This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

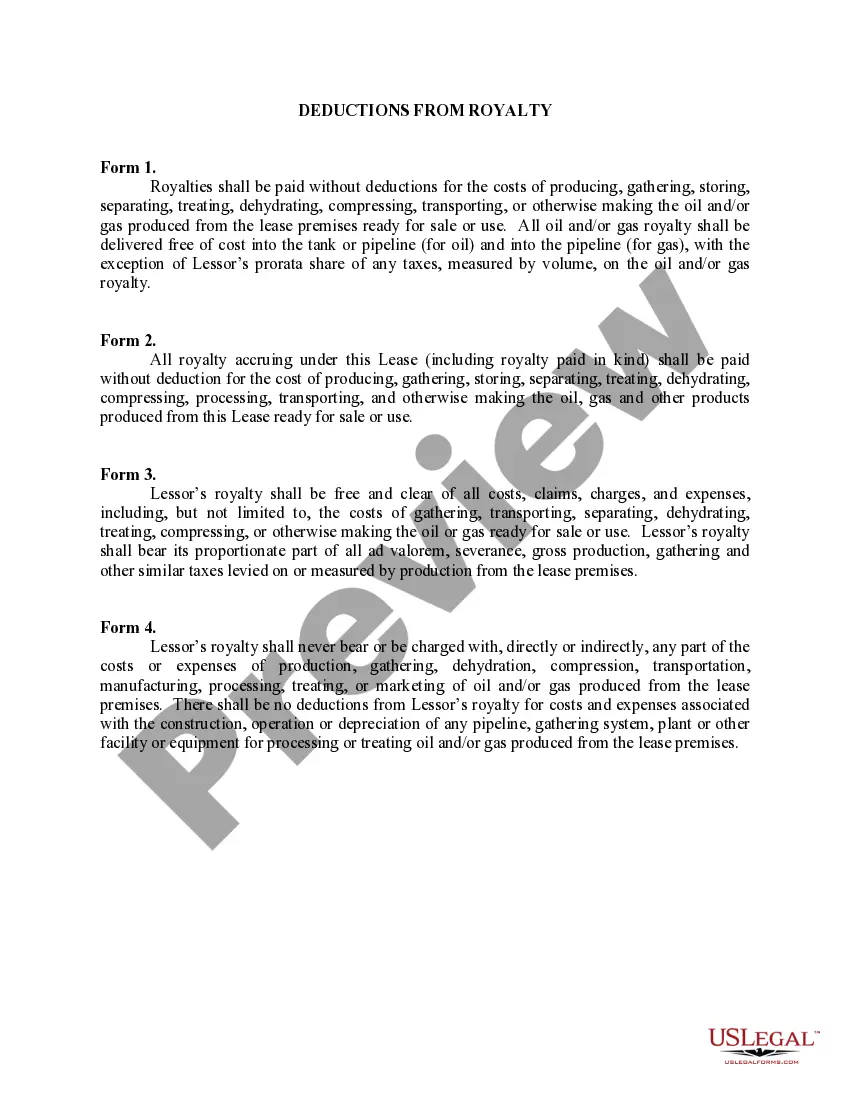

Maryland Deductions from Royalty refer to specific provisions and regulations that allow taxpayers in the state of Maryland to claim deductions from their royalty income. These deductions help reduce the taxable amount, resulting in potential tax savings for individuals or businesses receiving royalty payments. Below are the key types of Maryland Deductions from Royalty: 1. Ordinary and Necessary Expenses: Taxpayers can deduct ordinary and necessary expenses directly related to generating royalty income. These expenses include research and development costs, legal fees, management fees, and other expenditures incurred in producing or protecting the intellectual property rights that generate the royalty income. 2. Tangible Property Expenses: Maryland allows deductions for expenses associated with tangible property used in the production of royalty income. This may include depreciation, repairs, maintenance, and other costs related to equipment, machinery, or facilities utilized in royalty-generating activities. 3. Qualified Production Activities: Taxpayers engaging in qualified production activities within Maryland can claim deductions from royalty income. These deductions are aimed at promoting and encouraging certain industries, such as manufacturing, technology development, or creative arts, by providing tax incentives for royalty-generated income associated with qualifying activities. 4. Royalty Payments to Foreign Entities: Maryland may also permit deductions for royalty payments made to foreign entities under certain circumstances. Taxpayers need to ensure compliance with international tax laws and demonstrate that such payments are genuine and necessary business transactions to qualify for this deduction. 5. Intangible Property Expenses: Expenses incurred in the creation, acquisition, or maintenance of intangible property that generates royalty income may be eligible for deductions in Maryland. This includes costs associated with obtaining patents, copyrights, trademarks, franchises, and other intangible assets. It's important to note that taxpayers must meet specific criteria and guidelines set forth by the Maryland state tax authority to claim these deductions accurately. Consulting with a qualified tax professional or referring to Maryland's official tax resources will help ensure compliance and maximize deductions eligible to the individual or business receiving royalty income.Maryland Deductions from Royalty refer to specific provisions and regulations that allow taxpayers in the state of Maryland to claim deductions from their royalty income. These deductions help reduce the taxable amount, resulting in potential tax savings for individuals or businesses receiving royalty payments. Below are the key types of Maryland Deductions from Royalty: 1. Ordinary and Necessary Expenses: Taxpayers can deduct ordinary and necessary expenses directly related to generating royalty income. These expenses include research and development costs, legal fees, management fees, and other expenditures incurred in producing or protecting the intellectual property rights that generate the royalty income. 2. Tangible Property Expenses: Maryland allows deductions for expenses associated with tangible property used in the production of royalty income. This may include depreciation, repairs, maintenance, and other costs related to equipment, machinery, or facilities utilized in royalty-generating activities. 3. Qualified Production Activities: Taxpayers engaging in qualified production activities within Maryland can claim deductions from royalty income. These deductions are aimed at promoting and encouraging certain industries, such as manufacturing, technology development, or creative arts, by providing tax incentives for royalty-generated income associated with qualifying activities. 4. Royalty Payments to Foreign Entities: Maryland may also permit deductions for royalty payments made to foreign entities under certain circumstances. Taxpayers need to ensure compliance with international tax laws and demonstrate that such payments are genuine and necessary business transactions to qualify for this deduction. 5. Intangible Property Expenses: Expenses incurred in the creation, acquisition, or maintenance of intangible property that generates royalty income may be eligible for deductions in Maryland. This includes costs associated with obtaining patents, copyrights, trademarks, franchises, and other intangible assets. It's important to note that taxpayers must meet specific criteria and guidelines set forth by the Maryland state tax authority to claim these deductions accurately. Consulting with a qualified tax professional or referring to Maryland's official tax resources will help ensure compliance and maximize deductions eligible to the individual or business receiving royalty income.