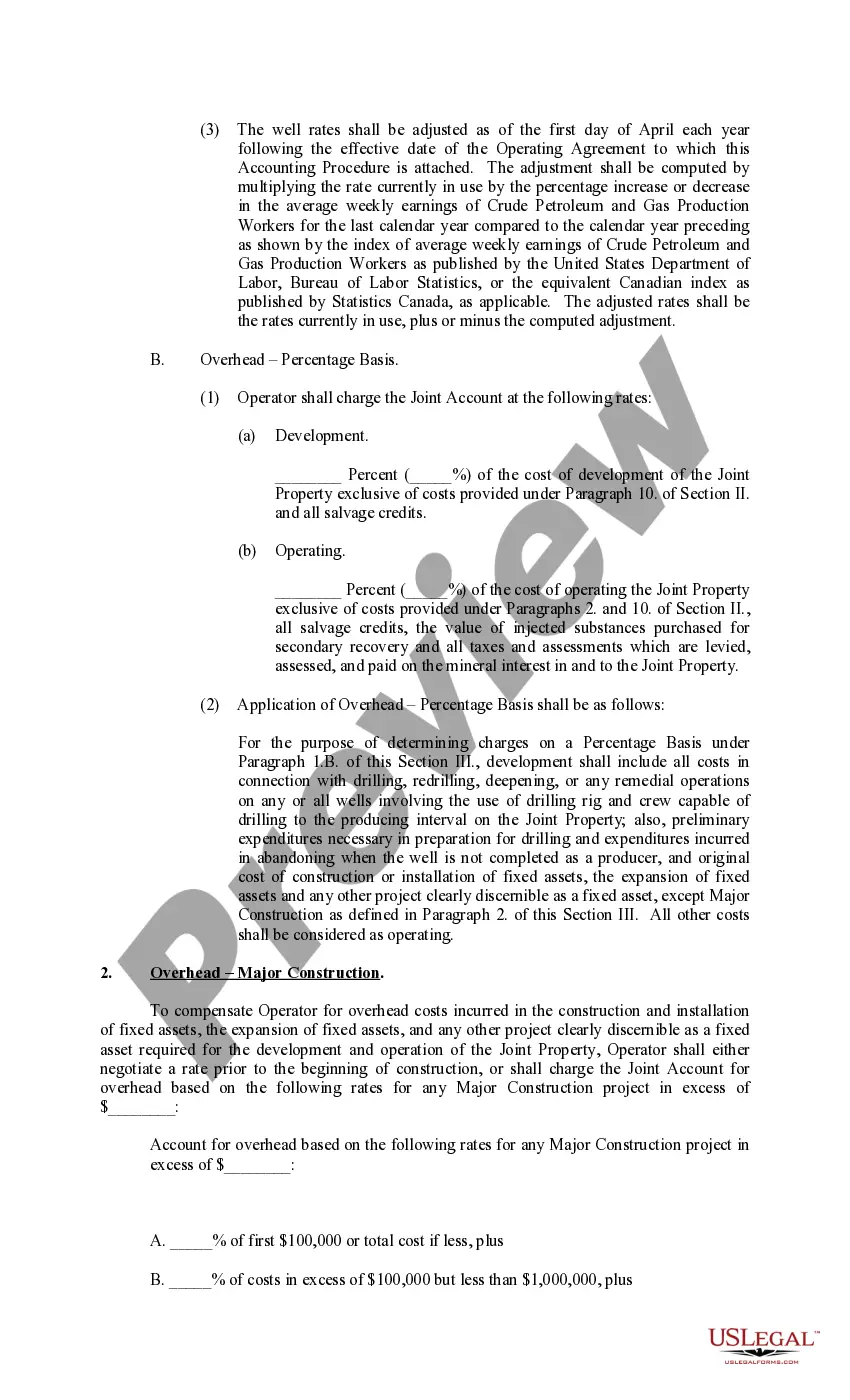

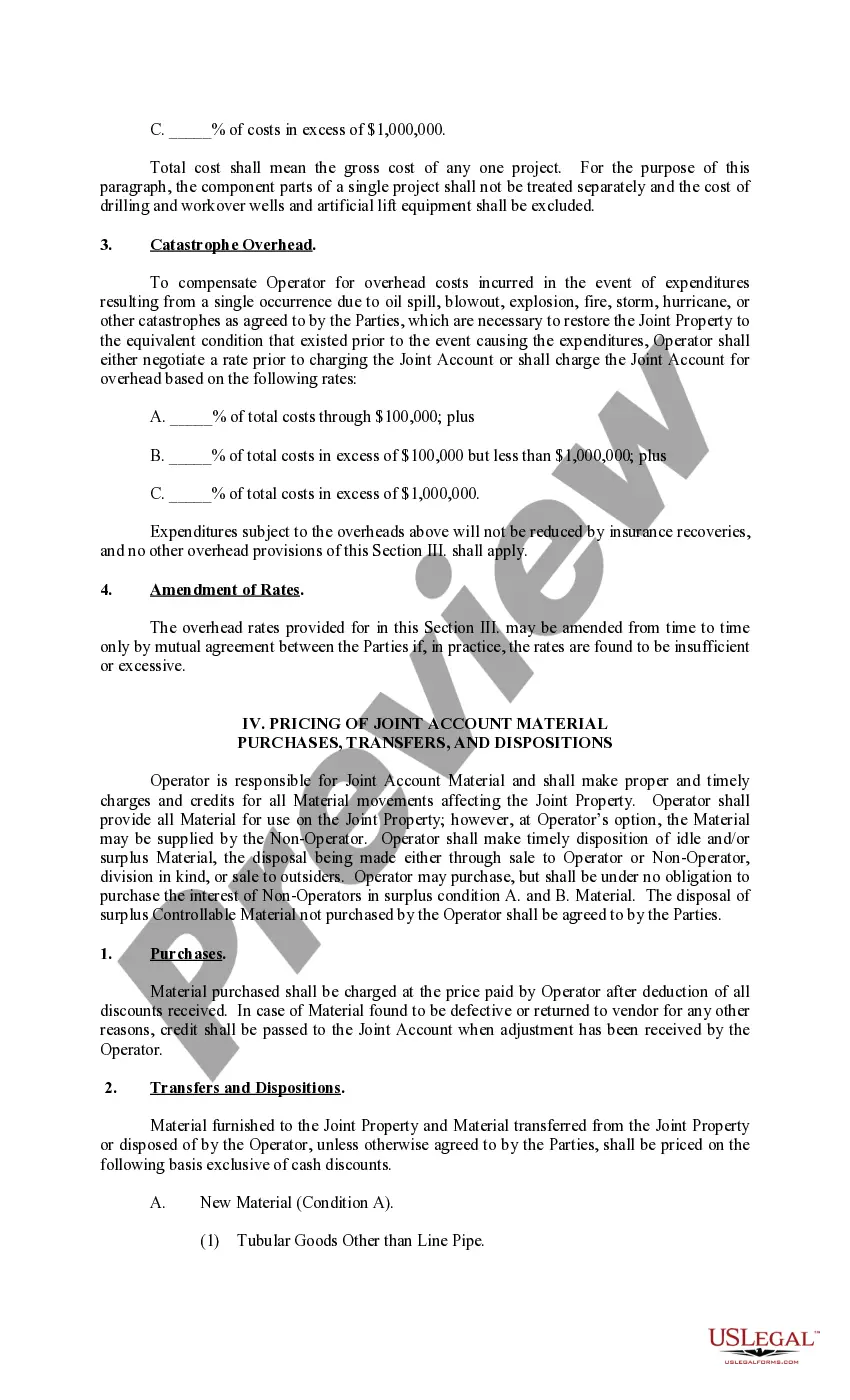

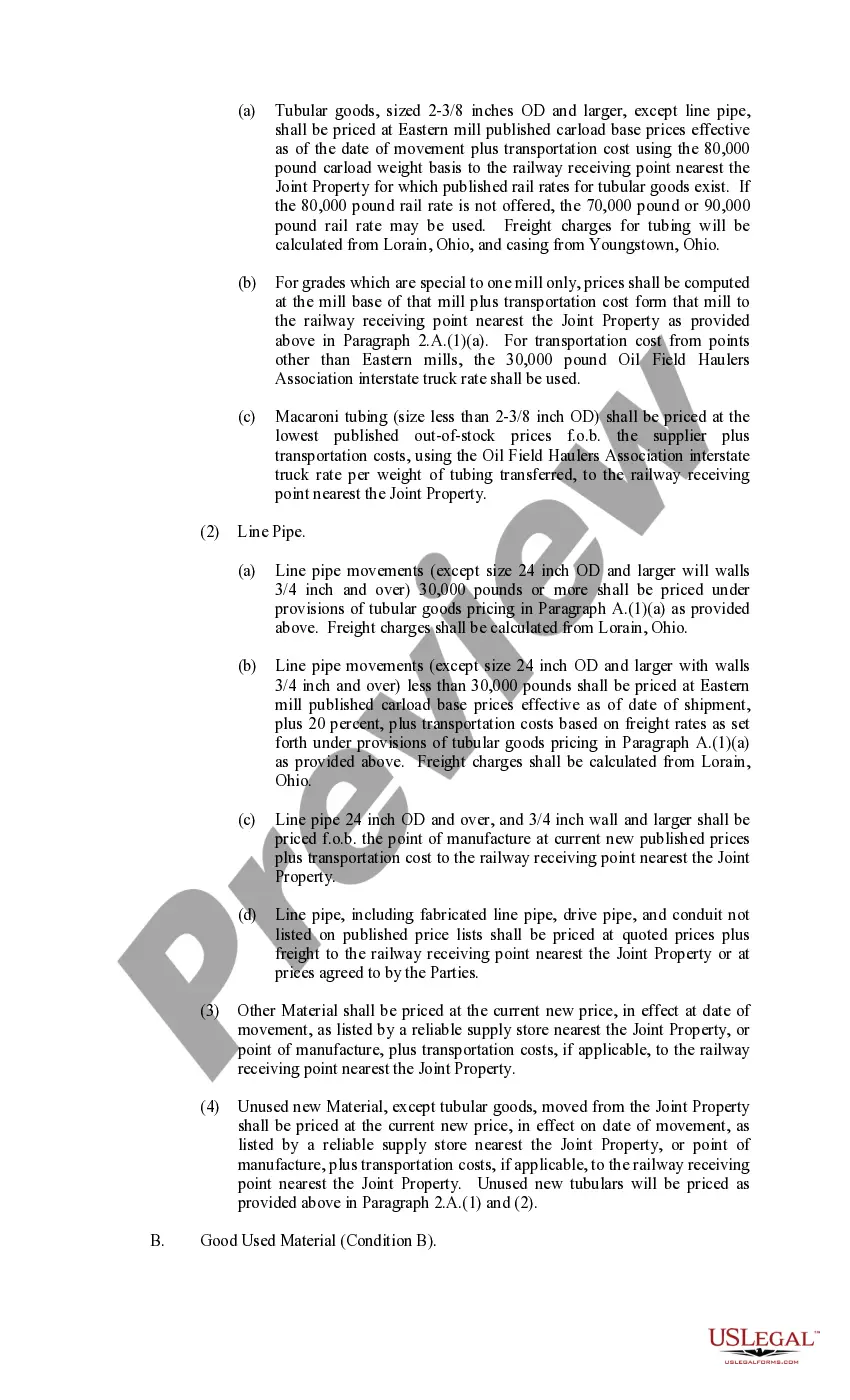

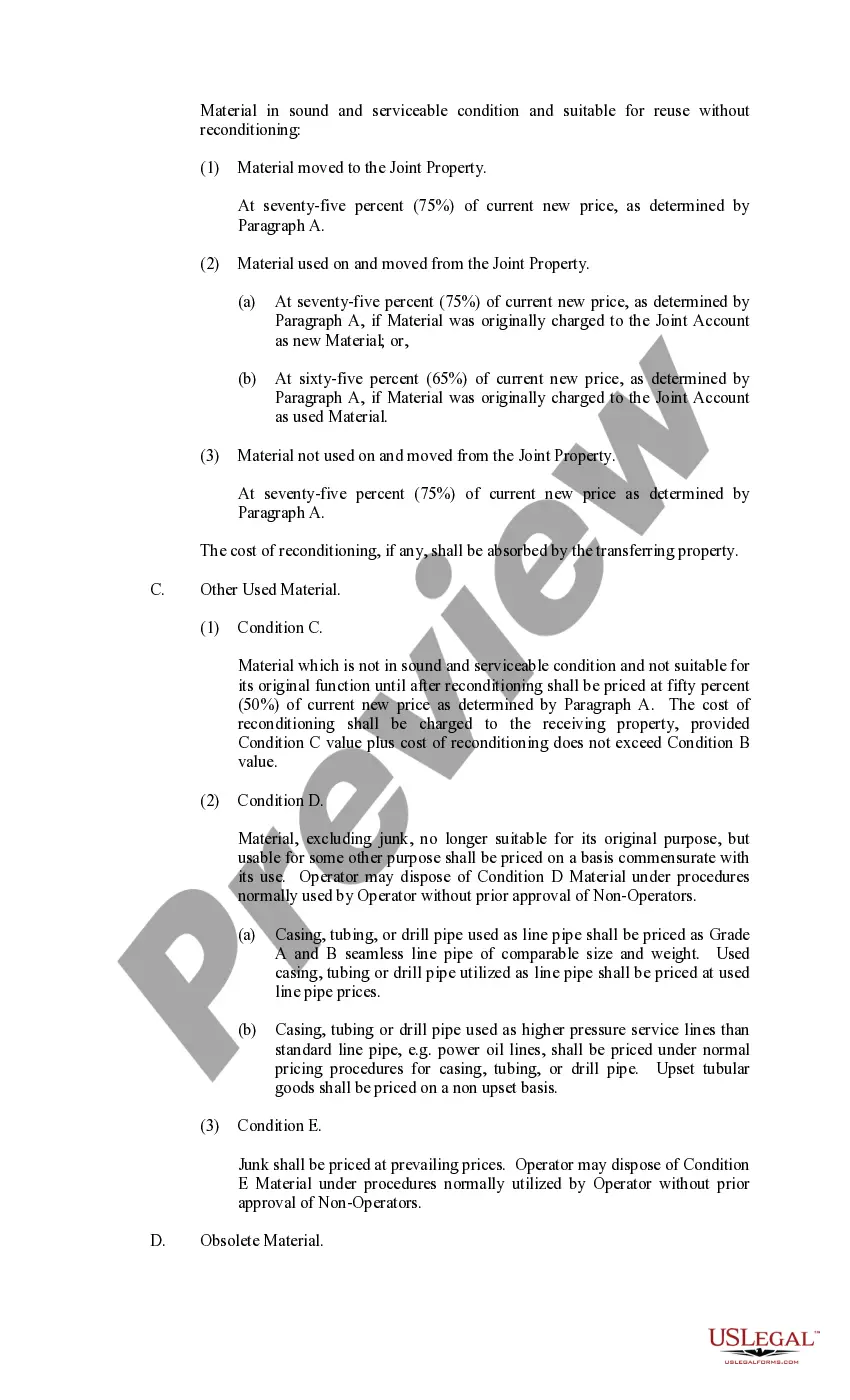

Maryland Exhibit C Accounting Procedure Joint Operations is a standardized accounting procedure followed in Maryland for joint operations. It sets guidelines and rules for accounting practices specific to joint ventures involving multiple entities. This accounting procedure ensures accuracy, transparency, and consistency in financial reporting. Keywords: Maryland, Exhibit C, accounting procedure, joint operations. There are two recognized types of Maryland Exhibit C Accounting Procedure Joint Operations: 1. Maryland Exhibit C Accounting Procedure Joint Operations for Private Sector Companies: This type of accounting procedure is applicable to joint ventures involving private sector companies in Maryland. It provides a framework for recording, classifying, summarizing, and reporting financial transactions and activities related to joint operations. It covers various aspects like revenue recognition, cost allocation, asset valuation, and financial statement presentation. 2. Maryland Exhibit C Accounting Procedure Joint Operations for Public Sector Companies: This type of accounting procedure is specifically designed for joint ventures involving public sector entities in Maryland. It outlines the accounting treatment for joint operations carried out by government agencies, municipalities, and other publicly owned entities. It includes guidelines for financial statement preparation, budgetary controls, fund accounting, grants management, interagency transactions, and compliance with governmental accounting principles. In both types of Maryland Exhibit C Accounting Procedure Joint Operations, the key focus is on maintaining proper accounting records, ensuring the accuracy of financial information, and aligning with applicable accounting standards such as Generally Accepted Accounting Principles (GAAP) or Governmental Accounting Standards Board (GAS) standards. These accounting procedures play a crucial role in promoting accountability, minimizing financial risks, facilitating decision-making, and enhancing transparency in joint operations conducted within Maryland. Companies and entities engaging in joint ventures must adhere to these procedures to establish a clear and consistent accounting framework, thereby enabling effective financial management and reporting.

Maryland Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Maryland Exhibit C Accounting Procedure Joint Operations?

Are you presently within a place in which you require paperwork for sometimes business or individual uses almost every day? There are a variety of legitimate papers web templates accessible on the Internet, but finding kinds you can trust isn`t simple. US Legal Forms offers 1000s of type web templates, just like the Maryland Exhibit C Accounting Procedure Joint Operations, that happen to be created to satisfy federal and state specifications.

When you are presently acquainted with US Legal Forms website and get an account, just log in. After that, you can acquire the Maryland Exhibit C Accounting Procedure Joint Operations format.

Unless you come with an profile and would like to begin using US Legal Forms, adopt these measures:

- Find the type you will need and ensure it is to the proper area/region.

- Utilize the Preview switch to review the form.

- Look at the description to ensure that you have selected the right type.

- In the event the type isn`t what you`re searching for, utilize the Lookup field to discover the type that meets your needs and specifications.

- Whenever you find the proper type, just click Buy now.

- Select the costs plan you want, complete the required information and facts to create your bank account, and pay for the order with your PayPal or credit card.

- Decide on a handy file format and acquire your copy.

Discover each of the papers web templates you have bought in the My Forms food list. You can obtain a more copy of Maryland Exhibit C Accounting Procedure Joint Operations anytime, if required. Just click on the necessary type to acquire or produce the papers format.

Use US Legal Forms, the most considerable collection of legitimate types, to conserve time as well as prevent errors. The service offers expertly produced legitimate papers web templates which can be used for a variety of uses. Produce an account on US Legal Forms and start creating your way of life easier.